What is Global Eccentricity Measurement Tools Market?

The Global Eccentricity Measurement Tools Market is a specialized segment within the broader field of precision measurement tools. These tools are designed to measure the eccentricity, or the degree to which an object deviates from being perfectly circular or cylindrical. Eccentricity measurement tools are crucial in various industries where precision is paramount, such as automotive, aerospace, and manufacturing. These tools help ensure that components meet stringent quality standards, thereby enhancing the performance and safety of the final products. The market for these tools is driven by the increasing demand for high-precision components and the growing adoption of automation in manufacturing processes. Technological advancements have also led to the development of more sophisticated and accurate measurement tools, further fueling market growth. The global market is characterized by a mix of established players and new entrants, all vying to offer innovative solutions to meet the evolving needs of their customers.

Portable, Desktop in the Global Eccentricity Measurement Tools Market:

Portable and desktop-based eccentricity measurement tools are two primary categories within the Global Eccentricity Measurement Tools Market. Portable eccentricity measurement tools are designed for on-the-go use, making them ideal for fieldwork and on-site inspections. These tools are typically lightweight, easy to handle, and come with user-friendly interfaces. They are often battery-operated and can be used in various environmental conditions, making them highly versatile. Portable tools are commonly used in industries such as construction, automotive, and aerospace, where quick and accurate measurements are essential. On the other hand, desktop-based eccentricity measurement tools are designed for more controlled environments, such as laboratories and manufacturing facilities. These tools are generally more robust and offer higher precision compared to their portable counterparts. They are often integrated with advanced software that allows for detailed analysis and reporting. Desktop-based tools are ideal for applications that require high accuracy and repeatability, such as quality control and research and development. Both types of tools have their unique advantages and are chosen based on the specific needs of the application. For instance, in the automotive industry, portable tools might be used for on-site inspections of vehicle components, while desktop-based tools could be used for detailed analysis in a laboratory setting. Similarly, in the aerospace industry, portable tools might be used for field inspections of aircraft parts, whereas desktop-based tools could be used for precision measurements during the manufacturing process. The choice between portable and desktop-based tools often depends on factors such as the required level of precision, the working environment, and the specific application. Both types of tools are essential for ensuring the quality and performance of components in various industries.

Industrial, Laboratories in the Global Eccentricity Measurement Tools Market:

The usage of Global Eccentricity Measurement Tools Market in industrial and laboratory settings is extensive and varied. In industrial settings, these tools are primarily used for quality control and assurance. They help in measuring the eccentricity of various components, ensuring that they meet the required specifications and standards. This is particularly important in industries such as automotive, aerospace, and manufacturing, where even minor deviations can lead to significant performance issues or safety concerns. For example, in the automotive industry, eccentricity measurement tools are used to check the alignment of wheels and other rotating components, ensuring smooth operation and reducing wear and tear. In the aerospace industry, these tools are used to measure the eccentricity of engine components, ensuring optimal performance and safety. In manufacturing, eccentricity measurement tools are used to check the alignment of various machine parts, ensuring that they operate smoothly and efficiently. In laboratory settings, eccentricity measurement tools are used for research and development purposes. They help in the precise measurement of various components, enabling researchers to study their properties and behavior. This is particularly important in fields such as materials science, where understanding the properties of different materials is crucial for developing new products and technologies. For example, in materials science, eccentricity measurement tools are used to measure the eccentricity of different materials, helping researchers understand their properties and behavior. In the field of metrology, these tools are used to measure the eccentricity of various components, helping researchers develop new measurement techniques and standards. In both industrial and laboratory settings, the use of eccentricity measurement tools is essential for ensuring the quality and performance of various components.

Global Eccentricity Measurement Tools Market Outlook:

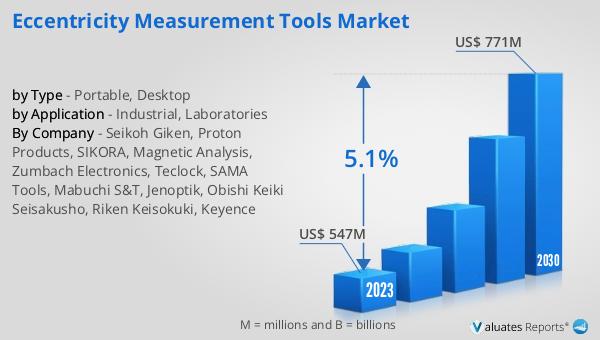

The global Eccentricity Measurement Tools market was valued at US$ 547 million in 2023 and is anticipated to reach US$ 771 million by 2030, witnessing a CAGR of 5.1% during the forecast period 2024-2030. This market growth can be attributed to several factors, including the increasing demand for high-precision components and the growing adoption of automation in manufacturing processes. The market is characterized by a mix of established players and new entrants, all vying to offer innovative solutions to meet the evolving needs of their customers. Technological advancements have also played a significant role in driving market growth, with the development of more sophisticated and accurate measurement tools. These advancements have enabled manufacturers to achieve higher levels of precision and efficiency, thereby enhancing the overall quality and performance of their products. The market is also witnessing increased investment in research and development, aimed at developing new and improved measurement tools. This is expected to further fuel market growth in the coming years. Overall, the global Eccentricity Measurement Tools market is poised for significant growth, driven by the increasing demand for high-precision components and the growing adoption of automation in manufacturing processes.

| Report Metric | Details |

| Report Name | Eccentricity Measurement Tools Market |

| Accounted market size in 2023 | US$ 547 million |

| Forecasted market size in 2030 | US$ 771 million |

| CAGR | 5.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Seikoh Giken, Proton Products, SIKORA, Magnetic Analysis, Zumbach Electronics, Teclock, SAMA Tools, Mabuchi S&T, Jenoptik, Obishi Keiki Seisakusho, Riken Keisokuki, Keyence |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |