What is Silage Wrap Film - Global Market?

Silage wrap film is a specialized plastic film used primarily in agriculture to preserve and store silage, which is fermented, high-moisture fodder fed to ruminants like cattle and sheep. This film plays a crucial role in maintaining the nutritional quality of the silage by creating an airtight seal that prevents spoilage and fermentation losses. The global market for silage wrap film is driven by the increasing demand for high-quality animal feed and the need for efficient storage solutions in the agricultural sector. Farmers and agricultural businesses rely on silage wrap film to ensure that their livestock receives nutritious feed throughout the year, regardless of seasonal changes. The film is typically made from polyethylene and is designed to be durable, UV-resistant, and stretchable, allowing it to tightly wrap around bales of silage. This market is expanding as more regions adopt modern farming techniques and seek to improve the efficiency of their feed storage systems. The versatility and effectiveness of silage wrap film make it an essential component in contemporary agricultural practices, contributing to the overall productivity and sustainability of livestock farming.

Three Layers, Five Layers, Seven Layers, Other in the Silage Wrap Film - Global Market:

Silage wrap film is available in various configurations, including three-layer, five-layer, seven-layer, and other multi-layer films, each offering distinct advantages in terms of durability, protection, and performance. The three-layer silage wrap film is a basic option that provides adequate protection for silage bales. It is typically composed of three layers of polyethylene, which offer a balance between cost and functionality. This type of film is suitable for farmers who require a reliable and economical solution for wrapping their silage bales. The three-layer film provides good puncture resistance and UV protection, ensuring that the silage remains fresh and nutritious over time. However, for those seeking enhanced protection and performance, five-layer silage wrap film is a popular choice. This film consists of five layers of polyethylene, which increases its strength and durability. The additional layers provide improved resistance to punctures and tears, making it ideal for use in harsher environmental conditions. The five-layer film also offers superior UV protection, which is crucial for maintaining the quality of the silage during extended storage periods. As a result, this type of film is often preferred by farmers who need to store silage for longer durations or in regions with intense sunlight. For even greater protection and performance, seven-layer silage wrap film is available. This advanced option features seven layers of polyethylene, providing exceptional strength and durability. The multiple layers offer enhanced resistance to punctures, tears, and UV radiation, making it suitable for use in the most demanding agricultural environments. The seven-layer film is designed to withstand extreme weather conditions and provide long-lasting protection for silage bales. It is an ideal choice for farmers who require the highest level of performance and reliability from their silage wrap film. In addition to these standard configurations, other multi-layer films are available, offering specialized features and benefits. These films may include additional layers or unique materials that provide specific advantages, such as increased stretchability, improved cling properties, or enhanced oxygen barrier capabilities. These specialized films are designed to meet the unique needs of different agricultural operations, ensuring that farmers can find the perfect solution for their silage wrapping requirements. Overall, the availability of various multi-layer silage wrap films allows farmers to choose the most suitable option based on their specific needs and environmental conditions. Whether they require basic protection or advanced performance, there is a silage wrap film available to meet their requirements. The diverse range of options ensures that farmers can effectively preserve and store their silage, contributing to the overall success and sustainability of their agricultural operations.

Maize, Sugar Beet Pulp, Alfalfa, Legumes, Others in the Silage Wrap Film - Global Market:

Silage wrap film is widely used in the global market for preserving various types of forage crops, including maize, sugar beet pulp, alfalfa, legumes, and others. Each of these crops has unique characteristics and nutritional profiles, making them valuable components of livestock feed. Maize, also known as corn, is one of the most common crops used in silage production. It is highly nutritious and provides a rich source of energy for livestock. Silage wrap film is used to tightly seal maize bales, preventing oxygen from entering and causing spoilage. This ensures that the maize retains its nutritional value and remains palatable for animals. The use of silage wrap film in maize production is particularly important in regions where maize is a staple feed for livestock, as it helps to maintain a consistent supply of high-quality feed throughout the year. Sugar beet pulp is another crop commonly preserved using silage wrap film. It is a byproduct of sugar beet processing and is rich in fiber and energy. Silage wrap film helps to protect sugar beet pulp from spoilage and fermentation losses, ensuring that it remains a valuable feed ingredient for livestock. The film's airtight seal prevents the growth of mold and bacteria, preserving the nutritional quality of the sugar beet pulp. This is especially important in regions where sugar beet pulp is a significant component of livestock diets, as it helps to optimize feed efficiency and animal performance. Alfalfa is a highly nutritious forage crop that is often used in silage production. It is rich in protein, vitamins, and minerals, making it an excellent feed for dairy cattle and other livestock. Silage wrap film is used to preserve alfalfa bales, preventing spoilage and maintaining their nutritional quality. The film's UV protection and puncture resistance ensure that the alfalfa remains fresh and palatable, even during extended storage periods. This is crucial for farmers who rely on alfalfa as a primary feed source, as it helps to ensure a consistent supply of high-quality feed for their animals. Legumes, such as clover and peas, are also commonly preserved using silage wrap film. These crops are rich in protein and provide essential nutrients for livestock. Silage wrap film helps to protect legume bales from spoilage and fermentation losses, ensuring that they remain a valuable feed ingredient. The film's airtight seal and UV protection help to maintain the nutritional quality of the legumes, contributing to the overall health and productivity of livestock. In addition to these specific crops, silage wrap film is also used to preserve other types of forage, such as grass and hay. These crops are often used as supplementary feed for livestock, providing additional nutrients and energy. Silage wrap film helps to protect these bales from spoilage and maintain their nutritional quality, ensuring that they remain a valuable feed resource. Overall, the use of silage wrap film in preserving various forage crops is essential for maintaining the nutritional quality and availability of livestock feed. The film's ability to create an airtight seal and protect against spoilage and fermentation losses makes it a valuable tool for farmers and agricultural businesses. By preserving the nutritional quality of forage crops, silage wrap film contributes to the overall success and sustainability of livestock farming operations.

Silage Wrap Film - Global Market Outlook:

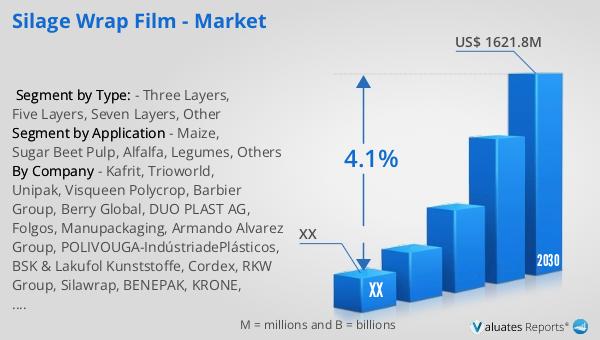

In 2023, the global market for silage wrap film was valued at approximately $1,229 million. This market is projected to grow, reaching an adjusted size of around $1,621.8 million by the year 2030, with a compound annual growth rate (CAGR) of 4.1% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for efficient and reliable solutions in the agricultural sector to preserve and store high-quality animal feed. The North American market for silage wrap film also shows promising potential, although specific figures for 2023 and 2030 are not provided. However, it is expected to experience growth during the same forecast period, driven by advancements in farming techniques and the need for sustainable feed storage solutions. The consistent growth in the silage wrap film market highlights the importance of this product in modern agriculture, as it plays a crucial role in maintaining the nutritional quality of livestock feed and supporting the productivity of farming operations. As more regions adopt innovative agricultural practices, the demand for silage wrap film is likely to continue its upward trajectory, contributing to the overall development and sustainability of the global agricultural industry.

| Report Metric | Details |

| Report Name | Silage Wrap Film - Market |

| Forecasted market size in 2030 | US$ 1621.8 million |

| CAGR | 4.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kafrit, Trioworld, Unipak, Visqueen Polycrop, Barbier Group, Berry Global, DUO PLAST AG, Folgos, Manupackaging, Armando Alvarez Group, POLIVOUGA-IndústriadePlásticos, BSK & Lakufol Kunststoffe, Cordex, RKW Group, Silawrap, BENEPAK, KRONE, Trioplast, Rani Plast, Plastika Kritis, Keqiang Plastics, Silage Packaging, Zill, KOROZO |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |