What is Global Anisotropic Magnetoresistive (AMR) Sensors Market?

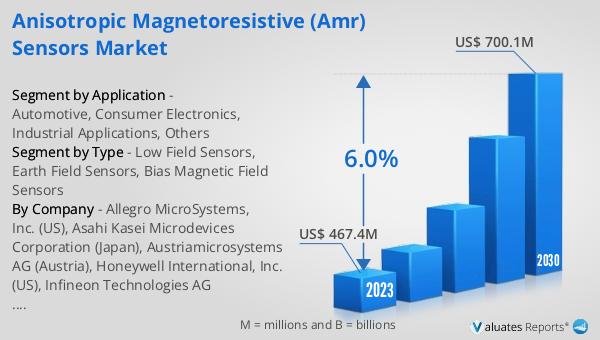

The global Anisotropic Magnetoresistive (AMR) Sensors market is a specialized segment within the broader sensor industry. AMR sensors are devices that detect changes in magnetic fields and convert them into electrical signals. These sensors are highly sensitive and can detect even minute changes in magnetic fields, making them ideal for various applications. The market for AMR sensors has been growing steadily due to their increasing adoption in multiple industries such as automotive, consumer electronics, and industrial applications. The sensors are known for their high accuracy, reliability, and low power consumption, which are critical factors driving their demand. The global market for AMR sensors was valued at US$ 467.4 million in 2023 and is expected to reach US$ 700.1 million by 2030, growing at a compound annual growth rate (CAGR) of 6.0% during the forecast period from 2024 to 2030. This growth is attributed to the rising need for advanced sensing technologies in various sectors, coupled with ongoing technological advancements in sensor technology.

Low Field Sensors, Earth Field Sensors, Bias Magnetic Field Sensors in the Global Anisotropic Magnetoresistive (AMR) Sensors Market:

Low Field Sensors, Earth Field Sensors, and Bias Magnetic Field Sensors are three primary types of AMR sensors that serve different purposes based on their sensitivity and application requirements. Low Field Sensors are designed to detect very weak magnetic fields, often in the range of microteslas. These sensors are particularly useful in applications where detecting small changes in magnetic fields is crucial, such as in medical devices for monitoring brain activity or in geological surveys for detecting mineral deposits. Earth Field Sensors, on the other hand, are calibrated to detect the Earth's magnetic field, which is relatively stronger compared to the fields detected by Low Field Sensors. These sensors are commonly used in navigation systems, including compasses and GPS devices, to provide accurate directional information. Bias Magnetic Field Sensors are designed to operate in environments where a constant magnetic field is present. These sensors are often used in industrial applications where machinery generates a consistent magnetic field, and the sensor's role is to detect any deviations from this constant field, which could indicate a malfunction or the presence of foreign objects. Each type of sensor has its unique advantages and is chosen based on the specific requirements of the application. For instance, Low Field Sensors are preferred in highly sensitive applications, while Earth Field Sensors are ideal for navigation and positioning systems. Bias Magnetic Field Sensors are commonly used in industrial settings where reliability and accuracy are paramount. The versatility of AMR sensors in detecting different ranges of magnetic fields makes them indispensable in various sectors, contributing to the overall growth of the global AMR sensors market.

Automotive, Consumer Electronics, Industrial Applications, Others in the Global Anisotropic Magnetoresistive (AMR) Sensors Market:

The usage of Global Anisotropic Magnetoresistive (AMR) Sensors spans across several key areas, including automotive, consumer electronics, industrial applications, and others. In the automotive sector, AMR sensors are extensively used for various functions such as position sensing, speed detection, and navigation. These sensors help in enhancing the safety and efficiency of vehicles by providing accurate data for systems like anti-lock braking systems (ABS), electronic stability control (ESC), and advanced driver-assistance systems (ADAS). In consumer electronics, AMR sensors are integrated into devices like smartphones, tablets, and wearable gadgets to enable features such as screen rotation, gaming controls, and navigation. The high sensitivity and low power consumption of these sensors make them ideal for portable electronic devices, where battery life and performance are critical. In industrial applications, AMR sensors are used for monitoring and controlling machinery, detecting the presence of magnetic materials, and ensuring the proper functioning of equipment. These sensors are crucial in automation and robotics, where precise position and speed measurements are necessary for efficient operation. Additionally, AMR sensors are employed in other areas such as healthcare, where they are used in medical devices for monitoring vital signs and in geophysical surveys for detecting mineral deposits. The versatility and reliability of AMR sensors make them suitable for a wide range of applications, driving their demand across various industries. The continuous advancements in sensor technology and the growing need for accurate and reliable sensing solutions are expected to further boost the adoption of AMR sensors in the coming years.

Global Anisotropic Magnetoresistive (AMR) Sensors Market Outlook:

The global Anisotropic Magnetoresistive (AMR) Sensors market was valued at US$ 467.4 million in 2023 and is anticipated to reach US$ 700.1 million by 2030, witnessing a CAGR of 6.0% during the forecast period 2024-2030. This indicates a steady growth trajectory for the market, driven by the increasing demand for advanced sensing technologies across various industries. The automotive sector, in particular, is expected to be a significant contributor to this growth, given the rising adoption of AMR sensors in modern vehicles for enhanced safety and efficiency. Similarly, the consumer electronics industry is likely to witness substantial growth in the use of AMR sensors, as these devices become more integral to the functionality of smartphones, tablets, and wearable gadgets. Industrial applications are also set to benefit from the advancements in AMR sensor technology, with these sensors playing a crucial role in automation, robotics, and machinery monitoring. The healthcare sector and geophysical surveys are other areas where the adoption of AMR sensors is expected to increase, further contributing to the market's growth. Overall, the global AMR sensors market is poised for significant expansion, driven by the continuous advancements in sensor technology and the growing need for accurate and reliable sensing solutions across various industries.

| Report Metric | Details |

| Report Name | Anisotropic Magnetoresistive (AMR) Sensors Market |

| Accounted market size in 2023 | US$ 467.4 million |

| Forecasted market size in 2030 | US$ 700.1 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Allegro MicroSystems, Inc. (US), Asahi Kasei Microdevices Corporation (Japan), Austriamicrosystems AG (Austria), Honeywell International, Inc. (US), Infineon Technologies AG (Germany), Melexis Microelectronic Systems (Belgium), MEMSIC, Inc. (US), Micronas Semiconductor Holding AG (Switzerland), NVE Corporation (US), NXP Semiconductors N.V. (The Netherlands), Sensitec GmbH (Germany) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |