What is Road Bicycle Light - Global Market?

The global market for road bicycle lights is a dynamic and evolving sector, driven by the increasing popularity of cycling as both a recreational activity and a mode of transportation. Road bicycle lights are essential safety accessories that enhance visibility and safety for cyclists, especially during low-light conditions or nighttime riding. These lights are typically mounted on the front and rear of bicycles, providing illumination and signaling to other road users. The market encompasses a wide range of products, including headlights, taillights, and combination light sets, each designed to meet specific needs and preferences of cyclists. Technological advancements have led to the development of more efficient and durable lights, with features such as rechargeable batteries, multiple lighting modes, and weather-resistant designs. The growing awareness of the importance of road safety, coupled with the increasing adoption of cycling for commuting and fitness, is expected to drive the demand for road bicycle lights globally. As urban areas continue to promote cycling infrastructure and sustainable transportation, the market for road bicycle lights is poised for steady growth, offering opportunities for manufacturers to innovate and cater to the diverse needs of cyclists worldwide.

Headlight, Taillight in the Road Bicycle Light - Global Market:

Headlights and taillights are critical components of road bicycle lights, serving distinct yet complementary functions to ensure cyclist safety. Headlights are mounted on the front of the bicycle and are primarily designed to illuminate the path ahead, allowing cyclists to see obstacles, road conditions, and potential hazards. They also make cyclists more visible to oncoming traffic, reducing the risk of accidents. Modern bicycle headlights come with various features, such as adjustable brightness levels, different beam patterns, and rechargeable batteries, catering to the diverse needs of cyclists. Some advanced models even offer smart features like automatic brightness adjustment based on ambient light conditions and connectivity with mobile apps for customization. On the other hand, taillights are mounted on the rear of the bicycle and are primarily designed to alert other road users to the presence of the cyclist. They typically emit a bright red light, which is easily recognizable and can be seen from a distance. Like headlights, taillights also come with various features, including multiple lighting modes (steady, flashing, pulsing), long battery life, and weather-resistant designs. Some taillights are equipped with motion sensors that activate the light when the bicycle is in motion, enhancing visibility during sudden stops or turns. The integration of LED technology in both headlights and taillights has significantly improved their efficiency, brightness, and longevity, making them more reliable and cost-effective for cyclists. The global market for road bicycle lights, including headlights and taillights, is influenced by several factors, such as technological advancements, consumer preferences, and regulatory standards. Manufacturers are continually innovating to develop lights that offer better performance, longer battery life, and enhanced safety features. The increasing emphasis on road safety and the growing popularity of cycling as a sustainable mode of transportation are driving the demand for high-quality bicycle lights. Additionally, the rise of e-commerce platforms has made it easier for consumers to access a wide range of bicycle lights, compare features, and make informed purchasing decisions. As the market continues to evolve, manufacturers are likely to focus on developing products that cater to the specific needs of different segments of cyclists, such as commuters, recreational riders, and professional athletes. This includes offering a variety of designs, price points, and features to meet the diverse preferences and budgets of consumers. Overall, the global market for road bicycle lights, including headlights and taillights, is expected to witness steady growth, driven by the increasing awareness of road safety, technological advancements, and the growing adoption of cycling as a preferred mode of transportation.

Offlines, Onlines in the Road Bicycle Light - Global Market:

The usage of road bicycle lights in offline and online markets reflects the diverse ways consumers access and purchase these essential safety accessories. In offline markets, road bicycle lights are typically available in specialty bike shops, sporting goods stores, and large retail chains. These physical stores offer consumers the opportunity to see and test the products before making a purchase, providing a tactile shopping experience that many consumers value. Sales representatives in these stores can offer personalized advice and recommendations based on the specific needs and preferences of the customer, enhancing the overall shopping experience. Additionally, offline markets often host events, workshops, and demonstrations that educate consumers about the importance of bicycle safety and the role of lights in ensuring visibility on the road. These initiatives help raise awareness and drive demand for road bicycle lights among cyclists of all levels. On the other hand, the online market for road bicycle lights has grown significantly in recent years, driven by the convenience and accessibility of e-commerce platforms. Online retailers offer a vast selection of bicycle lights, allowing consumers to compare features, prices, and customer reviews from the comfort of their homes. This ease of access has made it possible for consumers to find products that meet their specific needs and preferences, often at competitive prices. The online market also benefits from the ability to reach a global audience, enabling manufacturers to expand their customer base beyond local markets. Social media platforms and online forums play a crucial role in influencing consumer purchasing decisions, as cyclists often share their experiences and recommendations with a wider community. This digital word-of-mouth marketing can significantly impact the popularity and sales of specific bicycle light brands and models. Furthermore, online platforms often offer promotions, discounts, and bundle deals that attract price-sensitive consumers, further driving the demand for road bicycle lights. As the global market for road bicycle lights continues to evolve, the interplay between offline and online markets will play a crucial role in shaping consumer behavior and preferences. Manufacturers and retailers must adapt to the changing landscape by offering a seamless shopping experience across both channels, ensuring that consumers have access to high-quality products and reliable information. By leveraging the strengths of both offline and online markets, the road bicycle light industry can continue to grow and meet the diverse needs of cyclists worldwide.

Road Bicycle Light - Global Market Outlook:

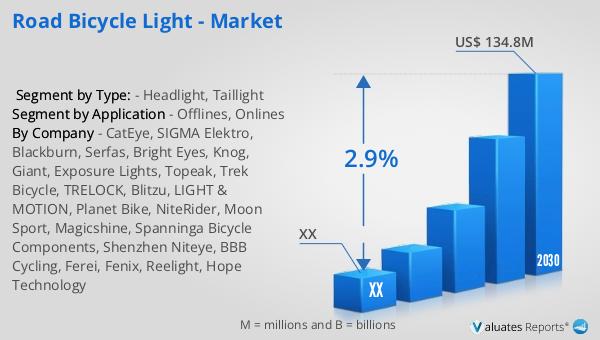

The global market for road bicycle lights was valued at approximately $110.7 million in 2023 and is projected to grow to around $134.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.9% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for road bicycle lights as more people embrace cycling for commuting, fitness, and recreation. The market's expansion is driven by factors such as technological advancements in lighting solutions, heightened awareness of road safety, and the growing popularity of cycling as a sustainable mode of transportation. In North America, the market for road bicycle lights is also expected to witness growth, although specific figures for 2023 and 2030 are not provided. The region's market dynamics are influenced by similar factors, including the increasing adoption of cycling infrastructure and the emphasis on safety measures for cyclists. As urban areas continue to promote cycling-friendly environments, the demand for high-quality road bicycle lights is likely to rise, offering opportunities for manufacturers to innovate and cater to the diverse needs of cyclists. Overall, the global market outlook for road bicycle lights is positive, with steady growth anticipated over the coming years.

| Report Metric | Details |

| Report Name | Road Bicycle Light - Market |

| Forecasted market size in 2030 | US$ 134.8 million |

| CAGR | 2.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | CatEye, SIGMA Elektro, Blackburn, Serfas, Bright Eyes, Knog, Giant, Exposure Lights, Topeak, Trek Bicycle, TRELOCK, Blitzu, LIGHT & MOTION, Planet Bike, NiteRider, Moon Sport, Magicshine, Spanninga Bicycle Components, Shenzhen Niteye, BBB Cycling, Ferei, Fenix, Reelight, Hope Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |