What is Global Ferrocene Market?

The global ferrocene market is a specialized segment within the broader chemical industry, focusing on the production and distribution of ferrocene, a compound consisting of two cyclopentadienyl anions bound to a central iron atom. This organometallic compound is known for its stability and unique chemical properties, making it valuable in various industrial applications. Ferrocene is primarily used as a fuel additive, in chemical synthesis, and in the pharmaceutical industry. Its ability to improve fuel efficiency and reduce emissions has made it a popular choice in the automotive and aerospace sectors. Additionally, ferrocene's role as a catalyst and its potential therapeutic properties have spurred interest in its use in medicine and other scientific research areas. The market for ferrocene is driven by its diverse applications and the growing demand for high-performance materials in various industries. As a result, the global ferrocene market is expected to continue its growth trajectory, supported by advancements in technology and increasing awareness of its benefits.

Purity ≥ 98%, Purity ≥ 99%, Purity ≥ 99.5% in the Global Ferrocene Market:

In the global ferrocene market, the purity levels of the product play a crucial role in determining its suitability for different applications. Purity levels such as ≥ 98%, ≥ 99%, and ≥ 99.5% are commonly used to classify ferrocene products. Ferrocene with a purity of ≥ 98% is typically used in applications where high purity is not critical, such as in certain fuel additives and industrial processes. This level of purity ensures that the ferrocene performs its intended function without significantly impacting the overall quality of the end product. On the other hand, ferrocene with a purity of ≥ 99% is preferred for more demanding applications, such as in chemical synthesis and pharmaceuticals, where higher purity is essential to achieve the desired chemical reactions and ensure the safety and efficacy of the final product. The highest purity level, ≥ 99.5%, is reserved for the most stringent applications, including advanced research and high-precision manufacturing processes. This level of purity guarantees the highest performance and minimal impurities, making it ideal for use in cutting-edge technologies and critical applications. The demand for high-purity ferrocene is driven by the need for reliable and consistent performance in various industries, and manufacturers are continually striving to improve their production processes to meet these stringent requirements. As the global ferrocene market continues to evolve, the importance of purity levels will remain a key factor in determining the suitability and effectiveness of ferrocene products for different applications.

Fuel Additive, Chemical Synthesis, Medicine, Others in the Global Ferrocene Market:

The global ferrocene market finds its usage in several key areas, including fuel additives, chemical synthesis, medicine, and other specialized applications. As a fuel additive, ferrocene is highly valued for its ability to enhance fuel efficiency and reduce emissions. By improving the combustion process, ferrocene helps in achieving better fuel economy and lower levels of harmful pollutants, making it an attractive option for the automotive and aerospace industries. In chemical synthesis, ferrocene serves as a versatile catalyst and reagent, facilitating various chemical reactions and enabling the production of complex molecules. Its stability and reactivity make it an essential component in the synthesis of pharmaceuticals, agrochemicals, and other fine chemicals. In the field of medicine, ferrocene's unique properties have led to its exploration as a potential therapeutic agent. Researchers are investigating its use in drug delivery systems, cancer treatment, and other medical applications, driven by its ability to interact with biological molecules and its relatively low toxicity. Beyond these primary areas, ferrocene is also used in other specialized applications, such as in the production of polymers, coatings, and electronic materials. Its role in these diverse fields underscores the versatility and importance of ferrocene in modern industrial and scientific applications. As the demand for high-performance materials continues to grow, the global ferrocene market is expected to expand, driven by ongoing research and development efforts and the increasing recognition of its benefits across various sectors.

Global Ferrocene Market Outlook:

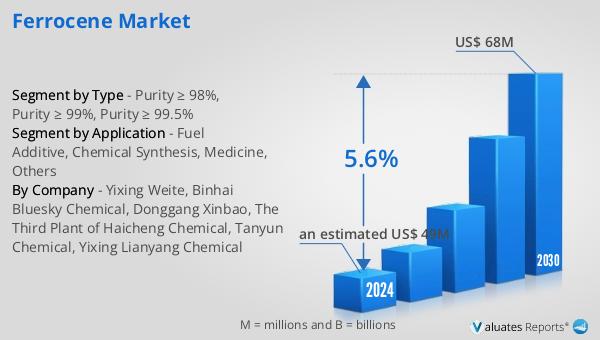

The global ferrocene market is anticipated to grow from an estimated US$ 49 million in 2024 to US$ 68 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.6% during this period. In 2019, the top three players in the market accounted for 78.31% of the global ferrocene CAS 102545 share and 77.52% of the global revenue share. China emerged as the world's largest production region for the ferrocene industry, contributing to 93.88% of the global ferrocene production share in 2019. This dominance is attributed to China's robust industrial infrastructure, extensive research and development capabilities, and the availability of raw materials. The concentration of production in China highlights the strategic importance of the region in the global ferrocene market. As the market continues to grow, the competitive landscape is expected to evolve, with key players focusing on innovation, quality improvement, and expanding their market presence to capitalize on the increasing demand for ferrocene across various applications.

| Report Metric | Details |

| Report Name | Ferrocene Market |

| Accounted market size in 2024 | an estimated US$ 49 million |

| Forecasted market size in 2030 | US$ 68 million |

| CAGR | 5.6% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Yixing Weite, Binhai Bluesky Chemical, Donggang Xinbao, The Third Plant of Haicheng Chemical, Tanyun Chemical, Yixing Lianyang Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |