What is Global Medical Adhesive Plaster Market?

The Global Medical Adhesive Plaster Market refers to the worldwide industry focused on the production and distribution of medical adhesive plasters. These plasters are essential in healthcare for covering wounds, securing dressings, and providing support to injured areas. They are designed to adhere to the skin without causing irritation and are used in various medical settings, including hospitals, clinics, and home care. The market encompasses a wide range of products, from simple adhesive bandages to more specialized plasters with advanced features like waterproofing and hypoallergenic materials. The demand for medical adhesive plasters is driven by factors such as the increasing prevalence of chronic wounds, the rising number of surgical procedures, and the growing awareness about the importance of wound care. Additionally, advancements in medical technology and the development of new materials have led to the creation of more effective and comfortable adhesive plasters, further boosting market growth. The global reach of this market means that these products are used by healthcare professionals and patients around the world, making it a vital component of the medical supplies industry.

Zinc Oxide Adhesive Plaster, Ordinary Adhesive Plaster in the Global Medical Adhesive Plaster Market:

Zinc oxide adhesive plaster and ordinary adhesive plaster are two significant types of products within the Global Medical Adhesive Plaster Market. Zinc oxide adhesive plaster is a type of medical tape that contains zinc oxide, which helps to prevent infections and promote healing. It is commonly used for securing dressings, catheters, and other medical devices to the skin. The zinc oxide component provides an added benefit of reducing the risk of skin irritation and allergic reactions, making it suitable for patients with sensitive skin. These plasters are often used in situations where long-term adhesion is required, such as in the treatment of chronic wounds or post-surgical care. On the other hand, ordinary adhesive plaster, also known as adhesive bandage or sticking plaster, is a more general-purpose product used for covering minor cuts, abrasions, and blisters. These plasters are typically made from a flexible fabric or plastic material with an adhesive backing and a small, absorbent pad in the center to cover the wound. Ordinary adhesive plasters are widely used in both professional healthcare settings and home care due to their ease of use and availability in various sizes and shapes. They are an essential item in first aid kits and are often the first line of defense in wound care. The Global Medical Adhesive Plaster Market includes a diverse range of products to meet the varying needs of patients and healthcare providers. Innovations in materials and adhesive technologies have led to the development of plasters that are more comfortable, durable, and effective. For example, some modern adhesive plasters are designed to be waterproof, allowing patients to bathe or swim without having to replace the plaster. Others are made with hypoallergenic materials to minimize the risk of skin reactions. The market also includes specialized plasters for specific applications, such as those designed for use on joints or areas with high movement, which require greater flexibility and adhesion. The growing demand for medical adhesive plasters is also driven by the increasing prevalence of chronic conditions such as diabetes, which can lead to slow-healing wounds that require ongoing care. Additionally, the rising number of surgical procedures worldwide has increased the need for reliable and effective wound care products. As the global population continues to age, the demand for medical adhesive plasters is expected to grow, as older adults are more prone to injuries and chronic wounds. The market is also influenced by regional factors, such as differences in healthcare infrastructure, economic conditions, and cultural practices related to wound care. In developed regions, there is a higher demand for advanced wound care products, while in developing regions, there may be a greater need for affordable and accessible options. Overall, the Global Medical Adhesive Plaster Market is a dynamic and evolving industry that plays a crucial role in healthcare by providing essential products for wound care and medical device fixation.

Hospitals, Ambulatory Surgery Center, Clinics, Home Care in the Global Medical Adhesive Plaster Market:

The usage of Global Medical Adhesive Plaster Market products spans across various healthcare settings, including hospitals, ambulatory surgery centers, clinics, and home care. In hospitals, medical adhesive plasters are indispensable for a wide range of applications. They are used to secure dressings over surgical incisions, cover wounds, and attach medical devices such as catheters and IV lines. The high demand for these products in hospitals is driven by the need for reliable and effective wound care solutions that can withstand the rigors of a hospital environment. Medical adhesive plasters used in hospitals must meet stringent standards for sterility, adhesion, and patient comfort. In ambulatory surgery centers, where patients undergo surgical procedures that do not require an overnight stay, medical adhesive plasters are equally important. These centers rely on high-quality adhesive plasters to ensure that surgical wounds are properly covered and protected during the recovery process. The use of medical adhesive plasters in ambulatory surgery centers helps to minimize the risk of infection and promote faster healing, allowing patients to return home with confidence. Clinics, which provide a wide range of outpatient services, also depend on medical adhesive plasters for wound care and medical device fixation. In these settings, adhesive plasters are used to cover minor injuries, secure dressings, and attach medical devices. The convenience and versatility of medical adhesive plasters make them a staple in clinic settings, where quick and effective wound care is essential. Home care is another significant area where medical adhesive plasters are widely used. Patients who require ongoing wound care or have chronic conditions that necessitate regular dressing changes often rely on medical adhesive plasters for their daily care needs. The ease of use and availability of these products make them ideal for home care settings, where patients or caregivers can apply and change dressings as needed. Medical adhesive plasters used in home care must be designed for comfort and ease of application, as they are often used by individuals without formal medical training. The growing trend of home healthcare, driven by factors such as an aging population and the increasing prevalence of chronic diseases, has further boosted the demand for medical adhesive plasters in this setting. In all these healthcare settings, the choice of medical adhesive plaster depends on various factors, including the type of wound, the patient's skin condition, and the required duration of adhesion. For example, in hospitals and ambulatory surgery centers, where surgical wounds need to be covered for extended periods, plasters with strong adhesion and durability are preferred. In contrast, in home care settings, where dressings may need to be changed frequently, plasters that are easy to apply and remove without causing skin irritation are more suitable. The Global Medical Adhesive Plaster Market continues to evolve to meet the diverse needs of these healthcare settings. Innovations in adhesive technologies and materials have led to the development of plasters that offer improved performance, comfort, and safety. For instance, some modern medical adhesive plasters are designed to be breathable, allowing air to reach the wound and promote faster healing. Others are made with hypoallergenic materials to reduce the risk of skin reactions, making them suitable for patients with sensitive skin. Overall, the usage of medical adhesive plasters in hospitals, ambulatory surgery centers, clinics, and home care highlights the critical role these products play in wound care and medical device fixation. The Global Medical Adhesive Plaster Market is poised to continue growing as healthcare providers and patients seek reliable and effective solutions for wound care and medical device fixation across various settings.

Global Medical Adhesive Plaster Market Outlook:

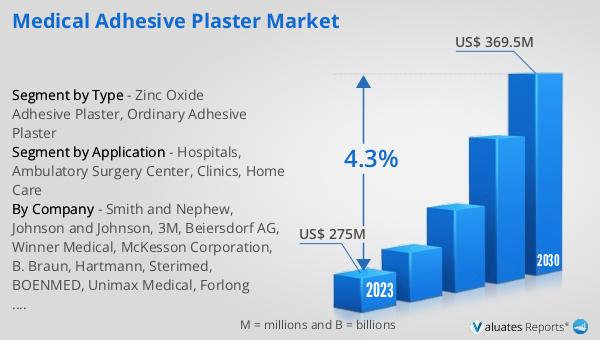

The global Medical Adhesive Plaster market was valued at US$ 275 million in 2023 and is anticipated to reach US$ 369.5 million by 2030, witnessing a CAGR of 4.3% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth reflects the increasing demand for medical adhesive plasters as essential components in wound care and medical device fixation. The rising prevalence of chronic wounds, the growing number of surgical procedures, and advancements in medical technology are key factors driving this market expansion. As healthcare providers and patients continue to seek reliable and effective solutions for wound care, the Global Medical Adhesive Plaster Market is expected to experience sustained growth, contributing to the overall development of the medical devices industry.

| Report Metric | Details |

| Report Name | Medical Adhesive Plaster Market |

| Accounted market size in 2023 | US$ 275 million |

| Forecasted market size in 2030 | US$ 369.5 million |

| CAGR | 4.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Smith and Nephew, Johnson and Johnson, 3M, Beiersdorf AG, Winner Medical, McKesson Corporation, B. Braun, Hartmann, Sterimed, BOENMED, Unimax Medical, Forlong Medical, AdvaCare Pharma, Haishi Hainuo Group, Zhuhai Runan, Wuhan Huawei Technology Co., Ltd., Shanghai Longlian Pharmaceutical Co., Ltd., Xinxiang Huaxi Sanitary Materials, Jianerkang Medical Co.,Ltd., Guangdong Hengjian Pharmaceutical Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |