What is Global Audio Streaming Platform and Service Market?

The Global Audio Streaming Platform and Service Market refers to the worldwide industry that provides digital audio content to users via the internet. This market encompasses a variety of services and platforms that allow users to stream music, podcasts, audiobooks, and other audio content on-demand. These platforms typically operate on a subscription-based model, offering both free and premium tiers. The free tier usually includes advertisements, while the premium tier offers an ad-free experience along with additional features such as offline listening and higher audio quality. The market has seen significant growth due to the increasing adoption of smartphones, high-speed internet, and the growing popularity of digital content consumption. Major players in this market include Spotify, Apple Music, Amazon Music, and Google Play Music, among others. These platforms not only provide a vast library of audio content but also offer personalized recommendations based on user preferences, enhancing the overall user experience. The market is also characterized by continuous technological advancements, such as the integration of artificial intelligence and machine learning to improve content discovery and user engagement.

Hardware, Software, Platform and Service in the Global Audio Streaming Platform and Service Market:

The Global Audio Streaming Platform and Service Market can be dissected into four main components: hardware, software, platform, and service. Hardware refers to the physical devices used to access audio streaming services, such as smartphones, tablets, smart speakers, and computers. These devices are essential for users to connect to the internet and stream audio content. The proliferation of affordable and high-quality hardware has significantly contributed to the growth of the audio streaming market. Software, on the other hand, includes the applications and operating systems that facilitate audio streaming. This encompasses mobile apps, desktop applications, and web-based platforms that provide a user-friendly interface for accessing and managing audio content. Software development in this market focuses on enhancing user experience through features like personalized playlists, social sharing, and seamless integration with other digital services. The platform component refers to the underlying infrastructure that supports audio streaming services. This includes cloud-based servers, content delivery networks (CDNs), and data analytics tools that ensure smooth and efficient streaming. Platforms are designed to handle large volumes of data and provide real-time analytics to optimize content delivery and user engagement. Finally, the service component encompasses the actual audio content and the business models that support it. This includes subscription plans, advertising models, and partnerships with content creators and record labels. Services are tailored to meet the diverse needs of users, offering a wide range of audio content from various genres and languages. The integration of advanced technologies like artificial intelligence and machine learning has further enhanced the service component by providing personalized recommendations and improving content discovery. Overall, the synergy between hardware, software, platform, and service is crucial for the success of the Global Audio Streaming Platform and Service Market.

Enterprise, Radio, Music Concerts & Events, Personal, Others in the Global Audio Streaming Platform and Service Market:

The Global Audio Streaming Platform and Service Market finds extensive usage across various sectors, including enterprises, radio, music concerts and events, personal use, and others. In the enterprise sector, audio streaming services are increasingly being used for corporate communications, training sessions, and webinars. Companies leverage these platforms to disseminate information efficiently and engage with employees and stakeholders. The ability to stream live audio and record sessions for later playback adds a layer of flexibility and convenience. In the radio sector, traditional radio stations are adopting audio streaming to reach a broader audience. Online radio streaming allows stations to broadcast their content globally, breaking geographical barriers. This has led to the resurgence of radio as a popular medium for news, music, and talk shows. Music concerts and events have also embraced audio streaming to enhance the audience experience. Live streaming of concerts allows fans who cannot attend in person to enjoy the performance from the comfort of their homes. This has opened up new revenue streams for artists and event organizers. For personal use, audio streaming platforms offer a convenient way for individuals to access a vast library of music, podcasts, and audiobooks. Users can create personalized playlists, discover new content, and enjoy high-quality audio on-demand. The integration of social features also allows users to share their favorite tracks and playlists with friends and family. Other areas where audio streaming is making an impact include education and healthcare. In education, audio streaming is used for delivering lectures, language learning, and providing access to educational podcasts. In healthcare, it is used for telemedicine consultations and delivering health-related information to patients. The versatility and convenience of audio streaming make it a valuable tool across various sectors, enhancing communication, entertainment, and information dissemination.

Global Audio Streaming Platform and Service Market Outlook:

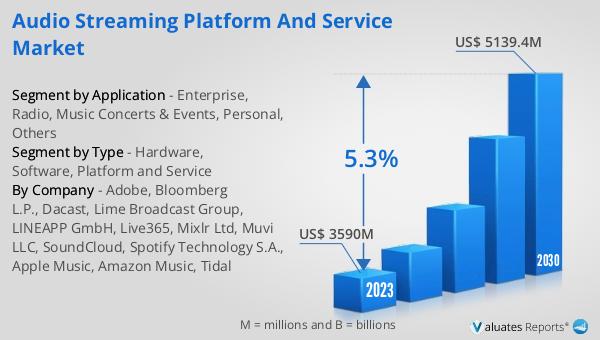

The global Audio Streaming Platform and Service market was valued at US$ 3,590 million in 2023 and is anticipated to reach US$ 5,139.4 million by 2030, witnessing a CAGR of 5.3% during the forecast period from 2024 to 2030. This growth trajectory highlights the increasing demand for audio streaming services worldwide. The market's expansion can be attributed to several factors, including the rising adoption of smartphones and high-speed internet, which make it easier for users to access audio content on-the-go. Additionally, the growing popularity of digital content consumption, driven by the convenience and variety offered by audio streaming platforms, is fueling market growth. The integration of advanced technologies such as artificial intelligence and machine learning is also playing a crucial role in enhancing user experience and engagement. These technologies enable personalized recommendations, improving content discovery and retention. Furthermore, the shift towards subscription-based models, offering both free and premium tiers, is attracting a diverse user base. The free tier, supported by advertisements, provides an entry point for new users, while the premium tier offers an ad-free experience with additional features, catering to more discerning users. The market is also benefiting from strategic partnerships and collaborations between audio streaming platforms and content creators, record labels, and other stakeholders. These partnerships ensure a steady supply of high-quality audio content, further driving user engagement and retention. Overall, the global Audio Streaming Platform and Service market is poised for significant growth, driven by technological advancements, changing consumer preferences, and strategic industry collaborations.

| Report Metric | Details |

| Report Name | Audio Streaming Platform and Service Market |

| Accounted market size in 2023 | US$ 3590 million |

| Forecasted market size in 2030 | US$ 5139.4 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Adobe, Bloomberg L.P., Dacast, Lime Broadcast Group, LINEAPP GmbH, Live365, Mixlr Ltd, Muvi LLC, SoundCloud, Spotify Technology S.A., Apple Music, Amazon Music, Tidal |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |