What is Global Ceramic Matrix Composites for Aerospace Market?

Global Ceramic Matrix Composites (CMCs) for the aerospace market are advanced materials designed to withstand extreme conditions encountered in aerospace applications. These composites are made by embedding ceramic fibers into a ceramic matrix, resulting in a material that combines the best properties of both ceramics and composites. CMCs are known for their high-temperature resistance, lightweight nature, and exceptional strength, making them ideal for aerospace components such as turbine blades, exhaust nozzles, and heat shields. The use of CMCs in aerospace helps improve fuel efficiency, reduce emissions, and enhance overall performance. As the aerospace industry continues to push the boundaries of technology, the demand for CMCs is expected to grow, driven by the need for materials that can endure the harsh environments of space and high-speed flight. The global market for CMCs in aerospace is characterized by ongoing research and development, with companies and research institutions striving to develop new formulations and manufacturing techniques to further enhance the properties and applications of these advanced materials.

Oxide, Silicon Carbide, Carbon, Others in the Global Ceramic Matrix Composites for Aerospace Market:

Oxide, Silicon Carbide, Carbon, and other types of Ceramic Matrix Composites (CMCs) play crucial roles in the aerospace market, each offering unique properties that cater to specific applications. Oxide CMCs, typically composed of alumina or zirconia fibers embedded in an oxide matrix, are known for their excellent thermal stability and resistance to oxidation. These properties make them suitable for applications in high-temperature environments, such as turbine engines and exhaust systems, where maintaining structural integrity under extreme heat is critical. Silicon Carbide (SiC) CMCs, on the other hand, are renowned for their exceptional strength, thermal conductivity, and resistance to thermal shock. SiC CMCs are often used in components that require high mechanical performance and durability, such as turbine blades and heat exchangers. Carbon CMCs, which consist of carbon fibers in a carbon matrix, offer high strength-to-weight ratios and excellent thermal and electrical conductivity. These composites are particularly valuable in applications where weight reduction is paramount, such as in spacecraft and high-speed aircraft. Additionally, Carbon CMCs are used in brake systems and other components that require high frictional performance. Other types of CMCs, including those based on boron nitride or silicon nitride, provide specialized properties for niche applications. For instance, boron nitride CMCs offer excellent thermal and chemical stability, making them suitable for use in harsh chemical environments. Silicon nitride CMCs, known for their high fracture toughness and wear resistance, are used in applications that demand high reliability and longevity. The diversity of CMC types allows aerospace engineers to select the most appropriate material for each specific application, optimizing performance and efficiency. The development and utilization of these advanced materials are driven by the continuous pursuit of innovation in the aerospace industry, aiming to achieve higher performance, greater fuel efficiency, and reduced environmental impact. As research and development efforts continue, the range of applications for CMCs in aerospace is expected to expand, further solidifying their importance in the industry.

Commercial, Military in the Global Ceramic Matrix Composites for Aerospace Market:

The usage of Global Ceramic Matrix Composites (CMCs) in the aerospace market spans both commercial and military sectors, each with distinct requirements and applications. In the commercial aerospace sector, CMCs are primarily used to enhance the performance and efficiency of aircraft engines. The high-temperature resistance and lightweight nature of CMCs make them ideal for turbine blades, combustor liners, and exhaust nozzles, where they help improve fuel efficiency and reduce emissions. By enabling engines to operate at higher temperatures, CMCs contribute to better fuel combustion and lower specific fuel consumption, which is crucial for commercial airlines aiming to reduce operational costs and meet stringent environmental regulations. Additionally, CMCs are used in thermal protection systems and heat shields, ensuring the safety and reliability of commercial aircraft during high-speed flight and re-entry into the Earth's atmosphere. In the military aerospace sector, the use of CMCs is driven by the need for advanced materials that can withstand the extreme conditions encountered in defense applications. Military aircraft, including fighter jets and unmanned aerial vehicles (UAVs), benefit from the high strength-to-weight ratio and thermal stability of CMCs. These properties are essential for components such as engine parts, missile casings, and thermal protection systems, where performance and durability are critical. CMCs also play a vital role in enhancing the stealth capabilities of military aircraft by reducing radar cross-sections and improving thermal management. The ability of CMCs to endure high temperatures and harsh environments makes them suitable for use in hypersonic vehicles and other advanced defense systems. Furthermore, the lightweight nature of CMCs contributes to increased payload capacity and extended range for military aircraft, providing strategic advantages in defense operations. The adoption of CMCs in both commercial and military aerospace sectors is driven by the continuous pursuit of innovation and the need to meet evolving performance and environmental standards. As the aerospace industry advances, the role of CMCs is expected to grow, offering new opportunities for enhancing the capabilities and efficiency of both commercial and military aircraft.

Global Ceramic Matrix Composites for Aerospace Market Outlook:

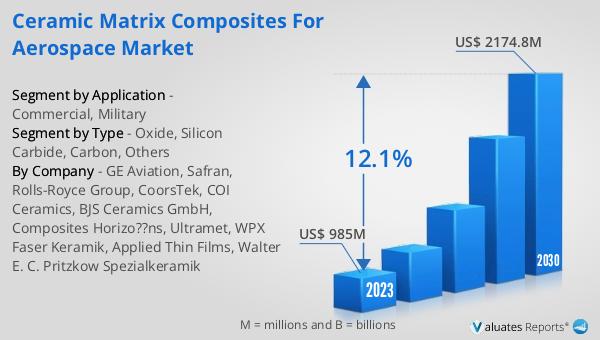

The aerospace and defense industry remains a hub of innovation, driven by the urgent need for modernization and the increasing significance of emerging technologies such as artificial intelligence and unmanned systems. In this dynamic environment, the global Ceramic Matrix Composites (CMCs) for Aerospace market has shown remarkable growth. Valued at US$ 985 million in 2023, the market is projected to reach US$ 2174.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 12.1% during the forecast period from 2024 to 2030. This growth is fueled by the continuous advancements in aerospace technology and the increasing demand for materials that can withstand extreme conditions while offering superior performance. The adoption of CMCs in aerospace applications is driven by their unique properties, including high-temperature resistance, lightweight nature, and exceptional strength, which are essential for improving fuel efficiency, reducing emissions, and enhancing overall performance. As the aerospace industry continues to evolve, the role of CMCs is expected to become even more significant, contributing to the development of next-generation aircraft and defense systems.

| Report Metric | Details |

| Report Name | Ceramic Matrix Composites for Aerospace Market |

| Accounted market size in 2023 | US$ 985 million |

| Forecasted market size in 2030 | US$ 2174.8 million |

| CAGR | 12.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | GE Aviation, Safran, Rolls-Royce Group, CoorsTek, COI Ceramics, BJS Ceramics GmbH, Composites Horizo??ns, Ultramet, WPX Faser Keramik, Applied Thin Films, Walter E. C. Pritzkow Spezialkeramik |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |