What is Global Rack Mounted Video Encoders Market?

The Global Rack Mounted Video Encoders Market refers to the industry focused on the production and distribution of video encoders that are designed to be mounted on racks. These devices are essential for converting analog video signals into digital formats, which can then be transmitted over various networks. Rack-mounted video encoders are widely used in professional broadcasting, security surveillance, and other applications where high-quality video transmission is crucial. They offer the advantage of being able to handle multiple video channels simultaneously, making them ideal for large-scale operations. The market for these devices is driven by the increasing demand for high-definition video content, advancements in video compression technologies, and the growing need for efficient video transmission solutions in various industries. As more organizations adopt digital video solutions, the demand for reliable and high-performance video encoders continues to rise, making this market a significant segment within the broader video technology industry.

1 Channel, 2 Channel, 4 Channel, 8 Channel, 16 Channel, More Than 16 Channel in the Global Rack Mounted Video Encoders Market:

In the Global Rack Mounted Video Encoders Market, the devices are categorized based on the number of channels they can handle. A 1 Channel video encoder is designed to convert a single analog video signal into a digital format. This type of encoder is typically used in smaller setups where only one video source needs to be digitized and transmitted. It is ideal for applications such as single-camera security systems or individual broadcasting setups. A 2 Channel video encoder, on the other hand, can handle two video signals simultaneously. This makes it suitable for slightly larger operations, such as small-scale surveillance systems or dual-camera broadcasting setups. Moving up, a 4 Channel video encoder can manage four video signals at once, making it a good fit for medium-sized security systems or multi-camera broadcasting environments. An 8 Channel video encoder can handle eight video signals simultaneously, which is ideal for larger surveillance systems or more complex broadcasting setups that require multiple camera angles. A 16 Channel video encoder can manage sixteen video signals at once, making it suitable for very large-scale operations such as extensive security surveillance systems in large facilities or comprehensive broadcasting setups. Finally, video encoders that can handle more than 16 channels are designed for the most demanding applications. These high-capacity encoders are used in large-scale security systems, major broadcasting networks, and other environments where a significant number of video sources need to be digitized and transmitted simultaneously. Each type of encoder offers different levels of performance, scalability, and functionality, catering to the diverse needs of various industries and applications.

Webcast, Live TV, Monitor, Other in the Global Rack Mounted Video Encoders Market:

The Global Rack Mounted Video Encoders Market finds extensive usage in several key areas, including webcasting, live TV, monitoring, and other applications. In webcasting, these video encoders play a crucial role in converting live video feeds into digital formats that can be streamed over the internet. This is essential for events such as webinars, online conferences, and live performances, where high-quality video streaming is required to reach a global audience. The ability to handle multiple video channels simultaneously makes rack-mounted video encoders ideal for complex webcasting setups that involve multiple camera angles and video sources. In the realm of live TV, these encoders are indispensable for broadcasting live events such as sports, news, and entertainment shows. They ensure that the video signals are converted into digital formats that can be transmitted over various networks, providing viewers with high-definition, real-time content. The reliability and performance of rack-mounted video encoders make them a preferred choice for professional broadcasters who need to deliver seamless live TV experiences. For monitoring purposes, these video encoders are widely used in security surveillance systems. They convert analog video feeds from security cameras into digital formats that can be transmitted over IP networks, allowing for real-time monitoring and recording. This is particularly important in large facilities such as airports, shopping malls, and corporate campuses, where multiple video feeds need to be managed simultaneously. Other applications of rack-mounted video encoders include medical imaging, where they are used to transmit high-definition video feeds from medical equipment to remote locations for diagnosis and consultation. They are also used in industrial automation, where video feeds from production lines are monitored to ensure quality control and operational efficiency. Overall, the versatility and high performance of rack-mounted video encoders make them essential tools in a wide range of industries and applications.

Global Rack Mounted Video Encoders Market Outlook:

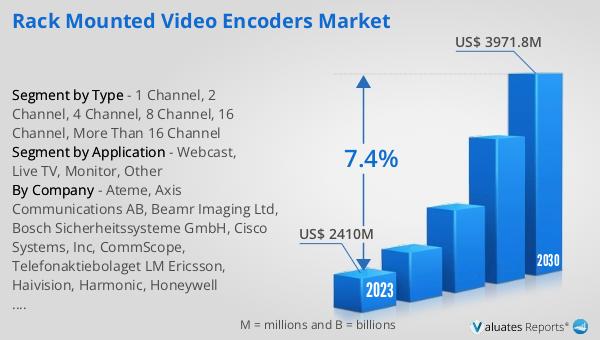

The global Rack Mounted Video Encoders market was valued at US$ 2410 million in 2023 and is anticipated to reach US$ 3971.8 million by 2030, witnessing a CAGR of 7.4% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for high-quality video transmission solutions across various industries. As organizations continue to adopt digital video technologies, the need for reliable and efficient video encoders is expected to rise. The market's expansion is driven by advancements in video compression technologies, the growing popularity of high-definition video content, and the increasing use of video encoders in applications such as broadcasting, security surveillance, and webcasting. The ability of rack-mounted video encoders to handle multiple video channels simultaneously makes them ideal for large-scale operations, further fueling their demand. As a result, the global Rack Mounted Video Encoders market is poised for substantial growth in the coming years, offering numerous opportunities for manufacturers and stakeholders in the industry.

| Report Metric | Details |

| Report Name | Rack Mounted Video Encoders Market |

| Accounted market size in 2023 | US$ 2410 million |

| Forecasted market size in 2030 | US$ 3971.8 million |

| CAGR | 7.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ateme, Axis Communications AB, Beamr Imaging Ltd, Bosch Sicherheitssysteme GmbH, Cisco Systems, Inc, CommScope, Telefonaktiebolaget LM Ericsson, Haivision, Harmonic, Honeywell International Inc, Matrox, Motorola Solutions, Inc, TRUEN, Milestone Systems A/S, Cdtech Innovations Private Limited, Delta Information Systems, Inc, ACTi Corporation, Dahua Technology USA Inc, HaiweiTech, Hangzhou Hikvision Digital Technology Co., Ltd, Merit LILIN Ent. Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |