What is Global Hospital Workforce Management System Market?

The Global Hospital Workforce Management System Market refers to the comprehensive suite of tools and technologies designed to optimize the management of hospital staff. This market encompasses various software, hardware, and services aimed at improving the efficiency and effectiveness of hospital workforce operations. These systems help in streamlining administrative tasks, reducing labor costs, and ensuring compliance with healthcare regulations. By leveraging advanced analytics and automation, hospital workforce management systems enable healthcare institutions to better manage their human resources, from scheduling and payroll to time and attendance tracking. This market is driven by the increasing demand for efficient healthcare services, the need to reduce operational costs, and the growing adoption of digital solutions in the healthcare sector. As hospitals strive to provide high-quality patient care while managing limited resources, the adoption of workforce management systems is becoming increasingly crucial.

Software, Hardware, Service in the Global Hospital Workforce Management System Market:

In the Global Hospital Workforce Management System Market, software, hardware, and services play pivotal roles in ensuring the smooth operation of hospital workforce management. Software solutions are the backbone of these systems, offering functionalities such as scheduling, payroll management, time and attendance tracking, and analytics. These software applications are designed to integrate seamlessly with existing hospital information systems, providing real-time data and insights that help in making informed decisions. For instance, scheduling software helps in creating efficient staff schedules that align with patient needs and hospital policies, thereby reducing instances of overstaffing or understaffing. Payroll management software automates the calculation of wages, deductions, and benefits, ensuring accurate and timely payments to staff. Time and attendance tracking software monitors employee work hours, leaves, and overtime, helping in maintaining compliance with labor laws and hospital policies. Hardware components, on the other hand, include devices such as biometric scanners, RFID tags, and time clocks that facilitate the accurate tracking of employee attendance and movements within the hospital premises. Biometric scanners, for example, use fingerprint or facial recognition technology to verify employee identities, ensuring that only authorized personnel have access to certain areas of the hospital. RFID tags can be used to track the location of staff and equipment in real-time, enhancing security and operational efficiency. Time clocks, whether traditional punch clocks or modern digital versions, provide a reliable means of recording employee work hours, which can then be integrated with the software for payroll processing and attendance tracking. Services in the Global Hospital Workforce Management System Market include consulting, implementation, training, and support. Consulting services help hospitals assess their workforce management needs and develop customized solutions that address specific challenges. Implementation services ensure that the chosen software and hardware solutions are installed and configured correctly, minimizing disruptions to hospital operations. Training services are crucial for ensuring that hospital staff are proficient in using the new systems, thereby maximizing the benefits of the investment. Support services provide ongoing assistance to address any technical issues or updates required, ensuring that the workforce management system continues to operate smoothly. In summary, the Global Hospital Workforce Management System Market is a complex ecosystem of software, hardware, and services that work together to optimize hospital workforce operations. Software solutions provide the core functionalities needed for efficient workforce management, while hardware components facilitate accurate data collection and monitoring. Services such as consulting, implementation, training, and support ensure that hospitals can effectively adopt and utilize these systems to improve their operational efficiency and deliver high-quality patient care. As the healthcare industry continues to evolve, the adoption of advanced workforce management systems will be essential for hospitals to meet the growing demands and challenges they face.

Payroll, Staffing and Scheduling, Time and Attendance, Patient Classification, Analytics in the Global Hospital Workforce Management System Market:

The usage of Global Hospital Workforce Management System Market in areas such as payroll, staffing and scheduling, time and attendance, patient classification, and analytics is extensive and multifaceted. In payroll management, these systems automate the entire payroll process, from calculating wages and deductions to generating pay slips and ensuring compliance with tax regulations. This not only reduces the administrative burden on hospital HR departments but also minimizes errors and ensures timely payments to staff. By integrating with time and attendance tracking systems, payroll management software can accurately calculate overtime, shift differentials, and other pay-related variables, ensuring that employees are compensated fairly for their work. In staffing and scheduling, workforce management systems enable hospitals to create optimized staff schedules that align with patient care needs and hospital policies. These systems use advanced algorithms to analyze historical data, patient admission rates, and staff availability to generate schedules that minimize instances of overstaffing or understaffing. This ensures that the right number of staff with the appropriate skills are available at all times, enhancing patient care and reducing labor costs. Additionally, these systems can accommodate staff preferences and availability, improving employee satisfaction and reducing turnover rates. Time and attendance tracking is another critical area where workforce management systems are used. These systems provide accurate and real-time tracking of employee work hours, leaves, and overtime. By using biometric scanners, RFID tags, or time clocks, hospitals can ensure that attendance data is accurately recorded and integrated with payroll systems. This not only helps in maintaining compliance with labor laws and hospital policies but also provides valuable insights into employee productivity and attendance patterns. Hospitals can use this data to identify trends, address attendance issues, and implement measures to improve workforce efficiency. Patient classification is another important application of workforce management systems. These systems help hospitals classify patients based on their care needs, acuity levels, and other relevant factors. By accurately classifying patients, hospitals can allocate the appropriate number of staff with the necessary skills to provide the required level of care. This ensures that patients receive timely and appropriate care, improving patient outcomes and satisfaction. Additionally, patient classification data can be used to forecast staffing needs, enabling hospitals to plan and allocate resources more effectively. Analytics is a powerful tool provided by workforce management systems that enables hospitals to gain valuable insights into their workforce operations. By analyzing data on staffing, scheduling, payroll, time and attendance, and patient classification, hospitals can identify trends, inefficiencies, and areas for improvement. For example, analytics can reveal patterns in staff absenteeism, overtime usage, and patient care needs, allowing hospitals to make data-driven decisions to optimize their workforce. Additionally, predictive analytics can be used to forecast future staffing needs, enabling hospitals to proactively plan and allocate resources to meet anticipated demand. In conclusion, the usage of Global Hospital Workforce Management System Market in areas such as payroll, staffing and scheduling, time and attendance, patient classification, and analytics is essential for optimizing hospital workforce operations. These systems automate and streamline administrative tasks, reduce labor costs, ensure compliance with regulations, and provide valuable insights into workforce efficiency. By leveraging these systems, hospitals can improve patient care, enhance employee satisfaction, and achieve operational excellence. As the healthcare industry continues to evolve, the adoption of advanced workforce management systems will be crucial for hospitals to meet the growing demands and challenges they face.

Global Hospital Workforce Management System Market Outlook:

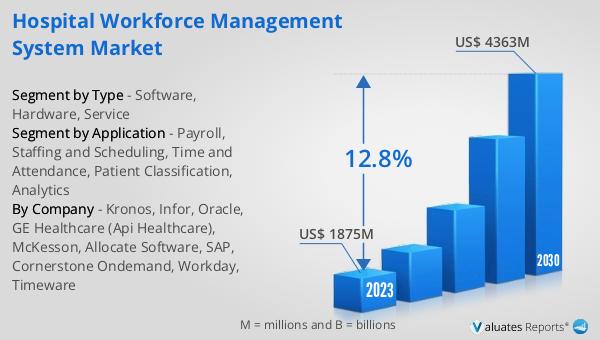

The global Hospital Workforce Management System market was valued at US$ 1875 million in 2023 and is projected to grow significantly, reaching an estimated value of US$ 4363 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 12.8% over the forecast period from 2024 to 2030. This substantial increase underscores the rising importance and adoption of workforce management systems in the healthcare sector. As hospitals and healthcare institutions strive to enhance operational efficiency, reduce costs, and improve patient care, the demand for advanced workforce management solutions is expected to surge. These systems offer a comprehensive suite of tools and technologies that streamline various aspects of workforce management, from scheduling and payroll to time and attendance tracking and analytics. The projected growth in the market reflects the increasing recognition of the benefits these systems provide in optimizing hospital workforce operations. With the healthcare industry facing numerous challenges, including staff shortages, regulatory compliance, and the need for cost-effective solutions, the adoption of workforce management systems is becoming increasingly crucial. This market outlook highlights the significant potential for growth and innovation in the Global Hospital Workforce Management System Market, driven by the ongoing advancements in technology and the evolving needs of the healthcare sector.

| Report Metric | Details |

| Report Name | Hospital Workforce Management System Market |

| Accounted market size in 2023 | US$ 1875 million |

| Forecasted market size in 2030 | US$ 4363 million |

| CAGR | 12.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kronos, Infor, Oracle, GE Healthcare (Api Healthcare), McKesson, Allocate Software, SAP, Cornerstone Ondemand, Workday, Timeware |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |