What is Global High Permeability Magnetic Shielding Sheet Market?

The Global High Permeability Magnetic Shielding Sheet Market refers to the industry focused on the production and distribution of magnetic shielding sheets with high permeability. These sheets are designed to block or redirect magnetic fields, thereby protecting sensitive electronic components and systems from electromagnetic interference (EMI). High permeability materials, such as certain alloys and specialized metals, are used in these sheets to ensure they effectively absorb and neutralize magnetic fields. The market encompasses various applications, including aerospace, automotive, communications, and other sectors where EMI can disrupt functionality and performance. The demand for these shielding sheets is driven by the increasing complexity and sensitivity of modern electronic devices, which require robust protection against magnetic interference to maintain optimal performance and reliability. As technology continues to advance, the need for effective magnetic shielding solutions is expected to grow, making this market a critical component of the broader electronics and materials industries.

0.1-0.3 mm Thickness, Other in the Global High Permeability Magnetic Shielding Sheet Market:

In the Global High Permeability Magnetic Shielding Sheet Market, sheets with a thickness of 0.1-0.3 mm are particularly significant. These thin sheets are highly effective in providing magnetic shielding while maintaining a lightweight and flexible form factor, which is crucial for various applications. The thinness of these sheets allows them to be easily integrated into compact and intricate electronic devices without adding significant bulk or weight. This is especially important in industries like aerospace and automotive, where every gram of weight can impact performance and efficiency. The high permeability of these sheets ensures that they can effectively absorb and redirect magnetic fields, providing robust protection against electromagnetic interference (EMI). This level of protection is essential for maintaining the functionality and reliability of sensitive electronic components. Additionally, the flexibility of these thin sheets allows them to be molded and shaped to fit specific design requirements, making them versatile and adaptable for a wide range of applications. The production of these thin magnetic shielding sheets involves advanced manufacturing techniques to ensure uniform thickness and consistent performance across the entire sheet. This precision is crucial for achieving the desired level of magnetic shielding and ensuring that the sheets meet the stringent quality standards required by various industries. As technology continues to evolve, the demand for thin, high-permeability magnetic shielding sheets is expected to increase, driven by the need for more compact and efficient electronic devices. The ability to provide effective magnetic shielding in a thin and flexible form factor makes these sheets an essential component in the design and development of modern electronics.

Aerospace, Automotive, Communications, Others in the Global High Permeability Magnetic Shielding Sheet Market:

The usage of Global High Permeability Magnetic Shielding Sheets spans across several key industries, including aerospace, automotive, communications, and others. In the aerospace industry, these sheets are critical for protecting avionics and other sensitive electronic systems from electromagnetic interference (EMI). The high permeability of the sheets ensures that they can effectively absorb and neutralize magnetic fields, preventing disruptions to navigation, communication, and control systems. This is particularly important in the aerospace sector, where the reliability and safety of electronic systems are paramount. In the automotive industry, high permeability magnetic shielding sheets are used to protect the increasingly complex electronic systems found in modern vehicles. From advanced driver-assistance systems (ADAS) to infotainment and navigation systems, these sheets help ensure that electronic components function reliably without interference from external magnetic fields. This is crucial for maintaining the performance and safety of vehicles, especially as the automotive industry moves towards more autonomous and connected technologies. In the communications sector, magnetic shielding sheets are used to protect sensitive equipment such as servers, routers, and other networking devices from EMI. This helps maintain the integrity and reliability of data transmission, which is essential for the smooth operation of communication networks. Additionally, these sheets are used in consumer electronics, such as smartphones and laptops, to protect internal components from magnetic interference, ensuring optimal performance and longevity. Beyond these industries, high permeability magnetic shielding sheets are also used in medical devices, industrial equipment, and other applications where EMI can impact functionality and performance. The versatility and effectiveness of these sheets make them a valuable solution for a wide range of applications, highlighting their importance in the modern technological landscape.

Global High Permeability Magnetic Shielding Sheet Market Outlook:

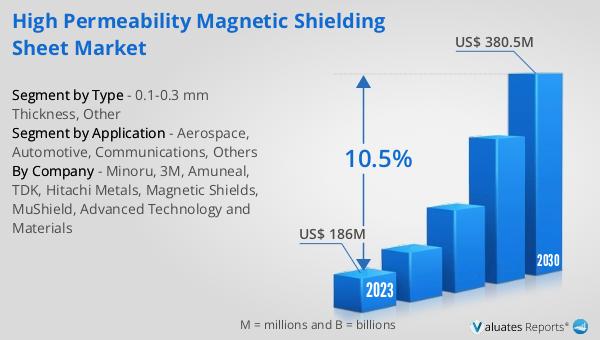

The global High Permeability Magnetic Shielding Sheet market was valued at US$ 186 million in 2023 and is anticipated to reach US$ 380.5 million by 2030, witnessing a CAGR of 10.5% during the forecast period 2024-2030. This significant growth reflects the increasing demand for effective magnetic shielding solutions across various industries. As electronic devices become more complex and sensitive, the need for robust protection against electromagnetic interference (EMI) continues to rise. High permeability magnetic shielding sheets offer an efficient and reliable solution to this challenge, making them an essential component in the design and development of modern electronics. The market's growth is driven by advancements in technology and the expanding applications of these shielding sheets in sectors such as aerospace, automotive, communications, and others. The ability to provide effective magnetic shielding in a thin and flexible form factor makes these sheets highly desirable for a wide range of applications. As a result, the global market for high permeability magnetic shielding sheets is expected to continue its upward trajectory, driven by the ongoing demand for advanced electronic devices and systems that require robust EMI protection.

| Report Metric | Details |

| Report Name | High Permeability Magnetic Shielding Sheet Market |

| Accounted market size in 2023 | US$ 186 million |

| Forecasted market size in 2030 | US$ 380.5 million |

| CAGR | 10.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Minoru, 3M, Amuneal, TDK, Hitachi Metals, Magnetic Shields, MuShield, Advanced Technology and Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |