What is Global Plastic Diaphragm Pumps Market?

The Global Plastic Diaphragm Pumps Market refers to the worldwide industry focused on the production, distribution, and utilization of plastic diaphragm pumps. These pumps are essential in various industries due to their ability to handle a wide range of fluids, including corrosive and abrasive substances. Unlike metal pumps, plastic diaphragm pumps are resistant to chemical reactions, making them ideal for applications where metal pumps would corrode or degrade. The market encompasses different types of plastic diaphragm pumps, including air-operated and electrically operated variants, each designed to meet specific industrial needs. The demand for these pumps is driven by their versatility, durability, and cost-effectiveness, making them a preferred choice in sectors such as water and wastewater management, oil and gas, chemicals, and food and beverages. As industries continue to seek efficient and reliable pumping solutions, the global plastic diaphragm pumps market is expected to grow, driven by technological advancements and increasing applications across various sectors.

Air Operated Diaphragm Pump, Electrically Operated Diaphragm Pump, Others in the Global Plastic Diaphragm Pumps Market:

Air Operated Diaphragm Pumps (AODD) are a significant segment within the Global Plastic Diaphragm Pumps Market. These pumps operate using compressed air, which drives the diaphragms to move back and forth, creating a pumping action. AODD pumps are highly versatile and can handle a wide range of fluids, including viscous, abrasive, and corrosive liquids. They are commonly used in industries where electricity is not readily available or where explosive environments require non-electrical equipment. The simplicity of their design, combined with their ability to self-prime and run dry without damage, makes them a popular choice in various applications. Electrically Operated Diaphragm Pumps, on the other hand, use an electric motor to drive the diaphragms. These pumps offer precise control over the flow rate and pressure, making them suitable for applications that require consistent and accurate fluid handling. They are often used in automated systems where integration with other electronic controls is necessary. Electrically operated pumps are known for their efficiency and reliability, providing a steady performance in demanding environments. Other types of plastic diaphragm pumps include hydraulically operated and mechanically operated variants. These pumps cater to specific needs where air or electric power may not be the most efficient or feasible option. Hydraulic diaphragm pumps use hydraulic fluid to drive the diaphragms, offering high pressure and flow capabilities. Mechanically operated diaphragm pumps use mechanical linkages to move the diaphragms, providing a robust and straightforward solution for certain applications. Each type of plastic diaphragm pump has its unique advantages and is chosen based on the specific requirements of the application, such as the type of fluid being pumped, the required flow rate, and the operating environment. The diversity in pump types ensures that there is a suitable solution for virtually any pumping need within the global market.

Water & Wastewater, Oil & Gas, Chemicals, Food & Beverages, Others in the Global Plastic Diaphragm Pumps Market:

The Global Plastic Diaphragm Pumps Market finds extensive usage across various industries, including water and wastewater management, oil and gas, chemicals, food and beverages, and others. In the water and wastewater sector, plastic diaphragm pumps are used for transferring and treating water, handling sludge, and dosing chemicals. Their resistance to corrosion and ability to handle abrasive materials make them ideal for these applications. In the oil and gas industry, these pumps are used for transferring crude oil, chemicals, and other fluids. Their ability to operate in harsh environments and handle a wide range of viscosities makes them indispensable in this sector. The chemical industry relies on plastic diaphragm pumps for transferring and dosing aggressive chemicals, acids, and solvents. The pumps' chemical resistance and ability to handle hazardous materials safely are crucial in these applications. In the food and beverage industry, plastic diaphragm pumps are used for transferring ingredients, dosing additives, and handling cleaning solutions. Their sanitary design and ability to handle a variety of fluids without contamination make them suitable for this sector. Other industries that utilize plastic diaphragm pumps include pharmaceuticals, mining, and agriculture. In pharmaceuticals, these pumps are used for transferring and dosing sensitive fluids, ensuring precise and contamination-free handling. In mining, they are used for dewatering, transferring slurry, and handling abrasive materials. In agriculture, plastic diaphragm pumps are used for irrigation, fertilization, and pesticide application. The versatility and reliability of plastic diaphragm pumps make them a preferred choice across these diverse industries, driving their demand in the global market.

Global Plastic Diaphragm Pumps Market Outlook:

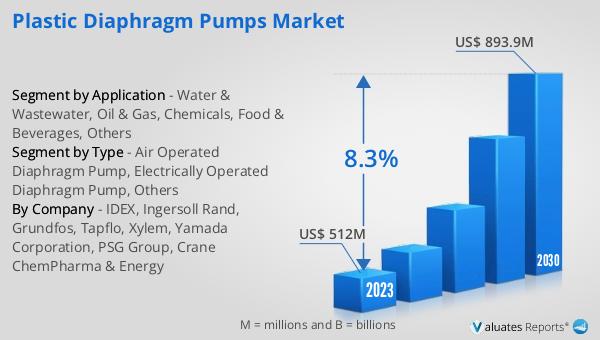

The global Plastic Diaphragm Pumps market was valued at US$ 512 million in 2023 and is anticipated to reach US$ 893.9 million by 2030, witnessing a CAGR of 8.3% during the forecast period 2024-2030. This significant growth reflects the increasing demand for efficient and reliable pumping solutions across various industries. The market's expansion is driven by the versatility and durability of plastic diaphragm pumps, which can handle a wide range of fluids, including corrosive and abrasive substances. As industries continue to seek cost-effective and reliable pumping solutions, the global plastic diaphragm pumps market is expected to grow, driven by technological advancements and increasing applications across various sectors. The market's growth is also supported by the rising need for efficient water and wastewater management, the expansion of the oil and gas industry, and the increasing demand for chemical and food and beverage processing. The ability of plastic diaphragm pumps to operate in harsh environments and handle a wide range of viscosities makes them indispensable in these sectors. As a result, the global plastic diaphragm pumps market is poised for significant growth in the coming years.

| Report Metric | Details |

| Report Name | Plastic Diaphragm Pumps Market |

| Accounted market size in 2023 | US$ 512 million |

| Forecasted market size in 2030 | US$ 893.9 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | IDEX, Ingersoll Rand, Grundfos, Tapflo, Xylem, Yamada Corporation, PSG Group, Crane ChemPharma & Energy |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |