What is Global Modular Steel Structure Bathroom Market?

The Global Modular Steel Structure Bathroom Market refers to the industry focused on the production and distribution of pre-fabricated bathroom units made primarily from steel. These modular bathrooms are designed to be easily transported and installed in various types of buildings, offering a convenient and efficient solution for construction projects. The market encompasses a wide range of products, including small, medium, and large-sized bathroom units, catering to different needs and preferences. The use of steel as the primary material ensures durability, strength, and resistance to corrosion, making these bathrooms suitable for various environments. The market is driven by the growing demand for quick and cost-effective construction solutions, particularly in sectors such as hospitality, healthcare, and residential buildings. Additionally, the modular nature of these bathrooms allows for customization and scalability, making them an attractive option for developers and contractors. Overall, the Global Modular Steel Structure Bathroom Market is a dynamic and evolving industry, offering innovative solutions to meet the diverse needs of modern construction projects.

Small Size, Medium Size, Large Size in the Global Modular Steel Structure Bathroom Market:

In the Global Modular Steel Structure Bathroom Market, products are categorized based on their size: small, medium, and large. Small-sized modular steel structure bathrooms are typically designed for compact spaces, such as small apartments, tiny homes, or office buildings with limited space. These units are highly efficient, maximizing the use of available space while providing all the necessary amenities. They are often chosen for their ease of installation and minimal footprint, making them ideal for urban environments where space is at a premium. Medium-sized modular bathrooms, on the other hand, offer a balance between space and functionality. They are suitable for a wide range of applications, including mid-sized residential buildings, hotels, and commercial properties. These units provide more room for fixtures and fittings, allowing for a more comfortable and luxurious bathroom experience. Large-sized modular steel structure bathrooms are designed for spacious environments, such as luxury hotels, large residential homes, and medical institutions. These units offer ample space for multiple fixtures, including bathtubs, showers, and double sinks, providing a high level of comfort and convenience. The large size also allows for greater customization, enabling developers to create unique and personalized bathroom spaces. Each size category in the Global Modular Steel Structure Bathroom Market caters to specific needs and preferences, ensuring that there is a suitable option for every type of construction project. The versatility and adaptability of these modular bathrooms make them a popular choice among developers and contractors, who appreciate the ease of installation, durability, and cost-effectiveness they offer. As the demand for efficient and innovative construction solutions continues to grow, the market for modular steel structure bathrooms is expected to expand, offering even more options and features to meet the diverse needs of modern construction projects.

Hotel, Medical Institutions, Civilian, Other in the Global Modular Steel Structure Bathroom Market:

The Global Modular Steel Structure Bathroom Market finds extensive usage across various sectors, including hotels, medical institutions, civilian applications, and other areas. In the hotel industry, modular steel structure bathrooms are highly valued for their efficiency and ease of installation. Hotels often require quick and cost-effective construction solutions to minimize downtime and maximize occupancy rates. Modular bathrooms provide a perfect solution, allowing for rapid installation and immediate use. They also offer a high level of customization, enabling hotel developers to create unique and luxurious bathroom experiences for their guests. In medical institutions, such as hospitals and clinics, modular steel structure bathrooms are used to ensure hygiene, durability, and ease of maintenance. These bathrooms are designed to meet strict health and safety standards, providing a clean and safe environment for patients and staff. The use of steel as the primary material ensures that these bathrooms are resistant to corrosion and wear, making them ideal for high-traffic areas. In civilian applications, modular steel structure bathrooms are used in residential buildings, office spaces, and public facilities. They offer a convenient and cost-effective solution for new construction projects and renovations, providing all the necessary amenities in a compact and efficient design. The modular nature of these bathrooms allows for easy installation and scalability, making them suitable for a wide range of applications. Other areas where modular steel structure bathrooms are used include temporary housing, disaster relief shelters, and military installations. In these situations, the quick and easy installation of modular bathrooms is crucial, providing essential facilities in a timely and efficient manner. Overall, the Global Modular Steel Structure Bathroom Market offers versatile and innovative solutions for various sectors, meeting the diverse needs of modern construction projects.

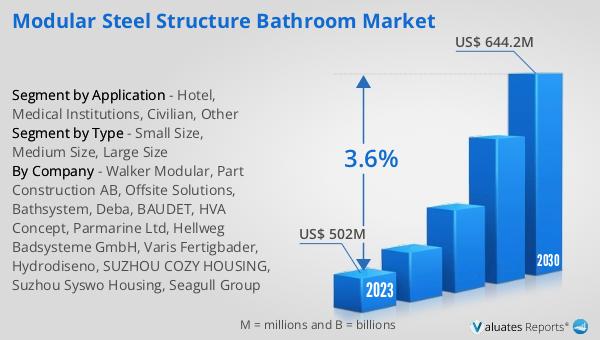

Global Modular Steel Structure Bathroom Market Outlook:

The outlook for the Global Modular Steel Structure Bathroom Market is promising. In 2023, the market was valued at approximately US$ 502 million. By 2030, it is expected to grow to around US$ 644.2 million, reflecting a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for efficient and cost-effective construction solutions across various sectors, including hospitality, healthcare, and residential buildings. The modular nature of these bathrooms, combined with the durability and strength of steel, makes them an attractive option for developers and contractors. As the market continues to evolve, it is expected to offer even more innovative and customizable solutions to meet the diverse needs of modern construction projects. The steady growth in the market value indicates a positive trend, highlighting the potential for further expansion and development in the coming years.

| Report Metric | Details |

| Report Name | Modular Steel Structure Bathroom Market |

| Accounted market size in 2023 | US$ 502 million |

| Forecasted market size in 2030 | US$ 644.2 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Walker Modular, Part Construction AB, Offsite Solutions, Bathsystem, Deba, BAUDET, HVA Concept, Parmarine Ltd, Hellweg Badsysteme GmbH, Varis Fertigbader, Hydrodiseno, SUZHOU COZY HOUSING, Suzhou Syswo Housing, Seagull Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |