What is Global Logstics Automation Solutions Market?

The Global Logistics Automation Solutions Market refers to the integration of advanced technologies and automated systems in the logistics sector to enhance efficiency, accuracy, and speed in the movement and storage of goods. This market encompasses a wide range of solutions, including automated storage and retrieval systems, robotics, conveyor systems, and software solutions that streamline logistics operations. The primary goal of logistics automation is to reduce human intervention, minimize errors, and optimize the supply chain process. By leveraging technologies such as artificial intelligence, machine learning, and the Internet of Things (IoT), logistics automation solutions enable companies to manage their inventory more effectively, improve order accuracy, and reduce operational costs. These solutions are increasingly being adopted across various industries, including retail, manufacturing, and e-commerce, as businesses strive to meet the growing demand for faster and more reliable delivery services. The market is driven by the need for operational efficiency, the rise of e-commerce, and the increasing complexity of supply chains. As companies continue to invest in automation technologies, the Global Logistics Automation Solutions Market is expected to experience significant growth in the coming years.

One Stop Solutions, Modular Solutions in the Global Logstics Automation Solutions Market:

In the realm of Global Logistics Automation Solutions, two prominent approaches are One Stop Solutions and Modular Solutions. One Stop Solutions refer to comprehensive packages that provide end-to-end automation services, covering all aspects of logistics operations from warehousing to transportation. These solutions are designed to offer a seamless integration of various technologies and systems, ensuring that all logistics processes are automated and optimized under a single umbrella. Companies opting for One Stop Solutions benefit from a unified platform that simplifies management, reduces the need for multiple vendors, and ensures compatibility across different systems. This approach is particularly advantageous for large enterprises with complex logistics needs, as it provides a holistic solution that addresses all facets of their supply chain. On the other hand, Modular Solutions offer a more flexible and customizable approach to logistics automation. These solutions allow companies to select and implement specific automation technologies based on their unique requirements and operational challenges. Modular Solutions are ideal for businesses that prefer a phased approach to automation, enabling them to gradually integrate new technologies without disrupting existing operations. This approach provides the flexibility to scale and adapt to changing business needs, making it suitable for companies of all sizes. By choosing Modular Solutions, businesses can focus on automating specific areas of their logistics operations, such as inventory management or order fulfillment, and expand their automation capabilities as needed. Both One Stop and Modular Solutions have their own set of advantages and are chosen based on the specific needs and goals of a business. One Stop Solutions are often favored by companies looking for a comprehensive and integrated approach to logistics automation, while Modular Solutions are preferred by those seeking flexibility and customization. The choice between these two approaches depends on factors such as the size of the business, the complexity of its logistics operations, and its long-term automation strategy. As the Global Logistics Automation Solutions Market continues to evolve, businesses are increasingly exploring these options to enhance their operational efficiency and gain a competitive edge in the market.

Automotive Manufacturing, Chemical Manufacturing, Food Industry, Others in the Global Logstics Automation Solutions Market:

The Global Logistics Automation Solutions Market plays a crucial role in various industries, including automotive manufacturing, chemical manufacturing, the food industry, and others. In automotive manufacturing, logistics automation solutions are used to streamline the supply chain, manage inventory, and ensure timely delivery of parts and components. Automated systems such as robotic arms and conveyor belts are employed to handle materials efficiently, reducing the risk of errors and delays. These solutions also facilitate real-time tracking and monitoring of shipments, enabling manufacturers to optimize their production schedules and meet customer demands more effectively. In chemical manufacturing, logistics automation solutions are essential for managing the complex and often hazardous supply chains associated with chemical products. Automated systems help in the safe handling and transportation of chemicals, minimizing the risk of spills and contamination. These solutions also enhance inventory management by providing accurate data on stock levels and enabling efficient order processing. By automating logistics operations, chemical manufacturers can improve safety, reduce operational costs, and ensure compliance with regulatory requirements. The food industry also benefits significantly from logistics automation solutions. With the increasing demand for fresh and perishable products, efficient logistics operations are critical to maintaining product quality and safety. Automated systems such as temperature-controlled storage and transportation solutions help in preserving the freshness of food products during transit. Additionally, logistics automation solutions enable food manufacturers to manage their supply chains more effectively, ensuring timely delivery of products to retailers and consumers. By optimizing logistics operations, food companies can reduce waste, improve customer satisfaction, and enhance their overall competitiveness in the market. Apart from these industries, logistics automation solutions are also widely used in sectors such as retail, healthcare, and e-commerce. In retail, automated systems help in managing inventory, processing orders, and ensuring timely delivery of products to customers. In healthcare, logistics automation solutions are used to manage the supply chain of medical supplies and equipment, ensuring their availability when needed. In e-commerce, automated systems enable companies to handle large volumes of orders efficiently, providing fast and reliable delivery services to customers. Overall, the Global Logistics Automation Solutions Market is transforming the way businesses operate, enabling them to achieve greater efficiency, accuracy, and speed in their logistics operations.

Global Logstics Automation Solutions Market Outlook:

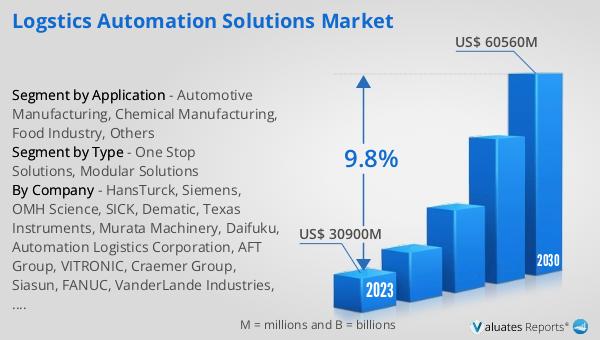

The outlook for the Global Logistics Automation Solutions Market is promising, with significant growth anticipated in the coming years. In 2023, the market was valued at approximately $30.9 billion, and it is projected to reach around $60.56 billion by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 9.8% during the forecast period from 2024 to 2030. This robust growth can be attributed to several factors, including the increasing demand for efficient and reliable logistics operations, the rise of e-commerce, and the growing complexity of supply chains. As businesses strive to meet the evolving needs of their customers, they are increasingly turning to automation solutions to enhance their logistics operations. The adoption of logistics automation solutions is driven by the need to improve operational efficiency, reduce costs, and enhance customer satisfaction. By automating various aspects of logistics operations, companies can streamline their supply chains, minimize errors, and ensure timely delivery of products. This not only improves the overall efficiency of logistics operations but also provides a competitive advantage in the market. As a result, businesses across various industries are investing in logistics automation solutions to stay ahead of the competition and meet the growing demands of their customers. Furthermore, advancements in technology, such as artificial intelligence, machine learning, and the Internet of Things (IoT), are playing a crucial role in driving the growth of the Global Logistics Automation Solutions Market. These technologies enable companies to collect and analyze data in real-time, providing valuable insights into their logistics operations. By leveraging these insights, businesses can make informed decisions, optimize their supply chains, and improve their overall performance. As technology continues to evolve, the adoption of logistics automation solutions is expected to increase, further fueling the growth of the market.

| Report Metric | Details |

| Report Name | Logstics Automation Solutions Market |

| Accounted market size in 2023 | US$ 30900 million |

| Forecasted market size in 2030 | US$ 60560 million |

| CAGR | 9.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | HansTurck, Siemens, OMH Science, SICK, Dematic, Texas Instruments, Murata Machinery, Daifuku, Automation Logistics Corporation, AFT Group, VITRONIC, Craemer Group, Siasun, FANUC, VanderLande Industries, SSI Schaefer, Swisslog, Okamura, Shanghai EOSlift, Tianqi Automation Engineering, Geek Plus, Sanfeng Intelligent Conveying Equipment, Bastian Solutions, Creation Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |