What is Global In-Cabin Monitoring Image Sensor Market?

The Global In-Cabin Monitoring Image Sensor Market refers to the industry focused on developing and deploying image sensors within vehicle cabins to enhance safety, comfort, and user experience. These sensors are designed to monitor various in-cabin activities, such as driver behavior, passenger status, and environmental conditions. By capturing and analyzing images, these sensors can detect signs of driver fatigue, distraction, or even medical emergencies, thereby enabling timely interventions. Additionally, they can monitor passenger occupancy and adjust climate control or infotainment settings accordingly. The market for these sensors is growing rapidly due to increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies. As automotive manufacturers strive to enhance vehicle safety and user experience, the adoption of in-cabin monitoring image sensors is expected to rise significantly. These sensors are becoming a critical component in modern vehicles, contributing to the overall trend towards smarter and safer transportation solutions.

IR Image Sensor, RGB-IR Image Sensor, Others in the Global In-Cabin Monitoring Image Sensor Market:

IR Image Sensors, RGB-IR Image Sensors, and other types of sensors play a crucial role in the Global In-Cabin Monitoring Image Sensor Market. IR (Infrared) Image Sensors are designed to capture images in low-light or no-light conditions, making them ideal for monitoring driver behavior and passenger activities during nighttime or in poorly lit environments. These sensors can detect subtle changes in temperature and movement, providing valuable data for systems that aim to prevent driver fatigue or distraction. RGB-IR Image Sensors, on the other hand, combine the capabilities of traditional RGB (Red, Green, Blue) sensors with infrared sensing. This combination allows for more accurate and detailed image capture, even in challenging lighting conditions. RGB-IR sensors can differentiate between various objects and surfaces within the cabin, enhancing the system's ability to monitor and respond to different scenarios. Other types of sensors, such as thermal sensors and ultrasonic sensors, also contribute to the in-cabin monitoring ecosystem. Thermal sensors detect heat signatures, which can be used to monitor the presence and condition of passengers, while ultrasonic sensors use sound waves to detect movement and occupancy. Together, these sensors create a comprehensive monitoring system that enhances vehicle safety and user experience. The integration of these sensors into vehicles is driven by the need for advanced driver-assistance systems (ADAS) and autonomous driving technologies. As automotive manufacturers continue to innovate and improve vehicle safety features, the demand for in-cabin monitoring image sensors is expected to grow. These sensors not only enhance safety but also contribute to a more personalized and comfortable driving experience by adjusting settings based on real-time data. For instance, they can automatically adjust the air conditioning or infotainment system based on the number of passengers and their preferences. The combination of IR, RGB-IR, and other sensors ensures that the monitoring system is robust and reliable, capable of functioning effectively in various conditions and scenarios. This comprehensive approach to in-cabin monitoring is essential for the development of smarter and safer vehicles, aligning with the broader trends in the automotive industry towards automation and enhanced user experience.

Passenger Car, Commercial Car in the Global In-Cabin Monitoring Image Sensor Market:

The usage of Global In-Cabin Monitoring Image Sensors in passenger cars and commercial vehicles is becoming increasingly prevalent due to the growing emphasis on safety and user experience. In passenger cars, these sensors are primarily used to monitor driver behavior and passenger status. For instance, they can detect if the driver is showing signs of fatigue or distraction and alert them to take a break or refocus on the road. This is particularly important for long-distance driving, where the risk of accidents due to driver fatigue is higher. Additionally, in-cabin monitoring sensors can detect the presence of passengers and adjust the vehicle's climate control and infotainment settings accordingly, ensuring a comfortable and personalized experience for everyone in the car. In commercial vehicles, the application of in-cabin monitoring image sensors is equally significant. These sensors are used to monitor the behavior of professional drivers, such as those operating trucks, buses, or delivery vans. By detecting signs of fatigue, distraction, or other risky behaviors, these sensors can help prevent accidents and improve overall road safety. This is particularly important in the commercial sector, where driver safety is not only a matter of personal well-being but also has significant economic implications. For instance, accidents involving commercial vehicles can lead to costly damages, legal liabilities, and disruptions in supply chains. In-cabin monitoring sensors can also be used to ensure compliance with regulations and company policies, such as mandatory rest breaks and safe driving practices. Furthermore, these sensors can enhance the overall efficiency of commercial operations by providing valuable data on driver behavior and vehicle usage. This data can be used to optimize routes, reduce fuel consumption, and improve maintenance schedules, ultimately leading to cost savings and increased productivity. The integration of in-cabin monitoring image sensors in both passenger and commercial vehicles is a testament to the growing importance of advanced safety and user experience features in the automotive industry. As technology continues to evolve, the capabilities of these sensors are expected to expand, offering even more sophisticated monitoring and intervention solutions. This will further enhance the safety, comfort, and efficiency of both passenger and commercial vehicles, contributing to the broader goals of smarter and safer transportation systems.

Global In-Cabin Monitoring Image Sensor Market Outlook:

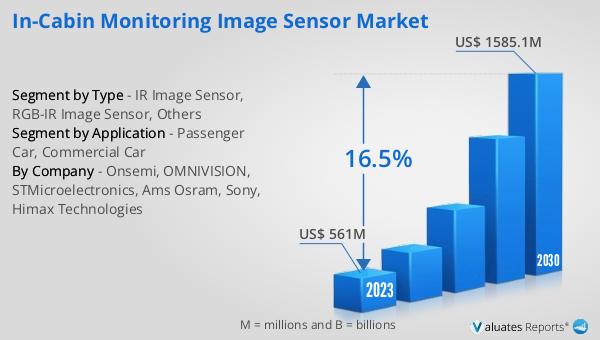

The global In-Cabin Monitoring Image Sensor market was valued at US$ 561 million in 2023 and is anticipated to reach US$ 1585.1 million by 2030, witnessing a CAGR of 16.5% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies, which rely heavily on in-cabin monitoring to enhance safety and user experience. The market's expansion is driven by the automotive industry's continuous efforts to innovate and improve vehicle safety features. As manufacturers integrate more sophisticated monitoring systems into their vehicles, the adoption of in-cabin image sensors is expected to rise. These sensors play a crucial role in detecting driver fatigue, distraction, and other risky behaviors, enabling timely interventions that can prevent accidents and save lives. Additionally, they contribute to a more personalized and comfortable driving experience by adjusting settings based on real-time data. The projected growth of the in-cabin monitoring image sensor market underscores the broader trends in the automotive industry towards smarter and safer transportation solutions. As technology continues to advance, the capabilities of these sensors are expected to expand, offering even more sophisticated monitoring and intervention solutions. This will further enhance the safety, comfort, and efficiency of both passenger and commercial vehicles, contributing to the broader goals of smarter and safer transportation systems.

| Report Metric | Details |

| Report Name | In-Cabin Monitoring Image Sensor Market |

| Accounted market size in 2023 | US$ 561 million |

| Forecasted market size in 2030 | US$ 1585.1 million |

| CAGR | 16.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Onsemi, OMNIVISION, STMicroelectronics, Ams Osram, Sony, Himax Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |