What is Global Additive Manufacturing with Metal Powders Market?

Global Additive Manufacturing with Metal Powders Market refers to the industry focused on producing metal parts and products using additive manufacturing techniques, commonly known as 3D printing. This market involves the use of metal powders, such as titanium, aluminum, stainless steel, and other alloys, which are melted and fused layer by layer to create complex and precise components. This technology is revolutionizing various industries by offering benefits like reduced material waste, shorter production times, and the ability to create intricate designs that are difficult or impossible to achieve with traditional manufacturing methods. The market is driven by advancements in technology, increasing demand for customized products, and the need for efficient production processes. As industries continue to recognize the potential of additive manufacturing with metal powders, the market is expected to grow significantly, offering new opportunities for innovation and efficiency in manufacturing.

Selective Laser Melting (SLM), Electronic Beam Melting (EBM), Others in the Global Additive Manufacturing with Metal Powders Market:

Selective Laser Melting (SLM), Electronic Beam Melting (EBM), and other techniques are pivotal in the Global Additive Manufacturing with Metal Powders Market. SLM is a popular method that uses a high-powered laser to selectively melt and fuse metal powders, layer by layer, to create a solid object. This technique is known for its precision and ability to produce high-quality parts with complex geometries. SLM is widely used in industries such as aerospace, automotive, and healthcare, where precision and strength are crucial. On the other hand, Electronic Beam Melting (EBM) utilizes an electron beam to melt the metal powder. EBM operates in a vacuum environment, which reduces the risk of contamination and allows for the production of parts with excellent mechanical properties. This method is particularly beneficial for manufacturing large, dense parts and is commonly used in the aerospace and medical industries. Other techniques in the market include Direct Metal Laser Sintering (DMLS), which is similar to SLM but uses a laser to sinter the metal powder instead of melting it completely. DMLS is known for its ability to produce parts with fine details and is often used in the production of prototypes and small batches. Binder Jetting is another technique where a binding agent is selectively deposited onto a powder bed, followed by a curing process to create the final part. This method is advantageous for producing large quantities of parts quickly and cost-effectively. Each of these techniques has its unique advantages and applications, contributing to the overall growth and diversification of the Global Additive Manufacturing with Metal Powders Market. As technology continues to advance, these methods are becoming more efficient and accessible, driving further adoption across various industries.

Aerospace and Defense, Automotive Industrial, Healthcare and Dental, Industrial, Others in the Global Additive Manufacturing with Metal Powders Market:

The usage of Global Additive Manufacturing with Metal Powders Market spans across several key industries, including Aerospace and Defense, Automotive, Healthcare and Dental, Industrial, and others. In the Aerospace and Defense sector, additive manufacturing with metal powders is used to produce lightweight, high-strength components that can withstand extreme conditions. This technology allows for the creation of complex geometries and customized parts, leading to improved performance and fuel efficiency in aircraft and defense systems. In the Automotive industry, additive manufacturing is revolutionizing the production of parts and components, enabling manufacturers to create lightweight, durable, and high-performance parts. This technology also allows for rapid prototyping and customization, reducing the time and cost associated with traditional manufacturing methods. In the Healthcare and Dental sector, additive manufacturing with metal powders is used to produce customized implants, prosthetics, and surgical instruments. This technology allows for the creation of patient-specific solutions, improving the fit and functionality of medical devices. In the Industrial sector, additive manufacturing is used to produce complex machinery parts, tools, and molds, enhancing the efficiency and precision of manufacturing processes. Other industries, such as consumer goods and electronics, are also leveraging this technology to create innovative products with intricate designs and improved performance. The versatility and efficiency of additive manufacturing with metal powders are driving its adoption across various industries, leading to significant advancements in manufacturing capabilities and product development.

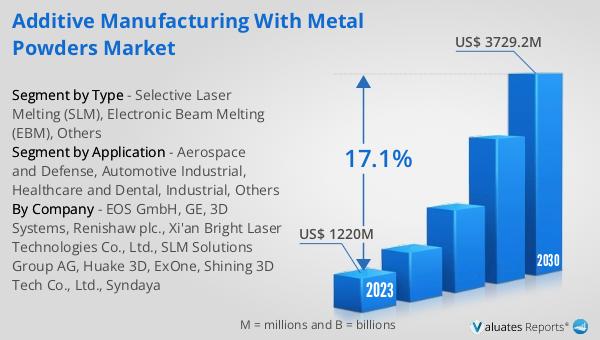

Global Additive Manufacturing with Metal Powders Market Outlook:

The global Additive Manufacturing with Metal Powders market is anticipated to expand from US$ 1446.4 million in 2024 to US$ 3729.2 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 17.1% during the forecast period. The top five global manufacturers collectively hold a market share exceeding 40%. Europe stands as the largest market, accounting for over 35% of the total share, followed by Asia-Pacific and North America, which together represent about 60% of the market. In terms of product segmentation, Selective Laser Melting (SLM) dominates with a share exceeding 70%. This significant growth is driven by the increasing adoption of additive manufacturing technologies across various industries, advancements in technology, and the rising demand for customized and efficient production processes. The market's expansion is also supported by the continuous development of new materials and techniques, enhancing the capabilities and applications of additive manufacturing with metal powders. As industries continue to recognize the benefits of this technology, the market is expected to witness substantial growth, offering new opportunities for innovation and efficiency in manufacturing.

| Report Metric | Details |

| Report Name | Additive Manufacturing with Metal Powders Market |

| Accounted market size in 2024 | US$ 1446.4 million |

| Forecasted market size in 2030 | US$ 3729.2 million |

| CAGR | 17.1 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | EOS GmbH, GE, 3D Systems, Renishaw plc., Xi'an Bright Laser Technologies Co., Ltd., SLM Solutions Group AG, Huake 3D, ExOne, Shining 3D Tech Co., Ltd., Syndaya |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |