What is Global Edge Cloud Service Market?

The Global Edge Cloud Service Market refers to a rapidly evolving sector within the broader cloud computing industry. Edge cloud services are designed to bring computing power closer to the data source or end-user, reducing latency and improving performance. This is particularly important for applications that require real-time processing, such as autonomous vehicles, smart cities, and IoT devices. By leveraging edge cloud services, businesses can enhance their operational efficiency, reduce costs, and deliver a better user experience. The market encompasses a wide range of services, including data storage, processing, and analytics, all delivered through a distributed network of edge nodes. These services are crucial for industries that rely on fast data processing and low-latency communication, making the Global Edge Cloud Service Market a key player in the future of technology.

Cloud-Based, On-Premises in the Global Edge Cloud Service Market:

Cloud-based and on-premises solutions are two primary deployment models within the Global Edge Cloud Service Market. Cloud-based edge services are hosted on remote servers and accessed via the internet, offering scalability, flexibility, and cost-effectiveness. These services are ideal for businesses that need to quickly scale their operations without investing heavily in physical infrastructure. Cloud-based solutions also provide the advantage of easy updates and maintenance, as the service provider handles these tasks. On the other hand, on-premises edge solutions are deployed locally within an organization's own data centers or facilities. This model offers greater control over data and security, making it suitable for industries with stringent regulatory requirements or sensitive data. On-premises solutions can also provide lower latency compared to cloud-based services, as data does not need to travel over the internet. However, they require significant upfront investment in hardware and ongoing maintenance costs. Both deployment models have their own set of advantages and challenges, and the choice between them often depends on the specific needs and constraints of the business. For instance, a large enterprise with extensive IT resources might opt for an on-premises solution to maintain control over its data, while a small or medium enterprise might prefer the flexibility and lower costs of a cloud-based service. The Global Edge Cloud Service Market continues to evolve, with many providers offering hybrid solutions that combine the best of both worlds. These hybrid models allow businesses to leverage the scalability of cloud-based services while maintaining control over critical data through on-premises deployments. As the demand for real-time data processing and low-latency communication grows, the market for both cloud-based and on-premises edge solutions is expected to expand, offering a wide range of options for businesses of all sizes.

Large Enterprises, Medium Enterprises, Small Enterprises in the Global Edge Cloud Service Market:

The usage of Global Edge Cloud Service Market varies significantly across large enterprises, medium enterprises, and small enterprises, each with its own set of requirements and challenges. Large enterprises often have complex IT infrastructures and require robust, scalable solutions to manage vast amounts of data. For these organizations, edge cloud services offer the ability to process data closer to the source, reducing latency and improving performance. This is particularly beneficial for industries such as finance, healthcare, and manufacturing, where real-time data processing is critical. Large enterprises can also leverage edge cloud services to enhance their cybersecurity measures, as data can be processed and analyzed locally before being sent to the cloud. Medium enterprises, on the other hand, may not have the same level of IT resources as large enterprises but still require efficient data processing and storage solutions. Edge cloud services provide these businesses with the flexibility to scale their operations without significant upfront investment in infrastructure. This is particularly useful for industries such as retail, logistics, and telecommunications, where the ability to quickly adapt to changing market conditions is crucial. Medium enterprises can also benefit from the improved performance and reduced latency offered by edge cloud services, enabling them to deliver better customer experiences. Small enterprises often face the challenge of limited IT budgets and resources, making it difficult to invest in expensive infrastructure. For these businesses, cloud-based edge services offer an affordable and scalable solution to their data processing needs. By leveraging edge cloud services, small enterprises can access advanced technologies and capabilities that were previously out of reach, such as real-time analytics and machine learning. This can help them compete more effectively with larger competitors and drive innovation within their industries. Additionally, edge cloud services can provide small enterprises with enhanced security and compliance features, ensuring that their data is protected and meets regulatory requirements. Overall, the Global Edge Cloud Service Market offers a wide range of solutions tailored to the needs of businesses of all sizes, enabling them to harness the power of edge computing and drive growth and innovation.

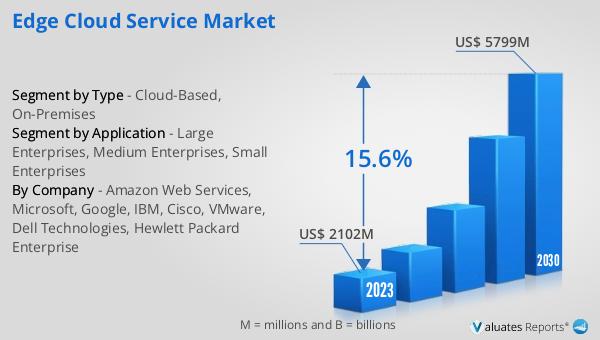

Global Edge Cloud Service Market Outlook:

The global Edge Cloud Service market was valued at US$ 2102 million in 2023 and is anticipated to reach US$ 5799 million by 2030, witnessing a CAGR of 15.6% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for real-time data processing and low-latency communication across various industries. As businesses continue to adopt digital transformation strategies, the need for efficient and scalable edge cloud services is expected to rise. The market's expansion is driven by advancements in technology, such as the proliferation of IoT devices, the development of 5G networks, and the growing importance of data analytics. These factors are contributing to the widespread adoption of edge cloud services, enabling businesses to enhance their operational efficiency and deliver better user experiences. The projected growth of the Global Edge Cloud Service Market underscores the critical role that edge computing will play in the future of technology, providing businesses with the tools they need to stay competitive in an increasingly digital world.

| Report Metric | Details |

| Report Name | Edge Cloud Service Market |

| Accounted market size in 2023 | US$ 2102 million |

| Forecasted market size in 2030 | US$ 5799 million |

| CAGR | 15.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Amazon Web Services, Microsoft, Google, IBM, Cisco, VMware, Dell Technologies, Hewlett Packard Enterprise |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |