What is Global Polymeric Bromide Market?

The Global Polymeric Bromide Market refers to the worldwide industry involved in the production, distribution, and application of polymeric bromides. These are chemical compounds that contain bromine atoms bonded to polymer chains. Polymeric bromides are used in various industries due to their unique properties, such as flame retardancy, chemical stability, and high thermal resistance. The market encompasses a range of products, including polyvinyl bromide and polybrominated biphenyls, which are utilized in applications like flame retardants, PTA synthesis, plasma etching, and mercury removal. The demand for polymeric bromides is driven by their effectiveness in enhancing the safety and performance of materials used in electronics, textiles, automotive, and other sectors. The market is influenced by factors such as regulatory policies, technological advancements, and the growing need for safer and more efficient materials. As industries continue to seek innovative solutions to meet safety and performance standards, the Global Polymeric Bromide Market is expected to evolve and expand, offering new opportunities for manufacturers and consumers alike.

Polyvinyl Bromide, Polybrominated Biphenyls in the Global Polymeric Bromide Market:

Polyvinyl Bromide (PVB) and Polybrominated Biphenyls (PBBs) are two significant types of polymeric bromides that play crucial roles in the Global Polymeric Bromide Market. Polyvinyl Bromide is a polymer that incorporates bromine atoms into its structure, providing it with enhanced flame retardant properties. This makes PVB an essential material in industries where fire safety is paramount, such as in the manufacturing of electrical cables, construction materials, and textiles. PVB is also known for its chemical resistance and durability, making it suitable for various industrial applications. On the other hand, Polybrominated Biphenyls are a group of brominated flame retardants that have been widely used in the past. PBBs are effective in reducing the flammability of materials, which is why they were commonly used in plastics, electronics, and textiles. However, due to their persistence in the environment and potential health risks, the use of PBBs has been restricted in many regions. Despite this, the legacy of PBBs continues to influence the market, as industries seek safer and more sustainable alternatives. The development of new polymeric bromides that offer similar or improved performance without the associated risks is a key focus for researchers and manufacturers. This ongoing innovation is essential for meeting the evolving demands of various industries while ensuring compliance with environmental and safety regulations. The Global Polymeric Bromide Market is thus characterized by a dynamic interplay between traditional materials like PVB and PBBs and emerging alternatives that promise to deliver enhanced performance and safety.

Flame retardant, PTA synthesis, Plasma Etching, Mercury Removal, Other in the Global Polymeric Bromide Market:

The Global Polymeric Bromide Market finds extensive usage in several critical areas, including flame retardants, PTA synthesis, plasma etching, mercury removal, and other specialized applications. In the realm of flame retardants, polymeric bromides are invaluable due to their ability to significantly reduce the flammability of materials. This makes them essential in the production of electronics, textiles, and construction materials, where fire safety is a major concern. By incorporating polymeric bromides, manufacturers can enhance the safety of their products, thereby meeting stringent regulatory standards and protecting consumers. In PTA synthesis, polymeric bromides play a crucial role as catalysts. Purified Terephthalic Acid (PTA) is a key raw material in the production of polyester, which is widely used in textiles and packaging. The use of polymeric bromides in the synthesis process helps improve efficiency and yield, making it a vital component in the polyester manufacturing industry. Plasma etching, another significant application, involves the use of polymeric bromides in the semiconductor industry. Plasma etching is a process used to create intricate patterns on semiconductor wafers, which are essential for the production of electronic devices. The unique properties of polymeric bromides make them suitable for this high-precision process, contributing to the advancement of semiconductor technology. Mercury removal is yet another critical application of polymeric bromides. Mercury is a hazardous pollutant that poses significant environmental and health risks. Polymeric bromides are used in various processes to capture and remove mercury from industrial emissions, thereby reducing pollution and protecting public health. Beyond these specific applications, polymeric bromides are also used in other specialized areas where their unique properties offer significant advantages. For instance, they are employed in the production of certain types of coatings, adhesives, and sealants, where their chemical stability and resistance to degradation are highly valued. The versatility and effectiveness of polymeric bromides make them indispensable in a wide range of industries, driving the growth and development of the Global Polymeric Bromide Market.

Global Polymeric Bromide Market Outlook:

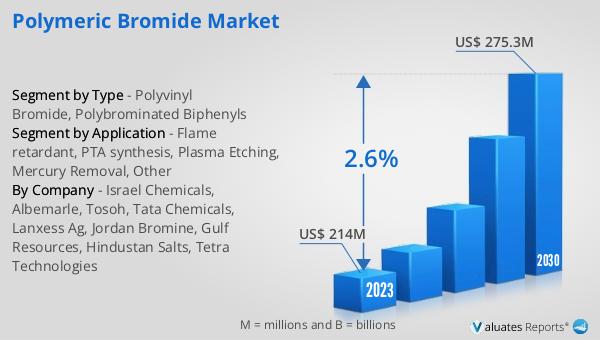

The global Polymeric Bromide market was valued at US$ 214 million in 2023 and is anticipated to reach US$ 275.3 million by 2030, witnessing a CAGR of 2.6% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the polymeric bromide industry over the next several years. The increase in market value reflects the rising demand for polymeric bromides across various applications, driven by their unique properties and effectiveness. The projected compound annual growth rate (CAGR) of 2.6% suggests a consistent expansion, underpinned by ongoing advancements in technology and the development of new applications. As industries continue to prioritize safety, efficiency, and environmental sustainability, the demand for polymeric bromides is expected to grow. This growth is also supported by regulatory frameworks that encourage the use of safer and more efficient materials. The market outlook underscores the importance of innovation and adaptation in meeting the evolving needs of different sectors. Manufacturers and stakeholders in the polymeric bromide market are likely to focus on research and development to create new products that offer enhanced performance and compliance with regulatory standards. Overall, the market outlook for polymeric bromides is positive, with significant opportunities for growth and development in the coming years.

| Report Metric | Details |

| Report Name | Polymeric Bromide Market |

| Accounted market size in 2023 | US$ 214 million |

| Forecasted market size in 2030 | US$ 275.3 million |

| CAGR | 2.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Israel Chemicals, Albemarle, Tosoh, Tata Chemicals, Lanxess Ag, Jordan Bromine, Gulf Resources, Hindustan Salts, Tetra Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |