What is Global Continuous Vessel Unloader Market?

The Global Continuous Vessel Unloader Market refers to the industry focused on the development, production, and distribution of machinery designed to unload bulk materials from vessels continuously. These machines are essential in various industries such as energy, mining, and metallurgy, where large quantities of materials like coal, ores, and grains need to be transferred efficiently from ships to storage facilities or processing plants. Continuous vessel unloaders are preferred over traditional unloading methods because they offer higher efficiency, reduced labor costs, and minimized material handling time. The market encompasses different types of unloaders, including spiral unloaders, grab unloaders, and belt unloaders, each designed to handle specific types of materials and operational requirements. The demand for these machines is driven by the increasing global trade of bulk commodities and the need for more efficient and cost-effective unloading solutions. As industries continue to expand and modernize, the Global Continuous Vessel Unloader Market is expected to grow, offering advanced technologies and improved performance to meet the evolving needs of various sectors.

Spiral Unloader, Grab Unloader, Belt Unloader, Other in the Global Continuous Vessel Unloader Market:

Spiral unloaders, grab unloaders, belt unloaders, and other types of continuous vessel unloaders each play a unique role in the Global Continuous Vessel Unloader Market. Spiral unloaders are designed to handle free-flowing materials such as grains, fertilizers, and certain types of ores. They operate using a rotating spiral mechanism that lifts and transports the material from the vessel to the desired location. This type of unloader is highly efficient for materials that do not require complex handling and can be easily moved through the spiral system. Grab unloaders, on the other hand, are more versatile and can handle a wider range of materials, including those that are sticky, lumpy, or irregularly shaped. They use a clamshell bucket or grab mechanism to scoop up the material and transfer it to a conveyor or storage area. Grab unloaders are particularly useful in ports and terminals where different types of bulk materials are frequently handled. Belt unloaders are designed for continuous and high-capacity unloading of materials such as coal, iron ore, and other heavy bulk commodities. They use a conveyor belt system to transport the material from the vessel to the storage or processing area. Belt unloaders are known for their high efficiency, reliability, and ability to handle large volumes of material with minimal spillage. Other types of continuous vessel unloaders include pneumatic unloaders, which use air pressure to move materials through pipelines, and screw unloaders, which use a rotating screw mechanism to transport materials. Each type of unloader has its own advantages and is selected based on the specific requirements of the operation, such as the type of material being handled, the unloading capacity needed, and the operational environment. The continuous development and innovation in unloader technology are driving the growth of the Global Continuous Vessel Unloader Market, providing industries with more efficient and cost-effective solutions for their bulk material handling needs.

Energy, Mining, Metallurgy, Other in the Global Continuous Vessel Unloader Market:

The Global Continuous Vessel Unloader Market finds extensive usage in various sectors, including energy, mining, metallurgy, and others. In the energy sector, continuous vessel unloaders are crucial for handling bulk materials such as coal, biomass, and other fuels used in power generation. These unloaders ensure a steady and efficient supply of fuel to power plants, reducing downtime and improving overall operational efficiency. In the mining industry, continuous vessel unloaders are used to handle ores, minerals, and other raw materials extracted from mines. They facilitate the efficient transfer of these materials from ships to storage facilities or processing plants, ensuring a smooth and continuous supply chain. In the metallurgy sector, continuous vessel unloaders are used to handle raw materials such as iron ore, bauxite, and other metals that are essential for the production of steel and other metal products. These unloaders help in maintaining a consistent supply of raw materials to smelting and refining plants, improving productivity and reducing operational costs. Other industries that benefit from continuous vessel unloaders include agriculture, where they are used to handle grains, fertilizers, and other bulk agricultural products, and the construction industry, where they are used to handle materials such as cement, sand, and gravel. The versatility and efficiency of continuous vessel unloaders make them an essential component in various industrial operations, ensuring the smooth and continuous flow of materials and improving overall productivity. The growing demand for bulk materials and the need for efficient handling solutions are driving the growth of the Global Continuous Vessel Unloader Market, providing industries with advanced technologies and improved performance to meet their evolving needs.

Global Continuous Vessel Unloader Market Outlook:

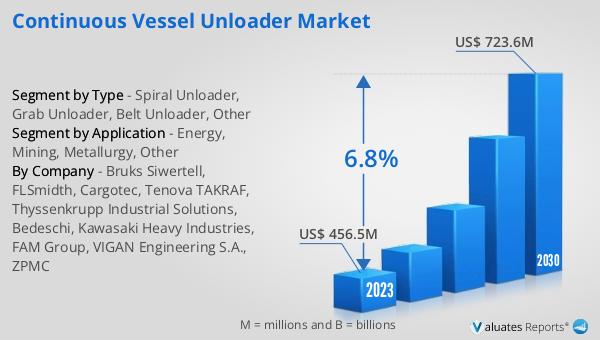

The global Continuous Vessel Unloader market was valued at US$ 456.5 million in 2023 and is anticipated to reach US$ 723.6 million by 2030, witnessing a CAGR of 6.8% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the continuous vessel unloader market, driven by the increasing demand for efficient and cost-effective bulk material handling solutions across various industries. The continuous vessel unloader market is expected to experience steady growth over the forecast period, with advancements in technology and the development of new and innovative unloading solutions contributing to this growth. The increasing global trade of bulk commodities, coupled with the need for more efficient and reliable unloading systems, is expected to drive the demand for continuous vessel unloaders. Additionally, the growing focus on sustainability and environmental protection is likely to further boost the adoption of continuous vessel unloaders, as these systems help in reducing material spillage and minimizing environmental impact. The continuous vessel unloader market is poised for significant growth, offering numerous opportunities for manufacturers and suppliers to capitalize on the increasing demand for advanced and efficient bulk material handling solutions.

| Report Metric | Details |

| Report Name | Continuous Vessel Unloader Market |

| Accounted market size in 2023 | US$ 456.5 million |

| Forecasted market size in 2030 | US$ 723.6 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bruks Siwertell, FLSmidth, Cargotec, Tenova TAKRAF, Thyssenkrupp Industrial Solutions, Bedeschi, Kawasaki Heavy Industries, FAM Group, VIGAN Engineering S.A., ZPMC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |