What is Global Medical Package Inspection System Market?

The Global Medical Package Inspection System Market refers to the industry focused on the development, production, and distribution of systems designed to inspect medical packages. These systems ensure that medical products are packaged correctly and safely, preventing contamination and ensuring the integrity of the products. They are crucial in maintaining the quality and safety standards required in the medical field. The market includes various types of inspection systems, such as visual inspection systems, X-ray inspection systems, and leak detection systems. These systems are used to detect defects, contaminants, and other issues that could compromise the safety and efficacy of medical products. The market is driven by the increasing demand for safe and reliable medical products, stringent regulatory requirements, and advancements in inspection technologies. As the healthcare industry continues to grow, the need for effective package inspection systems is expected to rise, making this market an essential component of the global medical industry.

Automatic, Semi-automatic in the Global Medical Package Inspection System Market:

In the Global Medical Package Inspection System Market, systems can be categorized into automatic and semi-automatic types. Automatic inspection systems are designed to operate with minimal human intervention. They use advanced technologies such as machine vision, artificial intelligence, and robotics to inspect medical packages quickly and accurately. These systems are highly efficient and can handle large volumes of packages, making them ideal for large-scale production environments. They are capable of detecting a wide range of defects, including cracks, leaks, and contamination, ensuring that only high-quality products reach the market. On the other hand, semi-automatic inspection systems require some level of human involvement. While they also use advanced technologies to inspect packages, they rely on operators to perform certain tasks, such as loading and unloading packages or making final decisions on borderline cases. These systems are typically more flexible and can be adjusted to handle different types of packages and inspection criteria. They are often used in smaller production environments or for specialized applications where a high degree of customization is required. Both types of systems play a crucial role in ensuring the safety and quality of medical products. Automatic systems offer the advantage of speed and consistency, making them suitable for high-volume production. Semi-automatic systems, on the other hand, provide greater flexibility and can be more cost-effective for smaller operations. The choice between automatic and semi-automatic systems depends on various factors, including the size of the production facility, the type of products being inspected, and the specific requirements of the inspection process. As technology continues to advance, the capabilities of both types of systems are expected to improve, further enhancing their effectiveness and efficiency.

Medical, Pharmaceutical, Health Products in the Global Medical Package Inspection System Market:

The Global Medical Package Inspection System Market finds extensive usage in the medical, pharmaceutical, and health products sectors. In the medical field, these inspection systems are used to ensure that medical devices and equipment are packaged correctly and free from defects. This is crucial for maintaining the sterility and functionality of medical products, which can directly impact patient safety and treatment outcomes. For example, surgical instruments, implants, and diagnostic devices must be thoroughly inspected to prevent any contamination or damage that could compromise their performance. In the pharmaceutical sector, package inspection systems are essential for ensuring the safety and efficacy of medications. These systems are used to detect defects in packaging, such as leaks, cracks, or improper seals, which could lead to contamination or degradation of the drugs. This is particularly important for products such as vaccines, injectable drugs, and other sterile medications, where even minor defects can have serious consequences. Additionally, inspection systems help to verify the accuracy of labeling and ensure that the correct dosage and expiration information is provided, which is critical for patient safety and regulatory compliance. In the health products sector, package inspection systems are used to ensure the quality and safety of a wide range of products, including dietary supplements, personal care items, and over-the-counter medications. These systems help to detect any defects or contaminants that could affect the safety and effectiveness of the products. For example, inspection systems can identify issues such as broken seals, foreign particles, or incorrect labeling, which could pose risks to consumers. By ensuring that health products are packaged correctly and free from defects, these systems help to protect consumer health and maintain trust in the products. Overall, the use of package inspection systems in the medical, pharmaceutical, and health products sectors is essential for ensuring the safety, quality, and efficacy of a wide range of products.

Global Medical Package Inspection System Market Outlook:

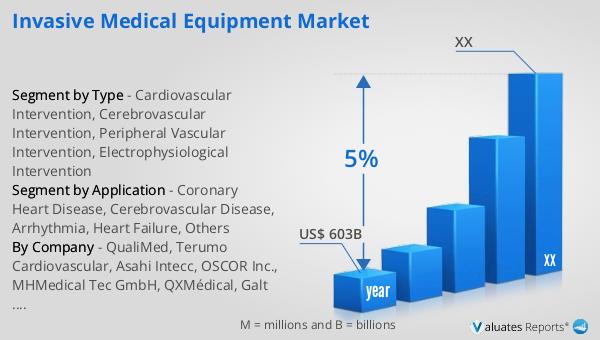

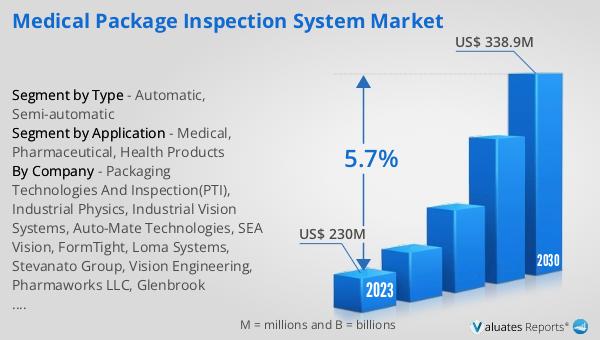

The global Medical Package Inspection System market was valued at US$ 230 million in 2023 and is anticipated to reach US$ 338.9 million by 2030, witnessing a CAGR of 5.7% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth is driven by the increasing demand for safe and reliable medical products, stringent regulatory requirements, and advancements in inspection technologies. As the healthcare industry continues to expand, the need for effective package inspection systems is expected to rise, making this market an essential component of the global medical industry. The market outlook indicates a positive trend, with significant growth opportunities for companies operating in this space. The increasing focus on patient safety and product quality, coupled with technological advancements, is expected to drive the demand for medical package inspection systems in the coming years.

| Report Metric | Details |

| Report Name | Medical Package Inspection System Market |

| Accounted market size in 2023 | US$ 230 million |

| Forecasted market size in 2030 | US$ 338.9 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Packaging Technologies And Inspection(PTI), Industrial Physics, Industrial Vision Systems, Auto-Mate Technologies, SEA Vision, FormTight, Loma Systems, Stevanato Group, Vision Engineering, Pharmaworks LLC, Glenbrook Technologies, Labthink International, Pfeiffer Vacuum, TM Electronics, FSI Technologies, Cognex Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |