What is Global Shikimic Acid Market?

The Global Shikimic Acid Market refers to the worldwide trade and utilization of shikimic acid, a naturally occurring compound primarily derived from the star anise plant. Shikimic acid is a crucial intermediate in the biosynthesis of many aromatic compounds and is extensively used in the pharmaceutical industry, particularly for the production of antiviral drugs like oseltamivir (Tamiflu). The market encompasses the entire supply chain, from raw material extraction to the final product's distribution. It includes various stakeholders such as manufacturers, suppliers, distributors, and end-users. The demand for shikimic acid is driven by its applications in medicine, cosmetics, and other industries. The market is influenced by factors such as raw material availability, technological advancements, regulatory policies, and global health trends. The increasing prevalence of viral infections and the growing demand for natural and organic products are expected to boost the market's growth.

Shikimic Acid (98%), Shikimic Acid (99%) in the Global Shikimic Acid Market:

Shikimic Acid (98%) and Shikimic Acid (99%) are two primary grades of shikimic acid available in the global market. Shikimic Acid (98%) refers to the compound with a purity level of 98%, while Shikimic Acid (99%) has a higher purity level of 99%. These purity levels are crucial as they determine the compound's suitability for various applications. Shikimic Acid (98%) is often used in applications where ultra-high purity is not critical, such as in certain cosmetic formulations and some pharmaceutical intermediates. On the other hand, Shikimic Acid (99%) is preferred for high-precision applications, particularly in the pharmaceutical industry, where the highest purity is essential for drug formulation and efficacy. The production of these different grades involves sophisticated extraction and purification processes to ensure the desired purity levels. The choice between Shikimic Acid (98%) and Shikimic Acid (99%) depends on the specific requirements of the end-use application. For instance, in the production of antiviral drugs like oseltamivir, Shikimic Acid (99%) is preferred due to its higher purity, which ensures the effectiveness and safety of the final product. The global market for these grades is influenced by factors such as raw material availability, technological advancements in extraction and purification processes, and the demand from end-use industries. The increasing focus on natural and organic products has also led to a rise in demand for high-purity shikimic acid, particularly in the pharmaceutical and cosmetic industries. Additionally, regulatory standards and quality control measures play a significant role in determining the market dynamics for these different grades of shikimic acid. Manufacturers are continually investing in research and development to improve the extraction and purification processes, thereby enhancing the quality and yield of shikimic acid. The competitive landscape of the global shikimic acid market is characterized by the presence of several key players who are engaged in the production and distribution of these different grades. These players are focusing on strategic collaborations, mergers, and acquisitions to expand their market presence and enhance their product offerings. The market is also witnessing a trend towards sustainable and eco-friendly production methods, driven by the increasing consumer preference for natural and organic products. This trend is expected to further boost the demand for high-purity shikimic acid in the coming years.

Medicine and Veterinary Drugs, Cosmetic and Personal Care, Others in the Global Shikimic Acid Market:

The Global Shikimic Acid Market finds extensive usage in various sectors, including Medicine and Veterinary Drugs, Cosmetic and Personal Care, and others. In the field of Medicine and Veterinary Drugs, shikimic acid is primarily used as a key intermediate in the synthesis of antiviral drugs, most notably oseltamivir (Tamiflu), which is used to treat influenza. The compound's ability to inhibit viral replication makes it a valuable component in the development of antiviral therapies. Additionally, shikimic acid is used in the production of other pharmaceutical intermediates and active pharmaceutical ingredients (APIs), contributing to its high demand in the medical sector. In Veterinary Drugs, shikimic acid is utilized for similar purposes, aiding in the development of antiviral medications for animals. In the Cosmetic and Personal Care industry, shikimic acid is valued for its natural origin and beneficial properties. It is used in various skincare and cosmetic products due to its antioxidant and anti-inflammatory properties. Shikimic acid helps in reducing skin inflammation, improving skin texture, and providing a natural glow, making it a popular ingredient in anti-aging and skin-brightening formulations. The demand for natural and organic ingredients in cosmetics has further propelled the use of shikimic acid in this sector. Other applications of shikimic acid include its use in the food and beverage industry as a flavoring agent and in the agricultural sector as a plant growth regulator. The compound's versatility and wide range of applications make it a valuable commodity in the global market. The increasing awareness about the benefits of natural and organic products, coupled with the rising prevalence of viral infections, is expected to drive the demand for shikimic acid across these sectors. The market dynamics are influenced by factors such as raw material availability, technological advancements, regulatory policies, and consumer preferences. Manufacturers are focusing on sustainable and eco-friendly production methods to meet the growing demand for high-quality shikimic acid. The competitive landscape of the global shikimic acid market is characterized by the presence of several key players who are engaged in the production and distribution of shikimic acid for various applications. These players are adopting strategies such as mergers, acquisitions, and collaborations to expand their market presence and enhance their product offerings. The market is also witnessing a trend towards the development of innovative products and formulations that incorporate shikimic acid, driven by the increasing consumer preference for natural and organic products.

Global Shikimic Acid Market Outlook:

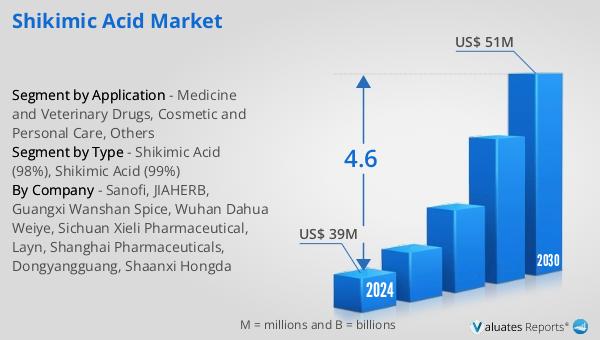

The global Shikimic Acid market is anticipated to expand from US$ 39 million in 2024 to US$ 51 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period. The market is dominated by the top five manufacturers, who collectively hold a market share exceeding 70%. China emerges as the largest market, commanding a share of over 80%, followed by Europe, which holds a share of approximately 20%. This growth trajectory is indicative of the increasing demand for shikimic acid across various sectors, driven by its extensive applications in pharmaceuticals, cosmetics, and other industries. The dominance of China in the market can be attributed to the abundant availability of raw materials and advanced extraction technologies. The European market, while smaller in comparison, is also significant due to the high demand for natural and organic products in the region. The competitive landscape of the global shikimic acid market is characterized by the presence of several key players who are focusing on strategic collaborations, mergers, and acquisitions to enhance their market presence and product offerings. The market dynamics are influenced by factors such as raw material availability, technological advancements, regulatory policies, and consumer preferences. The increasing awareness about the benefits of natural and organic products, coupled with the rising prevalence of viral infections, is expected to drive the demand for shikimic acid in the coming years.

| Report Metric | Details |

| Report Name | Shikimic Acid Market |

| Accounted market size in 2024 | US$ 39 million |

| Forecasted market size in 2030 | US$ 51 million |

| CAGR | 4.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Sanofi, JIAHERB, Guangxi Wanshan Spice, Wuhan Dahua Weiye, Sichuan Xieli Pharmaceutical, Layn, Shanghai Pharmaceuticals, Dongyangguang, Shaanxi Hongda |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |