What is Benchtop Dental Air Polisher - Global Market?

The Benchtop Dental Air Polisher is a specialized dental device used globally for cleaning and polishing teeth. It operates by using a combination of air, water, and a fine powder to remove plaque, stains, and other debris from the surface of teeth. This tool is particularly effective in reaching areas that traditional cleaning methods might miss, such as the spaces between teeth and along the gum line. The global market for benchtop dental air polishers is expanding as more dental professionals recognize the benefits of this technology in providing thorough and efficient dental care. The device is valued for its ability to enhance patient comfort and reduce the time required for dental cleaning procedures. As dental health awareness increases worldwide, the demand for advanced dental care tools like the benchtop dental air polisher is expected to grow, making it an essential component in modern dental practices. This growth is driven by technological advancements, increasing dental care expenditure, and a rising focus on preventive dental care. The benchtop dental air polisher is becoming a staple in dental clinics and hospitals, contributing to improved oral health outcomes globally.

Abrasion Polishing, Erosion Polishing in the Benchtop Dental Air Polisher - Global Market:

Abrasion polishing and erosion polishing are two key techniques employed by benchtop dental air polishers in the global market. Abrasion polishing involves the mechanical removal of surface material from the teeth using a stream of air, water, and abrasive powder. This method is particularly effective for removing stubborn stains and plaque that are resistant to traditional brushing and scaling. The abrasive powder, often made from sodium bicarbonate or glycine, is gentle enough to avoid damaging the enamel while being effective in cleaning. Abrasion polishing is favored for its ability to quickly and efficiently clean teeth, making it a popular choice in dental clinics worldwide. On the other hand, erosion polishing utilizes a similar mechanism but focuses more on the chemical interaction between the polishing powder and the tooth surface. This method is designed to soften and remove surface deposits through a controlled chemical reaction, which can be particularly useful for patients with sensitive teeth or those requiring a gentler cleaning approach. Erosion polishing is often used in conjunction with abrasion polishing to provide a comprehensive cleaning experience. The global market for benchtop dental air polishers is witnessing a growing demand for these techniques as they offer a non-invasive, efficient, and patient-friendly alternative to traditional dental cleaning methods. Dental professionals are increasingly adopting these technologies to enhance patient care and improve oral hygiene outcomes. The versatility of benchtop dental air polishers in offering both abrasion and erosion polishing makes them a valuable tool in modern dentistry. As the global market continues to evolve, manufacturers are focusing on developing more advanced and user-friendly devices that cater to the diverse needs of dental practitioners. This includes innovations in powder formulations, ergonomic designs, and enhanced control features to ensure optimal performance and patient comfort. The integration of digital technologies and smart features is also becoming a trend in the market, allowing for more precise and customizable polishing procedures. As a result, the benchtop dental air polisher market is poised for significant growth, driven by the increasing demand for advanced dental care solutions and the continuous advancements in dental technology. The adoption of these polishing techniques is not only improving the efficiency of dental cleaning procedures but also contributing to better oral health outcomes for patients worldwide.

Hospitals, Dental Clinics, Other in the Benchtop Dental Air Polisher - Global Market:

The usage of benchtop dental air polishers in hospitals, dental clinics, and other settings is becoming increasingly prevalent as the global market for these devices expands. In hospitals, benchtop dental air polishers are used primarily in dental departments to provide comprehensive oral care to patients. These devices are particularly useful in hospital settings where patients may have limited mobility or require specialized care. The ability of benchtop dental air polishers to efficiently remove plaque and stains without causing discomfort makes them an ideal choice for hospital dental care. Additionally, the use of these devices in hospitals helps to reduce the risk of cross-contamination and infection, as they are designed to be easily sterilized and maintained. In dental clinics, benchtop dental air polishers are a staple tool for dental hygienists and dentists. They are used to perform routine cleanings, remove stubborn stains, and prepare teeth for further dental procedures such as bonding or whitening. The versatility and efficiency of these devices make them an essential component of modern dental practice. Dental clinics benefit from the time-saving capabilities of benchtop dental air polishers, allowing them to serve more patients and improve overall patient satisfaction. The gentle yet effective cleaning action of these devices also enhances patient comfort, making dental visits a more pleasant experience. Beyond hospitals and dental clinics, benchtop dental air polishers are also used in other settings such as dental schools, research institutions, and mobile dental units. In dental schools, these devices are used to train future dental professionals in the latest dental care techniques. Research institutions utilize benchtop dental air polishers to study the effects of various polishing powders and techniques on dental health. Mobile dental units, which provide dental care to underserved communities, rely on the portability and efficiency of benchtop dental air polishers to deliver high-quality care in remote locations. The global market for benchtop dental air polishers is driven by the increasing demand for advanced dental care solutions across these various settings. As dental health awareness continues to rise, the adoption of benchtop dental air polishers is expected to grow, contributing to improved oral health outcomes worldwide. The versatility, efficiency, and patient-friendly nature of these devices make them an invaluable tool in the pursuit of better dental care.

Benchtop Dental Air Polisher - Global Market Outlook:

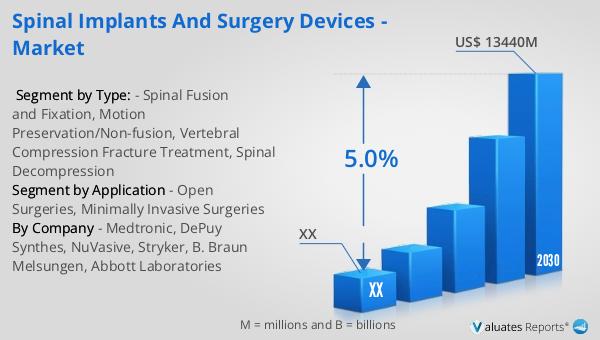

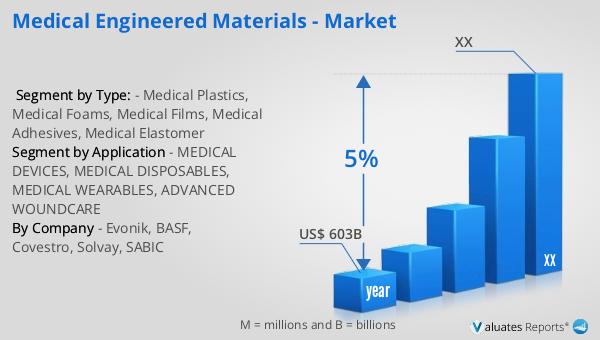

Based on our research, the global market for medical devices, which includes benchtop dental air polishers, is projected to reach approximately $603 billion by the year 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for advanced medical technologies and devices across various healthcare sectors. The benchtop dental air polisher market is a part of this larger medical device market, benefiting from the overall expansion and technological advancements in the industry. As dental professionals and healthcare providers continue to seek innovative solutions to improve patient care and outcomes, the demand for efficient and effective dental devices like benchtop dental air polishers is expected to rise. The projected growth of the medical device market reflects the ongoing efforts to enhance healthcare delivery and address the evolving needs of patients worldwide. With the continuous development of new technologies and the increasing focus on preventive care, the global market for medical devices, including benchtop dental air polishers, is poised for significant growth in the coming years. This growth presents opportunities for manufacturers and healthcare providers to invest in and adopt cutting-edge dental technologies that can improve patient care and contribute to better oral health outcomes.

| Report Metric | Details |

| Report Name | Benchtop Dental Air Polisher - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kavo, NSK, EMS, W&H, Dentsply Sirona, ACTEON, Dürr Dental, Hu-Friedy, Mectron, Deldent, LM-Dental, MK-dent, MICRON, TPC Advanced |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |