What is Global Large Size Panel Display Driver Chip Market?

The Global Large Size Panel Display Driver Chip Market refers to the industry that produces and sells driver chips specifically designed for large-sized display panels. These driver chips are essential components in various electronic devices, as they control the display's performance by managing the electrical signals that create images on the screen. The market encompasses a wide range of applications, including televisions, computer monitors, automotive displays, and other large-format screens. The demand for these chips is driven by the increasing popularity of high-definition and ultra-high-definition displays, which require more advanced driver technology to deliver superior image quality. Additionally, the rise of smart devices and the growing trend of integrating advanced display technologies in various sectors contribute to the market's expansion. As a result, manufacturers are continuously innovating to develop more efficient and powerful driver chips to meet the evolving needs of the market.

LCD Display Driver Chip, OLED Display Driver Chip in the Global Large Size Panel Display Driver Chip Market:

LCD Display Driver Chips and OLED Display Driver Chips are two primary types of driver chips used in the Global Large Size Panel Display Driver Chip Market. LCD (Liquid Crystal Display) driver chips are designed to control the pixels in an LCD screen by managing the voltage applied to the liquid crystals. These chips are crucial for ensuring accurate color reproduction, brightness, and contrast in LCD panels. They are widely used in televisions, computer monitors, and other large-format displays due to their cost-effectiveness and reliability. On the other hand, OLED (Organic Light Emitting Diode) driver chips are used in OLED panels, which offer superior image quality with deeper blacks, higher contrast ratios, and faster response times compared to LCDs. OLED driver chips manage the current flowing through the organic materials in the display, enabling each pixel to emit light independently. This results in more vibrant colors and better overall picture quality. OLED technology is increasingly popular in high-end televisions, smartphones, and other premium devices. Both LCD and OLED driver chips play a critical role in the performance of large-sized displays, and their development is driven by the demand for better image quality and more energy-efficient solutions. As the market for large-sized panels continues to grow, the competition between LCD and OLED technologies intensifies, leading to continuous advancements in driver chip design and functionality.

TV, Monitor, Car Display, Others in the Global Large Size Panel Display Driver Chip Market:

The usage of Global Large Size Panel Display Driver Chips spans various applications, including TVs, monitors, car displays, and other devices. In the television sector, these driver chips are essential for delivering high-definition and ultra-high-definition content, ensuring that viewers experience sharp, vibrant images with accurate colors and contrast. The demand for larger and more advanced TV screens has led to the development of more sophisticated driver chips that can handle the increased pixel density and provide smoother performance. In computer monitors, display driver chips are crucial for achieving high refresh rates and low response times, which are particularly important for gaming and professional applications where image quality and speed are paramount. The growing trend of remote work and online learning has also boosted the demand for high-quality monitors, further driving the need for advanced driver chips. In the automotive industry, display driver chips are used in car displays, including infotainment systems, digital dashboards, and heads-up displays. These chips ensure that the information displayed is clear and easily readable, enhancing the overall driving experience and safety. As cars become more connected and feature-rich, the demand for high-quality displays and, consequently, advanced driver chips, continues to rise. Other applications of large-size panel display driver chips include digital signage, medical displays, and industrial monitors, where high resolution and reliability are critical. In all these areas, the continuous improvement of driver chip technology is essential to meet the growing expectations for better performance, energy efficiency, and overall user experience.

Global Large Size Panel Display Driver Chip Market Outlook:

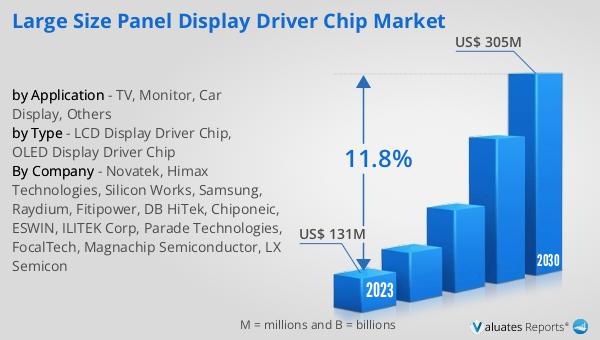

The global Large Size Panel Display Driver Chip market was valued at US$ 131 million in 2023 and is anticipated to reach US$ 305 million by 2030, witnessing a CAGR of 11.8% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-quality large-sized displays across various sectors, including consumer electronics, automotive, and industrial applications. The market's expansion is driven by technological advancements in display technologies, such as the development of more efficient and powerful driver chips that can support higher resolutions and better image quality. Additionally, the growing popularity of smart devices and the integration of advanced display features in various products contribute to the rising demand for large-size panel display driver chips. As manufacturers continue to innovate and improve their products, the market is expected to see sustained growth, offering numerous opportunities for companies operating in this space.

| Report Metric | Details |

| Report Name | Large Size Panel Display Driver Chip Market |

| Accounted market size in 2023 | US$ 131 million |

| Forecasted market size in 2030 | US$ 305 million |

| CAGR | 11.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Novatek, Himax Technologies, Silicon Works, Samsung, Raydium, Fitipower, DB HiTek, Chiponeic, ESWIN, ILITEK Corp, Parade Technologies, FocalTech, Magnachip Semiconductor, LX Semicon |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |