What is Commodity Adhesive Tapes - Global Market?

Commodity adhesive tapes are a vital component in various industries worldwide, serving as essential tools for bonding, sealing, and packaging. These tapes are made from different materials, including paper, plastic, and fabric, and are coated with adhesives to ensure they stick effectively to surfaces. The global market for commodity adhesive tapes is vast and diverse, catering to numerous applications across sectors such as automotive, construction, healthcare, and consumer goods. The demand for these tapes is driven by their versatility, ease of use, and cost-effectiveness. They are used in everyday tasks like sealing boxes, bundling items, and even in specialized applications like medical dressings and automotive assembly. The market is characterized by continuous innovation, with manufacturers developing tapes that offer enhanced performance, such as increased adhesion strength, temperature resistance, and environmental sustainability. As industries continue to grow and evolve, the need for reliable and efficient adhesive solutions remains critical, ensuring the steady expansion of the commodity adhesive tapes market globally.

Acrylic, Rubber, Silicone, Others [EVA and Butyl] in the Commodity Adhesive Tapes - Global Market:

Acrylic, rubber, silicone, and other materials like EVA and butyl are the primary adhesive types used in the production of commodity adhesive tapes, each offering unique properties that cater to specific applications. Acrylic adhesives are known for their excellent aging properties, UV resistance, and ability to adhere to a wide range of surfaces, making them ideal for outdoor applications and long-term use. They are often used in packaging, automotive, and construction industries where durability and resistance to environmental factors are crucial. Rubber adhesives, on the other hand, provide strong initial tack and are cost-effective, making them suitable for general-purpose applications such as carton sealing and bundling. They are preferred in situations where quick adhesion is needed, but they may not perform as well in extreme temperatures or prolonged exposure to sunlight. Silicone adhesives are prized for their exceptional temperature resistance and flexibility, which makes them suitable for high-performance applications in industries like electronics and aerospace. They can withstand extreme temperatures and harsh environments, providing reliable adhesion in challenging conditions. Other adhesives like EVA (ethylene-vinyl acetate) and butyl are used for specific applications where their unique properties are required. EVA adhesives offer good flexibility and are often used in packaging and footwear industries, while butyl adhesives provide excellent moisture resistance, making them ideal for sealing and insulation applications. Each adhesive type brings its own set of advantages and limitations, and the choice of adhesive depends on the specific requirements of the application, such as the type of surface, environmental conditions, and desired performance characteristics. Manufacturers continue to innovate and develop new adhesive formulations to meet the evolving needs of various industries, ensuring that commodity adhesive tapes remain a versatile and indispensable tool in the global market.

Packaging, Masking, Consumer & Office in the Commodity Adhesive Tapes - Global Market:

Commodity adhesive tapes play a crucial role in various applications, particularly in packaging, masking, and consumer and office use. In the packaging industry, these tapes are indispensable for sealing boxes, securing packages, and bundling items for transportation and storage. Their strong adhesion and durability ensure that packages remain intact during transit, protecting the contents from damage. Packaging tapes are available in various materials and adhesive types, allowing them to cater to different packaging needs, from lightweight parcels to heavy-duty shipments. In masking applications, adhesive tapes are used to protect surfaces during painting, coating, or blasting processes. They provide a clean edge and prevent paint bleed, ensuring a professional finish. Masking tapes are designed to adhere well to surfaces but can be easily removed without leaving residue, making them ideal for temporary applications. In consumer and office settings, adhesive tapes are used for a wide range of tasks, from wrapping gifts and sealing envelopes to mounting posters and repairing torn documents. Their versatility and ease of use make them a staple in homes and offices worldwide. Specialty tapes, such as double-sided and transparent tapes, offer additional functionality for specific tasks, such as crafting and decorating. The demand for commodity adhesive tapes in these areas is driven by their convenience, reliability, and cost-effectiveness, making them an essential tool for everyday use. As industries and consumers continue to seek efficient and practical solutions for their adhesive needs, the market for commodity adhesive tapes is expected to grow, driven by innovation and the development of new products that cater to evolving demands.

Commodity Adhesive Tapes - Global Market Outlook:

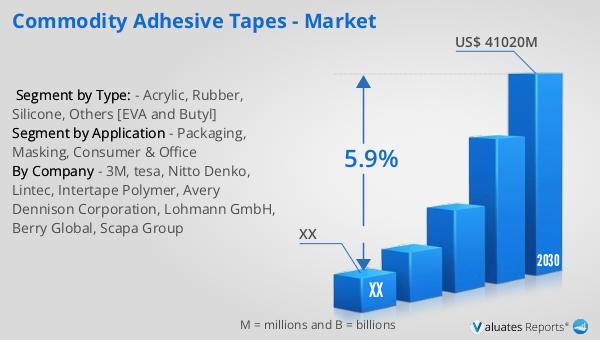

The global market for commodity adhesive tapes was valued at approximately $27,620 million in 2023, with projections indicating a growth to around $41,020 million by 2030. This represents a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for adhesive solutions across various industries, including packaging, automotive, construction, and healthcare. The North American market, a significant contributor to the global landscape, was valued at $ million in 2023, with expectations of reaching $ million by 2030. The growth in this region is attributed to the robust industrial base, technological advancements, and the rising need for efficient and reliable adhesive products. The market dynamics are influenced by factors such as the development of eco-friendly adhesives, the expansion of e-commerce, and the increasing focus on sustainability. As industries continue to evolve and adapt to changing consumer preferences and regulatory requirements, the demand for innovative adhesive solutions is expected to rise, driving the growth of the commodity adhesive tapes market globally.

| Report Metric | Details |

| Report Name | Commodity Adhesive Tapes - Market |

| Forecasted market size in 2030 | US$ 41020 million |

| CAGR | 5.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3M, tesa, Nitto Denko, Lintec, Intertape Polymer, Avery Dennison Corporation, Lohmann GmbH, Berry Global, Scapa Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |