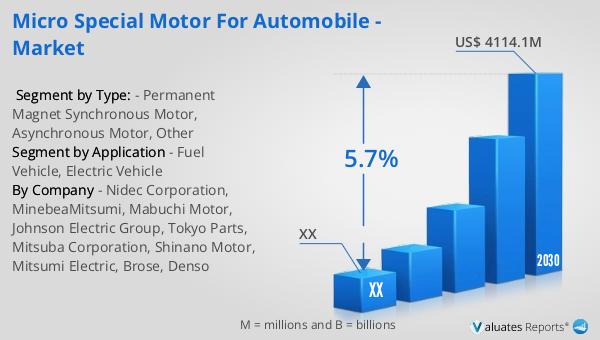

What is Micro Special Motor for Automobile - Global Market?

Micro special motors for automobiles are compact, highly efficient motors designed to perform specific functions within vehicles. These motors are integral to modern automotive systems, providing precise control and enhancing the performance of various vehicle components. They are used in a wide range of applications, from power windows and seats to advanced driver-assistance systems (ADAS) and electric power steering. The global market for these motors is driven by the increasing demand for advanced automotive technologies and the growing trend towards vehicle electrification. As automakers strive to improve fuel efficiency and reduce emissions, the adoption of micro special motors is expected to rise. These motors are engineered to deliver high performance while maintaining energy efficiency, making them ideal for both traditional fuel vehicles and electric vehicles. The market is characterized by continuous innovation, with manufacturers focusing on developing motors that offer improved performance, reliability, and cost-effectiveness. As the automotive industry evolves, the role of micro special motors is becoming increasingly significant, contributing to the advancement of vehicle technology and the enhancement of the overall driving experience.

Permanent Magnet Synchronous Motor, Asynchronous Motor, Other in the Micro Special Motor for Automobile - Global Market:

Permanent Magnet Synchronous Motors (PMSMs) are a type of micro special motor widely used in the automotive industry due to their high efficiency and performance. These motors utilize permanent magnets embedded in the rotor, which helps in achieving a constant magnetic field. This design allows PMSMs to operate with high precision and efficiency, making them ideal for applications requiring consistent torque and speed control. In automobiles, PMSMs are commonly used in electric powertrains, where they contribute to the vehicle's propulsion system. Their ability to deliver high torque at low speeds makes them suitable for electric vehicles (EVs), enhancing acceleration and overall performance. Additionally, PMSMs are known for their durability and low maintenance requirements, which are crucial for automotive applications.

Fuel Vehicle, Electric Vehicle in the Micro Special Motor for Automobile - Global Market:

Asynchronous motors, also known as induction motors, are another type of micro special motor used in the automotive sector. Unlike PMSMs, asynchronous motors do not use permanent magnets. Instead, they rely on electromagnetic induction to generate torque. This makes them less expensive to produce, as they do not require rare earth materials for magnets. Asynchronous motors are commonly used in applications where cost-effectiveness and robustness are prioritized over efficiency. In the automotive industry, these motors are often found in auxiliary systems such as air conditioning compressors and power steering pumps. Their simple design and reliability make them a popular choice for these applications, although they are generally less efficient than PMSMs.

Micro Special Motor for Automobile - Global Market Outlook:

Other types of micro special motors include brushless DC motors and stepper motors, each offering unique advantages for specific automotive applications. Brushless DC motors are known for their high efficiency and long lifespan, as they eliminate the need for brushes, reducing wear and tear. These motors are often used in applications requiring precise speed and position control, such as in electric power steering and advanced driver-assistance systems. Stepper motors, on the other hand, are used in applications that require precise positioning and repeatability, such as in throttle control and headlight adjustment systems. The choice of motor type depends on the specific requirements of the application, including factors such as cost, efficiency, and performance. As the automotive industry continues to evolve, the demand for specialized motors that can meet the diverse needs of modern vehicles is expected to grow, driving innovation and development in the micro special motor market.

| Report Metric | Details |

| Report Name | Micro Special Motor for Automobile - Market |

| Forecasted market size in 2030 | US$ 4114.1 million |

| CAGR | 5.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nidec Corporation, MinebeaMitsumi, Mabuchi Motor, Johnson Electric Group, Tokyo Parts, Mitsuba Corporation, Shinano Motor, Mitsumi Electric, Brose, Denso |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |