What is Global Video Wall Software Market?

The Global Video Wall Software Market is a dynamic and rapidly evolving sector that focuses on the development and distribution of software solutions designed to manage and operate video wall systems. Video walls are large displays made up of multiple screens or panels that work together to present a cohesive visual experience. These systems are widely used in various industries, including retail, entertainment, transportation, and corporate environments, to deliver impactful visual content. The software that powers these video walls is crucial as it enables users to control the content, layout, and functionality of the displays. It allows for seamless integration of different media types, real-time data visualization, and interactive features, enhancing the overall user experience. The market for video wall software is driven by the increasing demand for advanced display technologies and the need for effective communication tools in both public and private sectors. As businesses and organizations continue to seek innovative ways to engage their audiences and convey information, the demand for sophisticated video wall software solutions is expected to grow. This market is characterized by a diverse range of offerings, from basic software packages to highly specialized solutions tailored to specific industry needs.

Professional Edition, Standard Edition in the Global Video Wall Software Market:

In the Global Video Wall Software Market, there are different editions of software available to cater to the varying needs of users, primarily categorized into Professional Edition and Standard Edition. The Professional Edition is designed for users who require advanced features and capabilities. It typically includes a comprehensive set of tools for managing complex video wall configurations, supporting high-resolution content, and offering extensive customization options. This edition is ideal for large-scale installations in environments such as control rooms, broadcast studios, and corporate headquarters, where precision and flexibility are paramount. Users can benefit from features like multi-user access, remote management, and integration with other enterprise systems, ensuring seamless operation and collaboration. On the other hand, the Standard Edition is tailored for users who need essential functionalities without the complexity of advanced features. It provides a user-friendly interface and straightforward tools for setting up and managing video walls, making it suitable for smaller installations or organizations with limited technical expertise. This edition is often used in retail spaces, educational institutions, and small businesses where the focus is on delivering clear and engaging visual content without the need for extensive customization. Both editions play a crucial role in the Global Video Wall Software Market by addressing the diverse requirements of different user segments. The choice between Professional and Standard Editions depends on factors such as the scale of the installation, budget constraints, and the specific needs of the organization. As the market continues to evolve, software providers are constantly enhancing their offerings to include new features and capabilities, ensuring that users have access to the latest technologies and tools. This ongoing innovation is essential for meeting the growing demand for video wall solutions and maintaining a competitive edge in the market. By offering a range of options, from basic to advanced, the Global Video Wall Software Market ensures that users can find the right solution to meet their unique needs and achieve their communication goals.

Commercial, Home in the Global Video Wall Software Market:

The usage of Global Video Wall Software Market solutions extends across various sectors, including commercial and home environments, each with its unique set of requirements and applications. In commercial settings, video wall software is utilized to create immersive and engaging visual experiences that capture the attention of audiences. Retailers, for instance, use video walls to showcase products, promotions, and brand messages in a dynamic and visually appealing manner. The software allows for the integration of multimedia content, real-time updates, and interactive features, enhancing the overall shopping experience and driving customer engagement. In corporate environments, video walls serve as powerful communication tools for presentations, data visualization, and collaboration. The software enables seamless integration with other enterprise systems, allowing for real-time data sharing and analysis, which is crucial for decision-making processes. In the transportation sector, video walls are used for monitoring and managing operations, providing real-time information to passengers, and ensuring safety and efficiency. The software's ability to handle large volumes of data and display it in an organized and accessible manner is vital for these applications. In home environments, video wall software is gaining popularity as consumers seek to create personalized and immersive entertainment experiences. Home theaters, gaming setups, and smart home systems benefit from the advanced features and customization options offered by video wall software. Users can enjoy high-resolution content, interactive features, and seamless integration with other smart devices, enhancing their overall entertainment experience. The software's user-friendly interface and straightforward setup make it accessible to a wide range of users, from tech enthusiasts to casual consumers. As the demand for advanced display technologies continues to grow, the Global Video Wall Software Market is poised to expand its reach across both commercial and home environments, offering innovative solutions that cater to the diverse needs of users.

Global Video Wall Software Market Outlook:

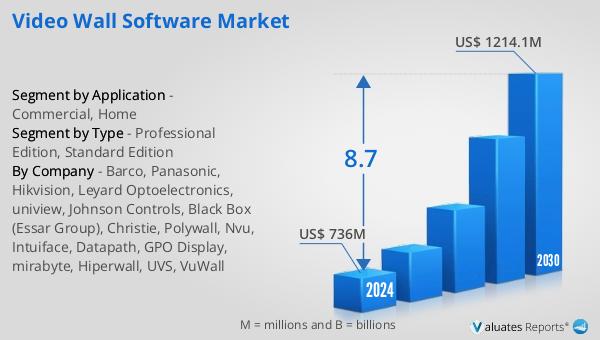

The outlook for the Global Video Wall Software Market is promising, with significant growth projected over the coming years. According to market analysis, the global market for video wall software is expected to expand from $736 million in 2024 to $1,214.1 million by 2030. This growth represents a Compound Annual Growth Rate (CAGR) of 8.7% during the forecast period. This upward trend is driven by several factors, including the increasing demand for advanced display technologies, the need for effective communication tools, and the growing adoption of video wall solutions across various industries. As businesses and organizations continue to seek innovative ways to engage their audiences and convey information, the demand for sophisticated video wall software solutions is expected to grow. The market is characterized by a diverse range of offerings, from basic software packages to highly specialized solutions tailored to specific industry needs. As the market continues to evolve, software providers are constantly enhancing their offerings to include new features and capabilities, ensuring that users have access to the latest technologies and tools. This ongoing innovation is essential for meeting the growing demand for video wall solutions and maintaining a competitive edge in the market. By offering a range of options, from basic to advanced, the Global Video Wall Software Market ensures that users can find the right solution to meet their unique needs and achieve their communication goals.

| Report Metric | Details |

| Report Name | Video Wall Software Market |

| Accounted market size in 2024 | US$ 736 million |

| Forecasted market size in 2030 | US$ 1214.1 million |

| CAGR | 8.7 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Barco, Panasonic, Hikvision, Leyard Optoelectronics, uniview, Johnson Controls, Black Box (Essar Group), Christie, Polywall, Nvu, Intuiface, Datapath, GPO Display, mirabyte, Hiperwall, UVS, VuWall |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |