What is Global SiC Chips Design Market?

The Global SiC (Silicon Carbide) Chips Design Market is a rapidly evolving sector within the semiconductor industry. SiC chips are known for their superior performance in high-temperature, high-voltage, and high-frequency applications compared to traditional silicon-based chips. These chips are increasingly being adopted across various industries due to their efficiency and reliability. The market for SiC chips is driven by the growing demand for energy-efficient electronic devices, advancements in electric vehicles (EVs), and the need for robust power management systems. As industries continue to seek ways to enhance performance while reducing energy consumption, SiC chips offer a promising solution. The market encompasses a wide range of applications, from automotive to renewable energy sectors, making it a critical area of focus for technological advancements and innovation.

in the Global SiC Chips Design Market:

The Global SiC Chips Design Market caters to a diverse range of customers, each with specific requirements and applications. In the automotive sector, SiC chips are used in electric vehicles (EVs) and hybrid electric vehicles (HEVs) to improve efficiency and performance. These chips help in reducing energy losses and enhancing the overall driving range of EVs. In the realm of EV charging, SiC chips are crucial for developing fast-charging stations that can handle high power levels without significant energy loss. This is essential for reducing charging times and making EVs more convenient for users. Uninterruptible Power Supplies (UPS) also benefit from SiC technology, as these chips provide reliable power management and ensure continuous operation during power outages. Data centers and servers, which require efficient power management to handle large volumes of data, utilize SiC chips to enhance performance and reduce energy consumption. In the photovoltaic (PV) industry, SiC chips are used in solar inverters to convert solar energy into usable electricity more efficiently. Energy storage systems, which are critical for managing renewable energy sources, also rely on SiC technology for better performance and reliability. Wind power generation, another key area, uses SiC chips in power converters to improve efficiency and reduce maintenance costs. Other applications include industrial machinery, aerospace, and defense, where the high-temperature and high-voltage capabilities of SiC chips are particularly beneficial. Each of these sectors leverages the unique properties of SiC chips to enhance performance, reduce energy consumption, and improve overall system reliability.

Automotive & EV/HEV, EV Charging, UPS, Data Center & Server, PV, Energy Storage, Wind Power, Others in the Global SiC Chips Design Market:

The usage of SiC chips in the automotive and EV/HEV sectors is particularly noteworthy. These chips are integral to the development of more efficient and reliable electric vehicles. By reducing energy losses and improving thermal management, SiC chips help extend the driving range of EVs and enhance their overall performance. In EV charging, SiC technology enables the creation of fast-charging stations that can handle higher power levels, significantly reducing charging times and making EVs more practical for everyday use. Uninterruptible Power Supplies (UPS) benefit from SiC chips by providing more reliable power management solutions, ensuring continuous operation during power outages and reducing downtime. Data centers and servers, which require efficient power management to handle large volumes of data, utilize SiC chips to enhance performance and reduce energy consumption. In the photovoltaic (PV) industry, SiC chips are used in solar inverters to convert solar energy into usable electricity more efficiently, thereby increasing the overall efficiency of solar power systems. Energy storage systems, which are critical for managing renewable energy sources, also rely on SiC technology for better performance and reliability. Wind power generation, another key area, uses SiC chips in power converters to improve efficiency and reduce maintenance costs. Other applications include industrial machinery, aerospace, and defense, where the high-temperature and high-voltage capabilities of SiC chips are particularly beneficial. Each of these sectors leverages the unique properties of SiC chips to enhance performance, reduce energy consumption, and improve overall system reliability.

Global SiC Chips Design Market Outlook:

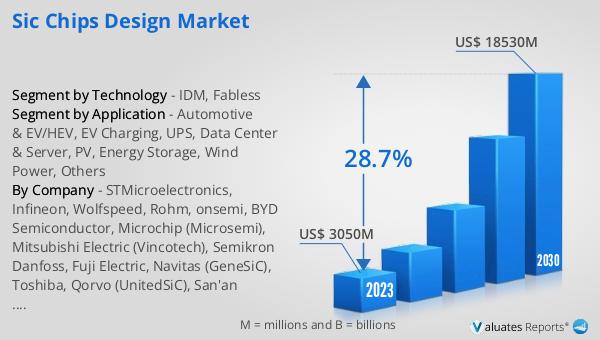

The global SiC Chips Design market was valued at US$ 3050 million in 2023 and is anticipated to reach US$ 18530 million by 2030, witnessing a CAGR of 28.7% during the forecast period 2024-2030. This significant growth is driven by the increasing demand for energy-efficient electronic devices and advancements in electric vehicles. The market's expansion is also fueled by the need for robust power management systems across various industries. As more sectors adopt SiC technology to enhance performance and reduce energy consumption, the market is expected to continue its upward trajectory. The versatility and efficiency of SiC chips make them a critical component in the development of next-generation electronic devices and systems.

| Report Metric | Details |

| Report Name | SiC Chips Design Market |

| Accounted market size in 2023 | US$ 3050 million |

| Forecasted market size in 2030 | US$ 18530 million |

| CAGR | 28.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Technology |

|

| Segment by Application |

|

| By Region |

|

| By Company | STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, Microchip (Microsemi), Mitsubishi Electric (Vincotech), Semikron Danfoss, Fuji Electric, Navitas (GeneSiC), Toshiba, Qorvo (UnitedSiC), San'an Optoelectronics, Littelfuse (IXYS), CETC 55, WeEn Semiconductors, BASiC Semiconductor, SemiQ, Diodes Incorporated, SanRex, Alpha & Omega Semiconductor, Bosch, GE Aerospace, KEC Corporation, PANJIT Group, Nexperia, Vishay Intertechnology, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, StarPower, Yangzhou Yangjie Electronic Technology, Guangdong AccoPower Semiconductor, Changzhou Galaxy Century Microelectronics, Hangzhou Silan Microelectronics, Cissoid, SK powertech, InventChip Technology, Hebei Sinopack Electronic Technology, Oriental Semiconductor, Jilin Sino-Microelectronics, PN Junction Semiconductor (Hangzhou) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |