What is Roasted Seeds and Nuts - Global Market?

Roasted seeds and nuts have become a staple in the global market, offering a nutritious and convenient snack option for consumers worldwide. These products are derived from various seeds and nuts, such as sunflower seeds, pumpkin seeds, almonds, cashews, and peanuts, which are roasted to enhance their flavor and texture. The roasting process not only improves taste but also extends shelf life, making them a popular choice for health-conscious individuals seeking a quick and satisfying snack. The global market for roasted seeds and nuts is driven by increasing awareness of their health benefits, including high protein content, healthy fats, and essential vitamins and minerals. Additionally, the growing trend of plant-based diets and the demand for natural and organic products have further fueled the market's expansion. As consumers continue to prioritize health and wellness, the roasted seeds and nuts market is expected to see sustained growth, with innovations in flavors and packaging catering to diverse consumer preferences.

Seed Nuts, Tree Nuts in the Roasted Seeds and Nuts - Global Market:

Seed nuts and tree nuts play a significant role in the roasted seeds and nuts global market, each offering unique nutritional benefits and culinary applications. Seed nuts, such as sunflower seeds and pumpkin seeds, are derived from the seeds of flowering plants. These seeds are rich in essential nutrients like magnesium, zinc, and vitamin E, making them a popular choice for health-conscious consumers. Sunflower seeds, for instance, are known for their high vitamin E content, which acts as a powerful antioxidant, while pumpkin seeds are celebrated for their magnesium and zinc levels, supporting bone health and immune function. On the other hand, tree nuts, including almonds, cashews, and walnuts, are sourced from the seeds of trees. These nuts are renowned for their heart-healthy fats, protein, and fiber content. Almonds, for example, are a rich source of monounsaturated fats, which have been linked to reduced risk of heart disease, while walnuts are packed with omega-3 fatty acids, known for their anti-inflammatory properties. The roasting process enhances the flavor and texture of both seed nuts and tree nuts, making them a versatile ingredient in various culinary applications. From being a standalone snack to being incorporated into granolas, salads, and baked goods, roasted seeds and nuts offer a delightful crunch and a burst of flavor. The global market for roasted seeds and nuts is witnessing a surge in demand due to the increasing popularity of plant-based diets and the growing awareness of the health benefits associated with these nutrient-dense foods. As consumers become more health-conscious, they are seeking out snacks that not only satisfy their taste buds but also provide essential nutrients. This shift in consumer preferences has led to an increase in the availability of roasted seeds and nuts in various forms, including flavored, unsalted, and organic options. Moreover, the convenience factor of roasted seeds and nuts cannot be overlooked. With busy lifestyles becoming the norm, consumers are gravitating towards snacks that are easy to carry and consume on the go. Roasted seeds and nuts fit this bill perfectly, offering a quick and nutritious snack option that can be enjoyed anytime, anywhere. The global market for roasted seeds and nuts is also benefiting from the rise of e-commerce, with online retailers offering a wide range of products to cater to diverse consumer preferences. This has made it easier for consumers to access a variety of roasted seeds and nuts, further driving market growth. In conclusion, seed nuts and tree nuts are integral components of the roasted seeds and nuts global market, offering a plethora of health benefits and culinary versatility. As consumers continue to prioritize health and wellness, the demand for these nutrient-rich snacks is expected to grow, with innovations in flavors and packaging catering to evolving consumer preferences.

Hypermarkets and Supermarkets, Convenience Stores, Grocery Stores, Online Retailers, Others in the Roasted Seeds and Nuts - Global Market:

The usage of roasted seeds and nuts in various retail channels such as hypermarkets and supermarkets, convenience stores, grocery stores, online retailers, and others plays a crucial role in the global market's expansion. Hypermarkets and supermarkets are major distribution channels for roasted seeds and nuts, offering a wide range of products to cater to diverse consumer preferences. These large retail outlets provide consumers with the convenience of one-stop shopping, where they can find an extensive selection of roasted seeds and nuts, including different flavors, packaging sizes, and brands. The availability of roasted seeds and nuts in hypermarkets and supermarkets is further enhanced by strategic product placement, promotional offers, and in-store sampling, which encourage consumers to try new products and make informed purchasing decisions. Convenience stores, on the other hand, cater to consumers seeking quick and easy snack options. The compact size and strategic locations of convenience stores make them an ideal choice for consumers looking for on-the-go snacks. Roasted seeds and nuts, with their convenient packaging and portability, fit perfectly into this retail channel, offering consumers a nutritious and satisfying snack option that can be easily consumed while on the move. Grocery stores also play a significant role in the distribution of roasted seeds and nuts, providing consumers with a more personalized shopping experience. These stores often focus on offering a curated selection of products, including locally sourced and organic options, catering to health-conscious consumers seeking high-quality snacks. The presence of roasted seeds and nuts in grocery stores is further supported by knowledgeable staff who can provide consumers with information on the nutritional benefits and culinary uses of these products. Online retailers have emerged as a key distribution channel for roasted seeds and nuts, driven by the increasing popularity of e-commerce and the convenience it offers. Consumers can easily browse and purchase a wide range of roasted seeds and nuts from the comfort of their homes, with the added benefit of home delivery. Online platforms also provide consumers with access to a broader selection of products, including niche and specialty items that may not be available in physical stores. The rise of online retailers has also facilitated the growth of direct-to-consumer brands, which offer unique and innovative roasted seed and nut products, further driving market expansion. Other retail channels, such as health food stores and specialty shops, also contribute to the distribution of roasted seeds and nuts, catering to consumers with specific dietary preferences and requirements. These stores often focus on offering high-quality, organic, and non-GMO products, appealing to health-conscious consumers seeking premium snacks. In conclusion, the distribution of roasted seeds and nuts across various retail channels plays a vital role in the global market's growth, providing consumers with convenient access to a wide range of products that cater to diverse preferences and dietary needs.

Roasted Seeds and Nuts - Global Market Outlook:

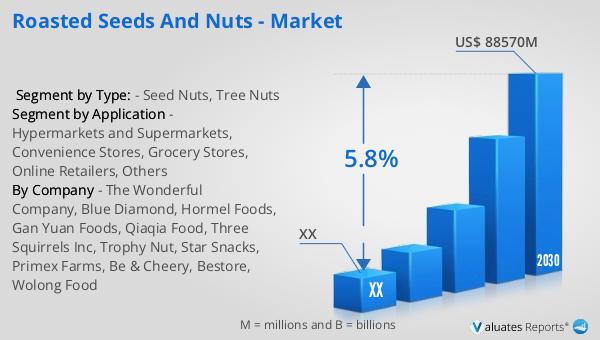

The global market for roasted seeds and nuts was valued at approximately $59,810 million in 2023, and it is projected to grow to a revised size of $88,570 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing consumer demand for healthy and convenient snack options, as well as the rising awareness of the nutritional benefits associated with roasted seeds and nuts. The North American market, in particular, is expected to experience significant growth, driven by the region's health-conscious consumers and the growing popularity of plant-based diets. Although specific figures for the North American market were not provided, it is anticipated that the region will contribute substantially to the overall market expansion. The projected growth of the roasted seeds and nuts market can be attributed to several factors, including the increasing availability of these products in various retail channels, the rise of e-commerce, and the growing trend of health and wellness among consumers. As the market continues to evolve, manufacturers and retailers are likely to focus on product innovation, flavor diversification, and sustainable packaging solutions to meet the changing preferences and demands of consumers. In conclusion, the global market for roasted seeds and nuts is poised for significant growth in the coming years, driven by the increasing consumer demand for nutritious and convenient snack options.

| Report Metric | Details |

| Report Name | Roasted Seeds and Nuts - Market |

| Forecasted market size in 2030 | US$ 88570 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | The Wonderful Company, Blue Diamond, Hormel Foods, Gan Yuan Foods, Qiaqia Food, Three Squirrels Inc, Trophy Nut, Star Snacks, Primex Farms, Be & Cheery, Bestore, Wolong Food |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |