What is Global Semiconductor Isotropic Graphite Market?

The Global Semiconductor Isotropic Graphite Market is a specialized segment within the broader graphite market, focusing on isotropic graphite used in semiconductor manufacturing. Isotropic graphite is a type of synthetic graphite known for its uniform properties in all directions, making it ideal for high-precision applications. This material is crucial in the semiconductor industry due to its excellent thermal and electrical conductivity, high purity, and resistance to thermal shock. These properties make isotropic graphite indispensable in processes like semiconductor crystal growth, epitaxy, ion implantation, and plasma etching. The market for this material is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and industrial sectors. As technology advances and the need for more efficient and reliable semiconductors grows, the demand for high-quality isotropic graphite is expected to rise. This market is characterized by a few key players who dominate the production and supply of isotropic graphite, ensuring that the material meets the stringent quality standards required by the semiconductor industry.

Purity ≥ 99.9%, Purity ≥ 99.99%, Purity ≥ 99.999%, Others in the Global Semiconductor Isotropic Graphite Market:

In the Global Semiconductor Isotropic Graphite Market, purity levels are a critical factor that determines the material's suitability for various applications. Purity levels are typically categorized as Purity ≥ 99.9%, Purity ≥ 99.99%, Purity ≥ 99.999%, and Others. Each level of purity has its specific applications and advantages. Purity ≥ 99.9% isotropic graphite is commonly used in applications where high thermal and electrical conductivity are required, but the presence of minor impurities is acceptable. This level of purity is often sufficient for general semiconductor manufacturing processes. Purity ≥ 99.99% isotropic graphite is used in more demanding applications where even minor impurities can affect the performance of the semiconductor devices. This level of purity ensures that the material has fewer contaminants, making it suitable for high-precision applications like semiconductor crystal growth and epitaxy. Purity ≥ 99.999% isotropic graphite is the highest purity level available and is used in the most critical applications where any impurities can lead to significant performance issues. This ultra-high purity graphite is essential for processes like ion implantation and plasma etching, where the presence of contaminants can severely impact the quality and reliability of the semiconductor devices. The "Others" category includes isotropic graphite with varying purity levels that do not fall into the standard categories. These materials are used in specialized applications where specific properties are required, and the standard purity levels may not be sufficient. The choice of purity level depends on the specific requirements of the semiconductor manufacturing process, with higher purity levels generally offering better performance and reliability. The production of high-purity isotropic graphite involves advanced manufacturing techniques and stringent quality control measures to ensure that the material meets the required standards. This includes processes like high-temperature purification, chemical vapor deposition, and meticulous inspection and testing. The demand for high-purity isotropic graphite is driven by the increasing complexity and miniaturization of semiconductor devices, which require materials with exceptional properties to ensure their performance and reliability. As the semiconductor industry continues to evolve, the need for high-purity isotropic graphite is expected to grow, making it a critical component in the production of advanced semiconductor devices.

Semiconductor Crystal Growth, Semiconductor Epitaxy, Ion Implantation, Plasma Etching, Others in the Global Semiconductor Isotropic Graphite Market:

The Global Semiconductor Isotropic Graphite Market finds extensive usage in various critical areas of semiconductor manufacturing, including Semiconductor Crystal Growth, Semiconductor Epitaxy, Ion Implantation, Plasma Etching, and Others. In Semiconductor Crystal Growth, isotropic graphite is used to create the crucibles and molds that hold the raw materials during the crystal growth process. Its high thermal conductivity and resistance to thermal shock ensure that the crystals grow uniformly, which is essential for producing high-quality semiconductor wafers. In Semiconductor Epitaxy, isotropic graphite is used as a substrate material due to its excellent thermal and electrical properties. It provides a stable and uniform surface for the deposition of thin semiconductor layers, which is crucial for creating high-performance semiconductor devices. In Ion Implantation, isotropic graphite is used in the construction of ion sources and beamline components. Its high purity and resistance to ion bombardment make it ideal for this application, ensuring that the implanted ions are accurately delivered to the semiconductor wafers without contamination. In Plasma Etching, isotropic graphite is used to create the electrodes and other components that generate and control the plasma. Its high thermal and electrical conductivity, combined with its resistance to chemical attack, make it an ideal material for this application. The "Others" category includes various specialized applications where isotropic graphite's unique properties are required. This can include uses in chemical vapor deposition, physical vapor deposition, and other advanced semiconductor manufacturing processes. The versatility and reliability of isotropic graphite make it an indispensable material in the semiconductor industry, ensuring that the complex and precise processes involved in semiconductor manufacturing can be carried out effectively and efficiently. As the demand for advanced semiconductor devices continues to grow, the usage of isotropic graphite in these critical areas is expected to increase, further highlighting its importance in the semiconductor manufacturing process.

Global Semiconductor Isotropic Graphite Market Outlook:

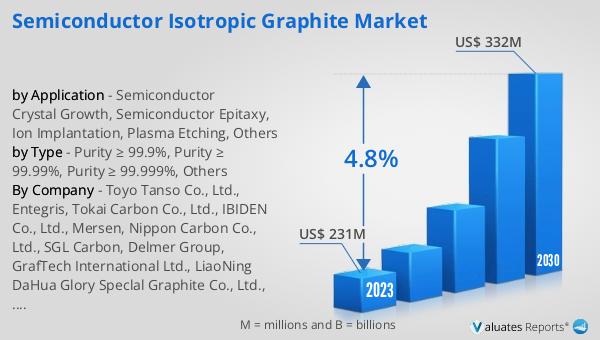

The global Semiconductor Isotropic Graphite market was valued at US$ 231 million in 2023 and is anticipated to reach US$ 332 million by 2030, witnessing a CAGR of 4.8% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for high-quality isotropic graphite in the semiconductor industry. The growth is attributed to the rising need for advanced semiconductor devices in various applications, including consumer electronics, automotive, and industrial sectors. The market's expansion is also supported by technological advancements and the continuous miniaturization of semiconductor components, which require materials with exceptional properties to ensure their performance and reliability. The projected growth rate of 4.8% CAGR reflects the market's resilience and the ongoing investments in semiconductor manufacturing infrastructure. As the industry evolves, the demand for high-purity isotropic graphite is expected to rise, making it a critical component in the production of advanced semiconductor devices. The market outlook underscores the importance of isotropic graphite in meeting the stringent quality standards required by the semiconductor industry, ensuring the production of reliable and efficient semiconductor devices.

| Report Metric | Details |

| Report Name | Semiconductor Isotropic Graphite Market |

| Accounted market size in 2023 | US$ 231 million |

| Forecasted market size in 2030 | US$ 332 million |

| CAGR | 4.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Toyo Tanso Co., Ltd., Entegris, Tokai Carbon Co., Ltd., IBIDEN Co., Ltd., Mersen, Nippon Carbon Co., Ltd., SGL Carbon, Delmer Group, GrafTech International Ltd., LiaoNing DaHua Glory Speclal Graphite Co., Ltd., WuXing New Material Technology Co., Ltd., Chengdu Carbon Co.,Ltd., Sichuan Guanghan Shida Carbon Co., Ltd., Graphite India Limited |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |