What is Global Ceramic Glow Plugs Market?

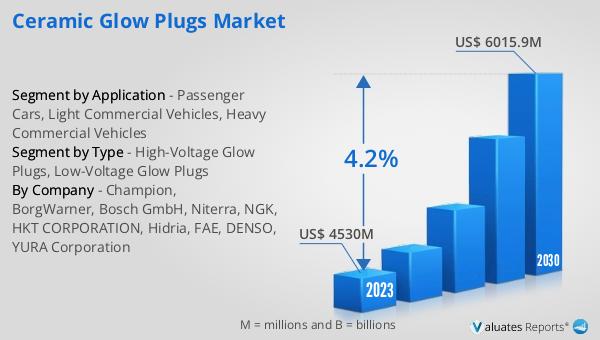

The global Ceramic Glow Plugs market is a specialized segment within the automotive industry, focusing on the production and distribution of ceramic glow plugs. These components are essential for diesel engines, as they help in the ignition process by heating the air-fuel mixture to a temperature high enough to ignite the fuel. Ceramic glow plugs are preferred over traditional metal glow plugs due to their superior heat resistance, faster heating times, and longer lifespan. They are made from advanced ceramic materials that can withstand extreme temperatures and provide consistent performance even in harsh conditions. The market for ceramic glow plugs is driven by the increasing demand for diesel engines in various types of vehicles, including passenger cars, light commercial vehicles, and heavy commercial vehicles. Additionally, stringent emission regulations and the need for fuel-efficient engines are further propelling the growth of this market. The global Ceramic Glow Plugs market was valued at US$ 4530 million in 2023 and is anticipated to reach US$ 6015.9 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030.

High-Voltage Glow Plugs, Low-Voltage Glow Plugs in the Global Ceramic Glow Plugs Market:

High-voltage glow plugs and low-voltage glow plugs are two primary types of ceramic glow plugs used in the global market. High-voltage glow plugs operate at a higher voltage, typically around 11 to 12 volts, and are designed to provide rapid heating and efficient ignition in diesel engines. These glow plugs are particularly beneficial in cold weather conditions, where quick engine start-up is crucial. High-voltage glow plugs are commonly used in modern diesel engines that require high performance and reliability. They are also known for their durability and ability to withstand high temperatures, making them suitable for heavy-duty applications. On the other hand, low-voltage glow plugs operate at a lower voltage, usually around 5 to 6 volts. These glow plugs are designed for engines that do not require rapid heating and can operate efficiently at lower temperatures. Low-voltage glow plugs are typically used in older diesel engines or in applications where quick start-up is not a priority. They are also more cost-effective compared to high-voltage glow plugs, making them a popular choice for budget-conscious consumers. Both high-voltage and low-voltage glow plugs play a crucial role in ensuring the smooth operation of diesel engines, and their usage depends on the specific requirements of the engine and the operating conditions. The choice between high-voltage and low-voltage glow plugs is influenced by factors such as engine design, performance requirements, and environmental conditions. As the demand for diesel engines continues to grow, the market for both high-voltage and low-voltage ceramic glow plugs is expected to expand, driven by advancements in technology and the need for more efficient and reliable ignition systems.

Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles in the Global Ceramic Glow Plugs Market:

The usage of ceramic glow plugs in passenger cars, light commercial vehicles, and heavy commercial vehicles varies based on the specific requirements and operating conditions of each vehicle type. In passenger cars, ceramic glow plugs are essential for ensuring quick and reliable engine start-up, especially in cold weather conditions. These vehicles require glow plugs that can provide rapid heating and consistent performance to ensure a smooth driving experience. Ceramic glow plugs are preferred in passenger cars due to their durability, heat resistance, and ability to provide efficient ignition even in extreme temperatures. In light commercial vehicles, ceramic glow plugs play a crucial role in ensuring the reliability and performance of diesel engines. These vehicles are often used for transporting goods and require engines that can start quickly and operate efficiently under various conditions. Ceramic glow plugs provide the necessary heat to ignite the air-fuel mixture, ensuring that the engine starts smoothly and operates efficiently. The durability and long lifespan of ceramic glow plugs make them an ideal choice for light commercial vehicles, which are often subjected to frequent start-stop cycles and varying load conditions. In heavy commercial vehicles, such as trucks and buses, ceramic glow plugs are essential for ensuring the reliable operation of large diesel engines. These vehicles require glow plugs that can withstand high temperatures and provide consistent performance under heavy load conditions. Ceramic glow plugs are designed to meet these requirements, providing rapid heating and efficient ignition even in the most demanding conditions. The use of ceramic glow plugs in heavy commercial vehicles helps to improve fuel efficiency, reduce emissions, and ensure the reliable operation of the engine. Overall, the usage of ceramic glow plugs in passenger cars, light commercial vehicles, and heavy commercial vehicles is driven by the need for reliable and efficient ignition systems that can operate under various conditions and provide consistent performance.

Global Ceramic Glow Plugs Market Outlook:

The global Ceramic Glow Plugs market was valued at US$ 4530 million in 2023 and is anticipated to reach US$ 6015.9 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This growth is driven by the increasing demand for diesel engines in various types of vehicles, including passenger cars, light commercial vehicles, and heavy commercial vehicles. The superior performance, durability, and heat resistance of ceramic glow plugs make them a preferred choice over traditional metal glow plugs. Additionally, stringent emission regulations and the need for fuel-efficient engines are further propelling the growth of this market. The advancements in technology and the development of high-voltage and low-voltage ceramic glow plugs are also contributing to the expansion of the market. As the demand for diesel engines continues to grow, the market for ceramic glow plugs is expected to witness significant growth during the forecast period.

| Report Metric | Details |

| Report Name | Ceramic Glow Plugs Market |

| Accounted market size in 2023 | US$ 4530 million |

| Forecasted market size in 2030 | US$ 6015.9 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Champion, BorgWarner, Bosch GmbH, Niterra, NGK, HKT CORPORATION, Hidria, FAE, DENSO, YURA Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |