What is Global Jet Self-priming Pump Market?

The Global Jet Self-priming Pump Market refers to the worldwide industry focused on the production, distribution, and utilization of jet self-priming pumps. These pumps are designed to automatically remove air from the pump and suction line, allowing them to start and operate without manual priming. This feature makes them highly efficient and convenient for various applications. The market encompasses a wide range of products, including different types of jet self-priming pumps such as diesel and electric variants. It serves multiple industries, including agriculture, construction, municipal wastewater treatment, and more. The market's growth is driven by the increasing demand for efficient water management solutions and the need for reliable pumping systems in various sectors. Technological advancements and innovations in pump design also contribute to the market's expansion, offering improved performance and energy efficiency. The global reach of this market highlights its significance in addressing water-related challenges and supporting various industrial and agricultural activities worldwide.

Diesel Jet Self-Priming Pump, Electric Jet Self-priming Pump in the Global Jet Self-priming Pump Market:

Diesel Jet Self-Priming Pumps and Electric Jet Self-Priming Pumps are two primary types of jet self-priming pumps available in the global market. Diesel jet self-priming pumps are powered by diesel engines, making them suitable for applications where electricity is not readily available. These pumps are highly durable and can handle heavy-duty tasks, making them ideal for use in remote locations, construction sites, and agricultural fields. They are known for their robustness and ability to operate under harsh conditions, providing reliable performance even in challenging environments. On the other hand, electric jet self-priming pumps are powered by electric motors, offering a more environmentally friendly and energy-efficient option. These pumps are commonly used in urban and industrial settings where a stable power supply is available. Electric jet self-priming pumps are known for their quiet operation, ease of maintenance, and lower operational costs compared to diesel-powered pumps. They are widely used in residential areas, commercial buildings, and municipal facilities for water supply and wastewater management. Both types of pumps play a crucial role in the global jet self-priming pump market, catering to diverse needs and applications across different sectors. The choice between diesel and electric pumps depends on factors such as the availability of power sources, the specific requirements of the application, and environmental considerations. As the demand for efficient and reliable pumping solutions continues to grow, both diesel and electric jet self-priming pumps are expected to see increased adoption in various industries.

Industry, Construction Industry, Municipal Wastewater Treatment, Agriculture, Others in the Global Jet Self-priming Pump Market:

The usage of Global Jet Self-priming Pump Market spans across several key areas, including industry, construction, municipal wastewater treatment, agriculture, and others. In the industrial sector, jet self-priming pumps are essential for processes that require the transfer of liquids, such as in chemical manufacturing, food and beverage production, and pharmaceuticals. These pumps ensure efficient and continuous operation, minimizing downtime and enhancing productivity. In the construction industry, jet self-priming pumps are used for dewatering sites, supplying water for construction activities, and managing wastewater. Their ability to handle solids and debris makes them ideal for construction environments where water management is critical. Municipal wastewater treatment facilities rely on jet self-priming pumps for the efficient handling and treatment of sewage and wastewater. These pumps help in maintaining the flow of wastewater through various treatment stages, ensuring the effective removal of contaminants and pollutants. In agriculture, jet self-priming pumps are used for irrigation, water supply, and drainage. They provide a reliable solution for farmers to manage water resources efficiently, supporting crop growth and livestock needs. Other applications of jet self-priming pumps include firefighting, marine operations, and emergency water supply. Their versatility and reliability make them a valuable asset in various scenarios where efficient water management is required. The global jet self-priming pump market's ability to cater to such a wide range of applications underscores its importance in supporting essential activities across different sectors.

Global Jet Self-priming Pump Market Outlook:

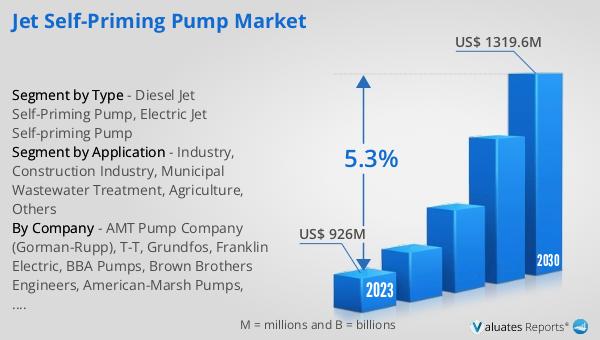

The global Jet Self-priming Pump market was valued at US$ 926 million in 2023 and is anticipated to reach US$ 1319.6 million by 2030, witnessing a CAGR of 5.3% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the jet self-priming pump market over the coming years. The projected increase in market value reflects the rising demand for efficient and reliable pumping solutions across various industries. The compound annual growth rate (CAGR) of 5.3% indicates a steady and robust expansion, driven by factors such as technological advancements, increasing industrialization, and the need for effective water management systems. The market's growth trajectory underscores the importance of jet self-priming pumps in addressing water-related challenges and supporting diverse applications. As industries and municipalities continue to seek innovative solutions for water supply, wastewater treatment, and other critical functions, the demand for jet self-priming pumps is expected to rise. This positive market outlook suggests a promising future for manufacturers, suppliers, and stakeholders in the global jet self-priming pump market.

| Report Metric | Details |

| Report Name | Jet Self-priming Pump Market |

| Accounted market size in 2023 | US$ 926 million |

| Forecasted market size in 2030 | US$ 1319.6 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | AMT Pump Company (Gorman-Rupp), T-T, Grundfos, Franklin Electric, BBA Pumps, Brown Brothers Engineers, American-Marsh Pumps, Calpeda, CRI, Pentax Water Pumps, Shimge Pump, Dayuan Pumps Industry, Haicheng Sanyu Pump Industry, Dynasty Pumps, Guangdong Winning Pumps Industrial, Shanghai Shuangbao Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |