What is Global Automobile EVP (Electric Vacuum Pump) Market?

The Global Automobile EVP (Electric Vacuum Pump) Market is a rapidly evolving sector within the automotive industry. Electric Vacuum Pumps (EVPs) are essential components in modern vehicles, particularly in electric and hybrid models, where they replace traditional mechanical pumps. These pumps are crucial for maintaining the vacuum required for various vehicle functions, such as brake boosters, which enhance braking performance and safety. The market for EVPs is driven by the increasing adoption of electric and hybrid vehicles, stringent emission regulations, and the need for fuel efficiency. As the automotive industry shifts towards more sustainable and efficient technologies, the demand for EVPs is expected to grow significantly. This market encompasses a range of products and technologies designed to meet the diverse needs of different vehicle types and manufacturers, making it a dynamic and competitive landscape.

Diaphragm Type, Leaf Type, Swing Pistol Type in the Global Automobile EVP (Electric Vacuum Pump) Market:

In the Global Automobile EVP (Electric Vacuum Pump) Market, there are several types of pumps, including Diaphragm Type, Leaf Type, and Swing Piston Type, each with its unique characteristics and applications. Diaphragm Type EVPs are known for their reliability and efficiency. They use a flexible diaphragm to create a vacuum, which is ideal for applications requiring a steady and consistent vacuum supply. These pumps are often used in electric and hybrid vehicles due to their ability to operate quietly and efficiently, which is crucial for maintaining the overall performance and comfort of the vehicle. Leaf Type EVPs, on the other hand, use a series of flexible leaves or vanes to generate a vacuum. This design allows for a compact and lightweight pump, making it suitable for vehicles where space and weight are critical considerations. Leaf Type pumps are also known for their durability and low maintenance requirements, making them a popular choice among manufacturers. Swing Piston Type EVPs utilize a piston that swings back and forth to create a vacuum. This type of pump is highly efficient and capable of generating a strong vacuum, making it ideal for applications that require a high level of vacuum performance. Swing Piston pumps are often used in conventional cars, where they can provide the necessary vacuum for brake boosters and other systems. Each of these pump types offers distinct advantages, and the choice of pump depends on the specific requirements of the vehicle and the manufacturer. As the demand for electric and hybrid vehicles continues to grow, the market for EVPs is expected to expand, with manufacturers developing new and innovative pump designs to meet the evolving needs of the automotive industry.

Electric Automobile, Hebric Electric Vehicle, Conventional car in the Global Automobile EVP (Electric Vacuum Pump) Market:

The usage of Global Automobile EVP (Electric Vacuum Pump) Market in Electric Automobiles, Hybrid Electric Vehicles, and Conventional Cars varies based on the specific requirements and design of each vehicle type. In Electric Automobiles, EVPs play a crucial role in maintaining the vacuum needed for brake boosters and other systems, as these vehicles do not have a traditional internal combustion engine to generate a vacuum. The use of EVPs in electric vehicles ensures that the braking system operates efficiently and safely, providing the necessary braking force when needed. Additionally, EVPs help improve the overall efficiency of electric vehicles by reducing the load on the battery and enhancing the vehicle's range. In Hybrid Electric Vehicles, EVPs are used to supplement the vacuum generated by the internal combustion engine. Hybrid vehicles often switch between electric and gasoline power, and during electric mode, the engine is not running, which means there is no vacuum available for the brake booster. EVPs ensure that the braking system remains functional and responsive, regardless of the power source being used. This is particularly important for maintaining the safety and performance of hybrid vehicles, which rely on a seamless transition between power sources. In Conventional Cars, EVPs are used to enhance the performance of the braking system and other vacuum-dependent systems. While traditional internal combustion engines can generate a vacuum, the use of EVPs can provide a more consistent and reliable vacuum supply, improving the overall performance and efficiency of the vehicle. EVPs can also help reduce emissions and improve fuel efficiency by optimizing the operation of the engine and other systems. Overall, the use of EVPs in electric, hybrid, and conventional vehicles highlights the importance of these components in modern automotive design, as they contribute to the safety, efficiency, and performance of the vehicle.

Global Automobile EVP (Electric Vacuum Pump) Market Outlook:

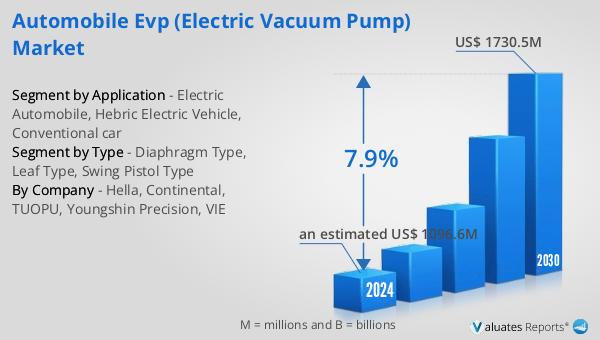

The global Automobile EVP Electric Vacuum Pump market is anticipated to grow significantly, with projections estimating it will reach US$ 1730.5 million by 2030, up from an estimated US$ 1096.6 million in 2024, reflecting a compound annual growth rate (CAGR) of 7.9% during the period from 2024 to 2030. Hella stands out as the largest producer in this market, holding a substantial market share of approximately 35.92% as of 2019. Following Hella, Continental is another major player, with a market share of 18.7%. These companies are leading the way in the development and production of EVPs, driven by the increasing demand for electric and hybrid vehicles, as well as the need for more efficient and environmentally friendly automotive technologies. The market's growth is also supported by stringent emission regulations and the push for greater fuel efficiency, which are encouraging manufacturers to adopt advanced vacuum pump technologies. As the automotive industry continues to evolve, the role of EVPs in enhancing vehicle performance, safety, and efficiency will become increasingly important, driving further innovation and growth in this dynamic market.

| Report Metric | Details |

| Report Name | Automobile EVP (Electric Vacuum Pump) Market |

| Accounted market size in 2024 | an estimated US$ 1096.6 million |

| Forecasted market size in 2030 | US$ 1730.5 million |

| CAGR | 7.9% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hella, Continental, TUOPU, Youngshin Precision, VIE |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |