What is Global Micro Gas Turbine Engines Market?

The Global Micro Gas Turbine Engines Market is a specialized segment within the broader energy and power generation industry. These engines are compact, lightweight, and efficient, making them ideal for various applications where space and weight are critical factors. Micro gas turbine engines typically range from a few kilowatts to several hundred kilowatts in power output. They operate on various fuels, including natural gas, diesel, and biofuels, providing flexibility in different environments and applications. The market for these engines is driven by the increasing demand for decentralized power generation, the need for cleaner and more efficient energy solutions, and advancements in technology that enhance their performance and reliability. Additionally, the growing emphasis on reducing carbon emissions and improving energy efficiency in various sectors further propels the adoption of micro gas turbine engines. These engines are used in a wide range of applications, including automotive, aerospace and defense, commercial buildings, and other industrial uses, making them a versatile solution for modern energy needs.

<300 KW, 200-600 KW, >600 KW in the Global Micro Gas Turbine Engines Market:

Micro gas turbine engines are categorized based on their power output, typically into three segments: <300 KW, 200-600 KW, and >600 KW. The <300 KW segment includes engines that are suitable for small-scale applications such as residential power generation, small commercial buildings, and backup power systems. These engines are valued for their compact size, ease of installation, and ability to provide reliable power in remote or off-grid locations. They are also used in hybrid electric vehicles, where their small size and efficiency make them ideal for providing auxiliary power. The 200-600 KW segment caters to medium-sized applications, including larger commercial buildings, small industrial facilities, and distributed energy systems. These engines offer a balance between power output and efficiency, making them suitable for combined heat and power (CHP) systems, where they can simultaneously generate electricity and useful thermal energy. This dual functionality enhances their appeal in sectors looking to improve energy efficiency and reduce operational costs. Additionally, these engines are used in microgrids, providing a reliable and flexible power source that can operate independently or in conjunction with the main grid. The >600 KW segment represents the high-power end of the micro gas turbine engine market. These engines are used in large industrial facilities, utility-scale power generation, and large commercial complexes. Their high power output and efficiency make them suitable for applications requiring substantial and continuous power supply. They are also used in large-scale CHP systems, where their ability to generate significant amounts of electricity and thermal energy can lead to substantial cost savings and environmental benefits. Furthermore, these engines are employed in critical infrastructure, such as hospitals and data centers, where uninterrupted power supply is crucial. Each of these segments addresses specific needs and applications, highlighting the versatility and adaptability of micro gas turbine engines. The <300 KW engines are ideal for small-scale and remote applications, the 200-600 KW engines serve medium-sized facilities and distributed energy systems, and the >600 KW engines cater to large-scale industrial and commercial applications. This segmentation allows manufacturers and users to select the most appropriate engine based on their specific power requirements, operational conditions, and efficiency goals.

Automotive, Aerospace and Defense, Commercial, Others in the Global Micro Gas Turbine Engines Market:

Micro gas turbine engines find extensive usage across various sectors, including automotive, aerospace and defense, commercial, and others. In the automotive sector, these engines are primarily used in hybrid electric vehicles (HEVs) and range extenders. Their compact size, lightweight, and high efficiency make them ideal for providing auxiliary power, improving fuel efficiency, and reducing emissions. They can also be used in off-road vehicles and specialty vehicles where traditional internal combustion engines may not be suitable due to space or weight constraints. In the aerospace and defense sector, micro gas turbine engines are used in unmanned aerial vehicles (UAVs), auxiliary power units (APUs), and portable power systems. Their high power-to-weight ratio and reliability make them suitable for UAVs, where weight and endurance are critical factors. In military applications, these engines provide reliable power for various equipment and systems, enhancing operational capabilities in remote or hostile environments. They are also used in APUs for aircraft, providing power for onboard systems when the main engines are not running, thereby improving overall efficiency and reducing fuel consumption. The commercial sector utilizes micro gas turbine engines in combined heat and power (CHP) systems, distributed energy systems, and backup power solutions. In CHP systems, these engines generate both electricity and useful thermal energy, improving overall energy efficiency and reducing operational costs. They are used in commercial buildings, hotels, hospitals, and other facilities where continuous and reliable power supply is essential. In distributed energy systems, micro gas turbine engines provide a flexible and scalable power source that can operate independently or in conjunction with the main grid, enhancing energy security and resilience. Other applications of micro gas turbine engines include industrial processes, remote power generation, and renewable energy integration. In industrial processes, these engines provide reliable and efficient power for various equipment and systems, improving productivity and reducing energy costs. In remote power generation, they offer a viable solution for providing electricity in off-grid or hard-to-reach locations, where traditional power infrastructure may not be feasible. Additionally, micro gas turbine engines can be integrated with renewable energy sources, such as solar or wind, to provide a stable and continuous power supply, addressing the intermittency issues associated with renewables. Overall, the versatility and adaptability of micro gas turbine engines make them suitable for a wide range of applications across different sectors. Their ability to provide reliable, efficient, and clean power solutions addresses the growing demand for decentralized and sustainable energy systems.

Global Micro Gas Turbine Engines Market Outlook:

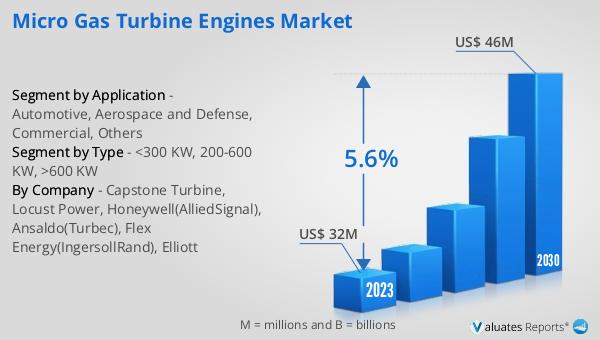

The global Micro Gas Turbine Engines market was valued at US$ 32 million in 2023 and is anticipated to reach US$ 46 million by 2030, witnessing a CAGR of 5.6% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing adoption of micro gas turbine engines across various sectors. The rising demand for decentralized power generation, coupled with the need for cleaner and more efficient energy solutions, drives the market's expansion. Technological advancements that enhance the performance and reliability of these engines further contribute to their growing popularity. Additionally, the emphasis on reducing carbon emissions and improving energy efficiency in different industries supports the market's positive trajectory. As more sectors recognize the benefits of micro gas turbine engines, their adoption is expected to increase, leading to sustained market growth over the forecast period.

| Report Metric | Details |

| Report Name | Micro Gas Turbine Engines Market |

| Accounted market size in 2023 | US$ 32 million |

| Forecasted market size in 2030 | US$ 46 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Capstone Turbine, Locust Power, Honeywell(AlliedSignal), Ansaldo(Turbec), Flex Energy(IngersollRand), Elliott |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |