What is Global PUF Panel Market?

The Global PUF Panel Market refers to the worldwide industry involved in the production, distribution, and application of Polyurethane Foam (PUF) panels. These panels are widely used in various sectors due to their excellent thermal insulation properties, lightweight nature, and structural strength. PUF panels are made by injecting a liquid mixture of polyol and isocyanate into a mold, where it reacts and expands to form a rigid foam core. This core is then sandwiched between two layers of protective material, such as metal or plastic, to create a durable and efficient insulation panel. The global market for PUF panels is driven by the increasing demand for energy-efficient building materials, the need for temperature-controlled environments in industries like food storage and pharmaceuticals, and the growing trend of prefabricated construction. These panels are also favored for their quick installation, cost-effectiveness, and versatility in various applications, ranging from industrial warehouses to commercial buildings and residential homes. As the world continues to prioritize sustainability and energy conservation, the demand for PUF panels is expected to grow, making it a significant segment in the construction and insulation industry.

Thickness below 51 mm, Thickness 51 mm-100 mm, Thickness above 100 mm in the Global PUF Panel Market:

In the Global PUF Panel Market, the thickness of the panels plays a crucial role in determining their application and effectiveness. Panels with a thickness below 51 mm are typically used in applications where space is a constraint, and moderate insulation is required. These thinner panels are ideal for interior partitions, ceilings, and areas where the primary focus is not on extreme thermal insulation but rather on providing a lightweight and easy-to-install solution. They are commonly used in residential buildings, office spaces, and temporary structures where quick assembly and disassembly are necessary. On the other hand, panels with a thickness ranging from 51 mm to 100 mm offer a higher level of insulation and are suitable for more demanding applications. These panels are often used in commercial buildings, cold storage facilities, and industrial warehouses where maintaining a consistent temperature is crucial. The increased thickness provides better thermal resistance, making them ideal for environments that require energy efficiency and temperature control. Additionally, these panels are also used in the construction of prefabricated buildings and modular homes, where their structural strength and insulation properties are highly valued. Panels with a thickness above 100 mm are designed for the most demanding insulation requirements. These thick panels are used in specialized applications such as refrigerated trucks, walk-in freezers, and large cold storage warehouses. The superior insulation provided by these panels ensures that the internal temperature remains stable, even in extreme external conditions. They are also used in industrial applications where high thermal resistance is necessary, such as in chemical plants and power generation facilities. The increased thickness not only provides excellent insulation but also adds to the structural integrity of the building, making them suitable for heavy-duty applications. In summary, the thickness of PUF panels in the global market varies to cater to different insulation needs and applications. Thinner panels below 51 mm are used for lightweight and less demanding applications, while panels with a thickness of 51 mm to 100 mm are suitable for commercial and industrial uses that require better insulation. Panels above 100 mm are reserved for specialized applications that demand the highest level of thermal resistance and structural strength. The versatility in thickness options allows PUF panels to be used in a wide range of industries, making them a valuable component in modern construction and insulation solutions.

Industry, Commercial, Others in the Global PUF Panel Market:

The usage of PUF panels in the Global PUF Panel Market spans across various sectors, including industry, commercial, and others. In the industrial sector, PUF panels are extensively used for their superior insulation properties and structural strength. They are commonly employed in the construction of cold storage facilities, warehouses, and manufacturing plants where maintaining a controlled temperature is essential. The panels help in reducing energy consumption by providing excellent thermal insulation, thereby ensuring that the internal environment remains stable. Additionally, PUF panels are used in the construction of clean rooms and laboratories where temperature and humidity control are critical. Their lightweight nature and ease of installation make them a preferred choice for industrial applications that require quick and efficient construction solutions. In the commercial sector, PUF panels are widely used in the construction of office buildings, shopping malls, and hotels. The panels provide an energy-efficient solution for maintaining comfortable indoor temperatures, reducing the need for extensive heating and cooling systems. They are also used in the construction of prefabricated buildings and modular structures, which are becoming increasingly popular due to their cost-effectiveness and quick assembly. PUF panels offer a versatile solution for commercial buildings, providing both insulation and structural support. The panels are also used in the construction of temporary structures, such as exhibition halls and event spaces, where quick installation and disassembly are required. In addition to industrial and commercial applications, PUF panels are also used in various other sectors. In the residential sector, they are used in the construction of energy-efficient homes, providing excellent insulation and reducing energy consumption. The panels are also used in the construction of agricultural buildings, such as barns and poultry houses, where maintaining a controlled environment is essential for the health and productivity of livestock. Furthermore, PUF panels are used in the transportation sector, particularly in the construction of refrigerated trucks and containers that require superior insulation to maintain the temperature of perishable goods. The versatility of PUF panels makes them a valuable component in a wide range of applications, providing energy-efficient and cost-effective solutions for various industries. In summary, the usage of PUF panels in the Global PUF Panel Market extends across multiple sectors, including industry, commercial, and others. In the industrial sector, they are used for cold storage facilities, warehouses, and clean rooms, providing excellent thermal insulation and structural strength. In the commercial sector, they are used in office buildings, shopping malls, and prefabricated structures, offering energy-efficient and versatile solutions. Additionally, PUF panels are used in the residential, agricultural, and transportation sectors, providing valuable insulation and structural support. The wide range of applications highlights the importance of PUF panels in modern construction and insulation solutions.

Global PUF Panel Market Outlook:

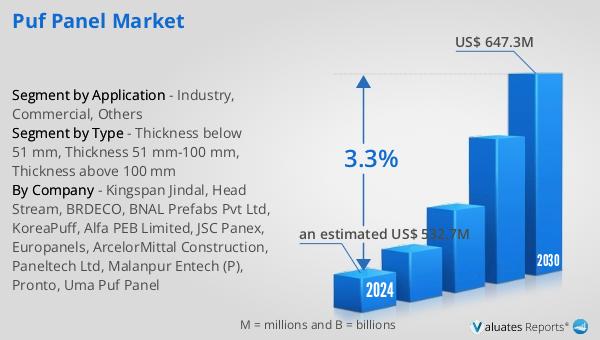

The global PUF Panel market is anticipated to grow significantly, with projections indicating it will reach US$ 647.3 million by 2030, up from an estimated US$ 532.7 million in 2024, reflecting a compound annual growth rate (CAGR) of 3.3% during the period from 2024 to 2030. This growth is driven by the increasing demand for energy-efficient building materials and the need for temperature-controlled environments in various industries. Among the regions, India stands out with the highest market share, accounting for more than 50% of the total consumption. This dominance can be attributed to the rapid industrialization and urbanization in the country, which has led to a surge in demand for PUF panels in construction and industrial applications. The growing awareness about energy conservation and the benefits of using PUF panels for insulation purposes has further fueled the market growth in India. The regional division highlights the significant role that India plays in the global PUF Panel market, making it a key player in the industry. The market outlook indicates a positive trend, with steady growth expected over the forecast period, driven by the increasing adoption of PUF panels in various sectors and the continuous advancements in panel technology.

| Report Metric | Details |

| Report Name | PUF Panel Market |

| Accounted market size in 2024 | an estimated US$ 532.7 million |

| Forecasted market size in 2030 | US$ 647.3 million |

| CAGR | 3.3% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kingspan Jindal, Head Stream, BRDECO, BNAL Prefabs Pvt Ltd, KoreaPuff, Alfa PEB Limited, JSC Panex, Europanels, ArcelorMittal Construction, Paneltech Ltd, Malanpur Entech (P), Pronto, Uma Puf Panel |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |