What is NTC Thermostat - Global Market?

The NTC Thermostat, or Negative Temperature Coefficient Thermostat, is a crucial component in various electronic devices and systems globally. It operates on the principle that its resistance decreases as the temperature increases, making it an essential tool for temperature sensing and control. This characteristic allows NTC thermostats to be widely used in applications where precise temperature monitoring is necessary, such as in automotive, consumer electronics, and industrial equipment. The global market for NTC thermostats is driven by the increasing demand for efficient temperature control solutions in these sectors. As industries continue to innovate and integrate more sophisticated technologies, the need for reliable and accurate temperature management systems like NTC thermostats becomes even more critical. This market is characterized by a diverse range of products tailored to meet specific industry needs, from simple temperature sensors to complex integrated systems. The ongoing advancements in technology and the growing emphasis on energy efficiency and sustainability further propel the demand for NTC thermostats worldwide. As a result, the NTC Thermostat market is poised for steady growth, reflecting its indispensable role in modern technology and industry.

Mechanical, Digital in the NTC Thermostat - Global Market:

In the realm of NTC Thermostats, two primary types dominate the global market: mechanical and digital. Mechanical NTC thermostats are traditional devices that rely on physical components to regulate temperature. They are often used in applications where simplicity and reliability are paramount, such as in household appliances and basic industrial equipment. These thermostats operate by using a bimetallic strip or a similar mechanism that physically moves to open or close a circuit as the temperature changes. This movement adjusts the flow of electricity, thereby controlling the temperature. Mechanical NTC thermostats are valued for their durability and straightforward design, making them a cost-effective solution for many applications. However, they may lack the precision and flexibility offered by their digital counterparts. Digital NTC thermostats, on the other hand, represent the modern evolution of temperature control technology. These devices utilize electronic sensors and microprocessors to monitor and adjust temperature settings with high accuracy. Digital NTC thermostats are commonly found in advanced applications where precise temperature control is crucial, such as in HVAC systems, automotive climate control, and sophisticated industrial processes. The digital nature of these thermostats allows for programmable settings, remote control capabilities, and integration with smart home systems, offering users enhanced convenience and efficiency. Additionally, digital NTC thermostats often feature user-friendly interfaces, such as touchscreens or mobile app connectivity, enabling easy customization and monitoring of temperature settings. The global market for NTC thermostats is witnessing a shift towards digital solutions, driven by the increasing demand for smart and energy-efficient technologies. As industries and consumers alike prioritize sustainability and cost savings, digital NTC thermostats offer significant advantages in terms of energy management and operational efficiency. Moreover, the integration of Internet of Things (IoT) technology into digital NTC thermostats is opening new avenues for innovation and application. IoT-enabled thermostats can communicate with other smart devices, providing real-time data and insights that enhance overall system performance and user experience. Despite the growing popularity of digital NTC thermostats, mechanical variants continue to hold a significant share of the market, particularly in regions or sectors where cost constraints and simplicity are key considerations. The choice between mechanical and digital NTC thermostats often depends on the specific requirements of the application, including factors such as budget, desired level of control, and environmental conditions. As the global market evolves, manufacturers are focusing on developing hybrid solutions that combine the best features of both mechanical and digital technologies, offering users a versatile and adaptable approach to temperature management. In conclusion, the NTC Thermostat global market is characterized by a dynamic interplay between mechanical and digital technologies. While digital NTC thermostats are gaining traction due to their advanced features and energy efficiency, mechanical thermostats remain a viable option for many applications. The ongoing advancements in technology and the increasing emphasis on smart solutions are likely to shape the future of this market, driving innovation and expanding the range of applications for NTC thermostats worldwide.

Online, Offline in the NTC Thermostat - Global Market:

The usage of NTC Thermostats in the global market spans both online and offline channels, each offering distinct advantages and challenges. In the online realm, the sale and distribution of NTC thermostats have been significantly bolstered by the rise of e-commerce platforms and digital marketplaces. Online channels provide manufacturers and distributors with a broader reach, enabling them to connect with a global customer base. This accessibility is particularly beneficial for small and medium-sized enterprises (SMEs) that may not have the resources to establish a physical presence in multiple regions. Through online platforms, customers can easily compare products, read reviews, and make informed purchasing decisions, enhancing the overall buying experience. Additionally, online sales channels often offer competitive pricing and promotional deals, attracting cost-conscious consumers and businesses. However, the online market for NTC thermostats also presents certain challenges. The lack of physical interaction with the product can be a drawback for customers who prefer to see and test the product before purchasing. This limitation can be mitigated through detailed product descriptions, high-quality images, and virtual demonstrations, but it remains a consideration for some buyers. Furthermore, the online market is highly competitive, with numerous sellers vying for attention. To succeed in this environment, companies must invest in effective digital marketing strategies, search engine optimization, and customer engagement initiatives to stand out from the competition. In contrast, the offline market for NTC thermostats involves traditional retail channels, including brick-and-mortar stores, distributors, and direct sales. Offline channels offer the advantage of personal interaction, allowing customers to physically examine the product and receive immediate assistance from sales representatives. This face-to-face engagement can build trust and confidence, particularly for complex or high-value purchases. Offline sales channels are also well-suited for B2B transactions, where personalized service and long-term relationships are often prioritized. In industries such as manufacturing and construction, where NTC thermostats are frequently used, offline channels provide a reliable and established means of procurement. Despite the benefits of offline channels, they are not without their challenges. Establishing and maintaining a physical presence can be costly, requiring significant investment in infrastructure, staffing, and logistics. Additionally, offline sales are typically limited by geographical constraints, restricting the potential customer base to a specific region. To overcome these limitations, many companies adopt a hybrid approach, leveraging both online and offline channels to maximize their reach and effectiveness. This omnichannel strategy allows businesses to cater to diverse customer preferences and adapt to changing market dynamics. In summary, the global market for NTC thermostats utilizes both online and offline channels to meet the diverse needs of consumers and industries. Online channels offer convenience, accessibility, and competitive pricing, while offline channels provide personal interaction and established relationships. Each channel has its unique advantages and challenges, and the choice between them often depends on factors such as target audience, product complexity, and market conditions. As the market continues to evolve, companies are increasingly adopting integrated strategies that combine the strengths of both online and offline channels, ensuring a comprehensive and flexible approach to sales and distribution.

NTC Thermostat - Global Market Outlook:

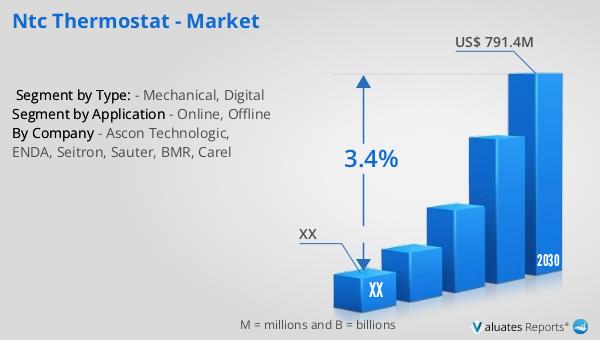

The global market for NTC Thermostats was valued at approximately $623.2 million in 2023, with projections indicating a growth to around $791.4 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.4% from 2024 to 2030. The market for NTC Negative Temperature Coefficient Thermistors is notably fragmented, characterized by intense competition among numerous players. The top ten companies in this sector collectively account for 69% of the total revenue market share, highlighting the competitive nature of the industry. The Asia Pacific region emerges as the largest market for NTC thermostats, capturing about 71% of the market share in terms of volume. This dominance can be attributed to the region's robust industrial base, rapid technological advancements, and increasing demand for efficient temperature control solutions. The competitive landscape and regional dynamics underscore the complexity and potential of the NTC Thermostat market, as companies strive to innovate and capture a larger share of this growing industry.

| Report Metric | Details |

| Report Name | NTC Thermostat - Market |

| Forecasted market size in 2030 | US$ 791.4 million |

| CAGR | 3.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ascon Technologic, ENDA, Seitron, Sauter, BMR, Carel |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |