What is Global Gynecological Surgery Adhesion Barrier Market?

The Global Gynecological Surgery Adhesion Barrier Market refers to the market for medical products designed to prevent adhesions, which are bands of scar tissue that can form after gynecological surgeries. Adhesions can cause significant complications, including chronic pain, infertility, and bowel obstruction. Adhesion barriers are used during surgeries to reduce the risk of these complications by creating a physical barrier between tissues and organs. These barriers come in various forms, such as liquids, films, and gels, and are applied directly to the surgical site. The market for these products is driven by the increasing number of gynecological surgeries, advancements in medical technology, and growing awareness about the complications associated with adhesions. The market is also influenced by regulatory approvals and the availability of different types of adhesion barriers that cater to specific surgical needs.

Liquid Formulation, Film Formulation, Gel Formulation in the Global Gynecological Surgery Adhesion Barrier Market:

In the Global Gynecological Surgery Adhesion Barrier Market, there are three main types of formulations: liquid, film, and gel. Liquid formulations are typically easy to apply and can cover large or irregular surfaces effectively. They are often used in laparoscopic surgeries where precision and ease of application are crucial. Liquid barriers can be sprayed or poured onto the surgical site, forming a thin layer that prevents tissues from sticking together during the healing process. Film formulations, on the other hand, are thin, flexible sheets that can be cut to size and placed directly over the surgical area. These films are particularly useful in open surgeries where a more controlled and localized application is needed. They provide a physical barrier that remains in place until the tissues have healed sufficiently to prevent adhesion formation. Gel formulations are another popular option, offering a combination of ease of application and effective coverage. Gels can be spread over the surgical site and conform to the shape of the tissues, providing a consistent barrier that reduces the risk of adhesions. Each of these formulations has its own advantages and is chosen based on the specific requirements of the surgery and the surgeon's preference. The choice of formulation can also be influenced by factors such as the type of surgery, the patient's condition, and the surgeon's experience with the product.

Uterine Use, Pelvic Use, Others in the Global Gynecological Surgery Adhesion Barrier Market:

The usage of Global Gynecological Surgery Adhesion Barriers can be categorized into three main areas: uterine use, pelvic use, and others. Uterine use involves the application of adhesion barriers during surgeries that involve the uterus, such as myomectomy, hysterectomy, and cesarean sections. These barriers help prevent adhesions that can lead to complications like chronic pelvic pain and infertility. In pelvic use, adhesion barriers are applied during surgeries involving the pelvic organs, such as the ovaries, fallopian tubes, and bladder. These surgeries can include procedures for endometriosis, pelvic inflammatory disease, and ovarian cysts. The barriers help reduce the risk of adhesions that can cause pain and dysfunction in the pelvic region. The "others" category includes the use of adhesion barriers in surgeries that do not specifically involve the uterus or pelvic organs but still require the prevention of adhesions. This can include abdominal surgeries, bowel resections, and other procedures where adhesions can cause significant complications. In all these areas, the use of adhesion barriers is crucial for improving surgical outcomes and reducing the risk of long-term complications.

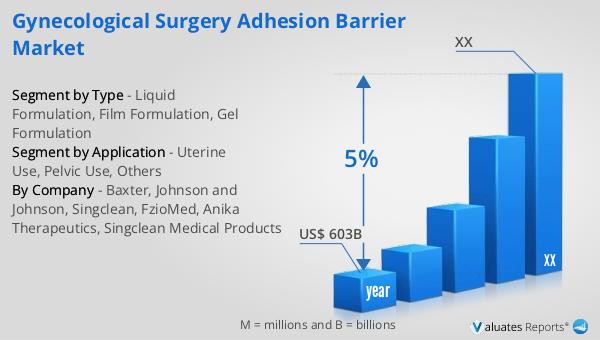

Global Gynecological Surgery Adhesion Barrier Market Outlook:

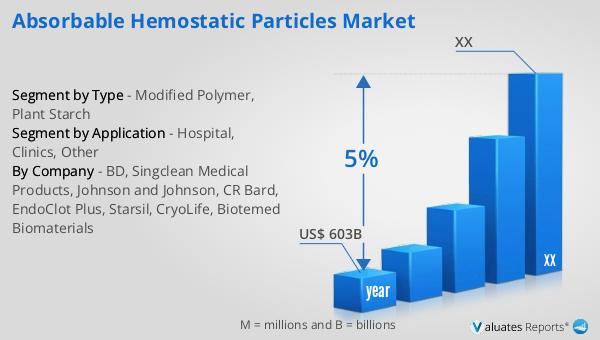

Based on our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing healthcare expenditures, and the rising prevalence of chronic diseases that require medical interventions. The market encompasses a wide range of devices, from diagnostic equipment to therapeutic and surgical instruments, catering to various medical needs. The continuous innovation in medical devices, coupled with the growing demand for minimally invasive procedures, is expected to fuel the market's expansion. Additionally, the aging population and the increasing focus on improving healthcare infrastructure in emerging economies are contributing to the market's growth. As healthcare providers and patients seek more efficient and effective treatment options, the demand for advanced medical devices is likely to rise, further propelling the market's development.

| Report Metric | Details |

| Report Name | Gynecological Surgery Adhesion Barrier Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Baxter, Johnson and Johnson, Singclean, FzioMed, Anika Therapeutics, Singclean Medical Products |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |