What is Global Tahini Market?

The global Tahini market is a rapidly growing sector within the food industry, driven by increasing consumer awareness and demand for healthy, natural, and versatile food products. Tahini, a paste made from ground sesame seeds, is a staple in Middle Eastern cuisine but has gained popularity worldwide due to its rich flavor and nutritional benefits. It is used in a variety of dishes, from savory to sweet, and is known for its high content of healthy fats, protein, and essential vitamins and minerals. The market encompasses a wide range of products, including hulled and unhulled tahini, each offering unique textures and flavors. The growth of the global tahini market is fueled by the rising trend of plant-based diets, the increasing popularity of ethnic foods, and the expanding use of tahini in various culinary applications. As consumers continue to seek out nutritious and flavorful food options, the demand for tahini is expected to rise, making it a significant player in the global food market.

Hulled Tahini, Unhulled Tahini in the Global Tahini Market:

Hulled tahini and unhulled tahini are two primary types of tahini available in the global market, each with distinct characteristics and uses. Hulled tahini is made from sesame seeds that have had their outer husks removed before grinding. This process results in a smoother, creamier texture and a milder flavor compared to unhulled tahini. Hulled tahini is often preferred for its lighter color and less bitter taste, making it a popular choice for use in sauces, dressings, and spreads. It is also easier to digest and has a slightly lower fiber content than unhulled tahini. On the other hand, unhulled tahini is made from whole sesame seeds, including the husks. This gives it a darker color, a thicker consistency, and a more robust, slightly bitter flavor. Unhulled tahini is richer in nutrients, particularly fiber, calcium, and other minerals, due to the presence of the husks. It is often used in recipes where a stronger sesame flavor is desired, such as in traditional Middle Eastern dishes like halva and certain types of hummus. Both types of tahini offer unique benefits and can be used interchangeably depending on the desired taste and texture of the final dish. The choice between hulled and unhulled tahini often comes down to personal preference and specific culinary applications. As the global tahini market continues to expand, consumers are becoming more aware of the differences between these two types and are making informed choices based on their nutritional needs and taste preferences.

Paste & Spreads, Halva & Other Sweets, Sauces & Dips, Others in the Global Tahini Market:

The global tahini market finds extensive usage in various culinary applications, including paste and spreads, halva and other sweets, sauces and dips, and other diverse uses. In the realm of pastes and spreads, tahini is a key ingredient due to its creamy texture and rich flavor. It is commonly used as a base for spreads like hummus, where it adds a nutty depth and smooth consistency. Tahini spreads are also popular as a healthy alternative to traditional nut butters, offering a unique taste and a wealth of nutritional benefits. In the category of halva and other sweets, tahini plays a crucial role. Halva, a traditional Middle Eastern confection, relies heavily on tahini for its distinctive flavor and texture. The natural sweetness and rich, nutty taste of tahini make it an ideal ingredient in various sweet treats, from cookies and cakes to energy bars and desserts. Tahini's versatility extends to sauces and dips, where it is used to create a wide range of flavorful and nutritious options. Tahini-based sauces are a staple in Middle Eastern cuisine, often used to dress salads, grilled meats, and vegetables. Its creamy consistency and ability to blend well with other ingredients make it a popular choice for creating dips like baba ghanoush and tahini sauce. Beyond these specific categories, tahini is also used in a variety of other culinary applications. It can be incorporated into smoothies for added creaminess and nutrition, used as a base for marinades, or even added to baked goods for a unique flavor twist. The growing popularity of tahini in global cuisine is a testament to its versatility and the increasing consumer demand for healthy, natural, and flavorful food options. As the global tahini market continues to expand, its usage in these diverse culinary applications is expected to grow, further cementing its place as a staple ingredient in kitchens around the world.

Global Tahini Market Outlook:

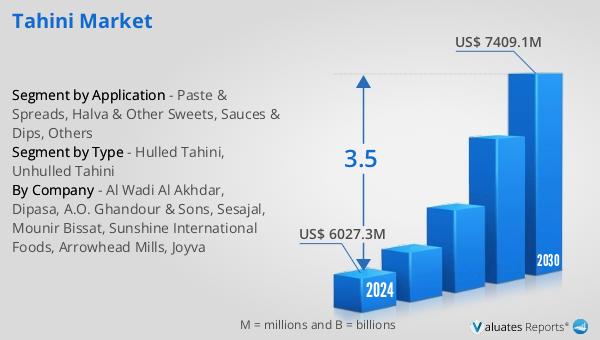

The global tahini market is anticipated to experience significant growth, with projections indicating an increase from US$ 6027.3 million in 2024 to US$ 7409.1 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.5% during the forecast period. Asia, excluding China, emerges as the largest tahini market, holding approximately 36% of the market share. China follows closely, accounting for about 25% of the market share. The top three companies in the tahini market collectively occupy around 6% of the market share. This growth is driven by the rising consumer awareness of the health benefits associated with tahini, its versatility in culinary applications, and the increasing popularity of ethnic foods. The expanding use of tahini in various food products, from spreads and sauces to sweets and baked goods, further fuels its market growth. As consumers continue to seek out nutritious and flavorful food options, the demand for tahini is expected to rise, making it a significant player in the global food market.

| Report Metric | Details |

| Report Name | Tahini Market |

| Accounted market size in 2024 | US$ 6027.3 in million |

| Forecasted market size in 2030 | US$ 7409.1 million |

| CAGR | 3.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Al Wadi Al Akhdar, Dipasa, A.O. Ghandour & Sons, Sesajal, Mounir Bissat, Sunshine International Foods, Arrowhead Mills, Joyva |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |