What is Global High Temperature Smoke Extraction Motor Market?

The Global High Temperature Smoke Extraction Motor Market refers to the industry focused on the production and distribution of motors designed to operate in high-temperature environments, specifically for the purpose of extracting smoke. These motors are crucial in ensuring safety and compliance with fire safety regulations in various buildings and industrial settings. They are engineered to function effectively even under extreme heat conditions, which is essential during fire emergencies to clear smoke and toxic fumes, thereby aiding in safe evacuation and minimizing damage. The market encompasses a range of products tailored to different temperature classes and applications, ensuring that there is a suitable solution for various needs, from commercial buildings to industrial facilities. The demand for these motors is driven by stringent fire safety regulations, increasing awareness about safety measures, and the need for reliable smoke extraction systems in high-risk environments. As urbanization and industrialization continue to grow, the importance of these motors in safeguarding lives and property becomes even more pronounced.

200 °C Class, 250 °C Class, 300 °C Class, 400 °C Class in the Global High Temperature Smoke Extraction Motor Market:

In the Global High Temperature Smoke Extraction Motor Market, motors are categorized based on their ability to withstand specific temperature classes, namely 200 °C, 250 °C, 300 °C, and 400 °C. The 200 °C Class motors are designed for environments where the maximum temperature does not exceed 200 degrees Celsius. These are typically used in less severe fire scenarios or in areas where the likelihood of extreme heat is lower. They provide a cost-effective solution for smoke extraction in buildings with moderate fire safety requirements. The 250 °C Class motors are built to handle slightly higher temperatures, making them suitable for more demanding applications where the risk of higher heat levels is present. These motors are often found in commercial buildings and industrial settings where enhanced fire safety measures are necessary. The 300 °C Class motors are engineered for even more challenging environments, capable of operating efficiently at temperatures up to 300 degrees Celsius. These are essential in high-risk areas such as large industrial plants, warehouses, and facilities that store flammable materials. Finally, the 400 °C Class motors represent the highest level of heat resistance in this market. They are designed to function in the most extreme conditions, such as in tunnels, underground facilities, and other critical infrastructure where the potential for intense fires is significant. These motors ensure that smoke and toxic fumes can be effectively extracted even in the most severe fire emergencies, providing the highest level of safety and compliance with stringent fire safety regulations. Each class of motor is tailored to meet specific needs, ensuring that there is an appropriate solution for every application, from moderate to extreme fire scenarios.

Commercial Area, Industries Area, Other in the Global High Temperature Smoke Extraction Motor Market:

The Global High Temperature Smoke Extraction Motor Market finds its usage across various areas, including commercial, industrial, and other specialized settings. In commercial areas, these motors are integral to the fire safety systems of buildings such as shopping malls, office complexes, hotels, and hospitals. These environments often have high foot traffic and require efficient smoke extraction systems to ensure the safety of occupants during a fire emergency. The motors help in quickly clearing smoke and toxic fumes, facilitating safe evacuation and minimizing potential damage to property. In industrial areas, the usage of high-temperature smoke extraction motors is even more critical. Factories, manufacturing plants, and warehouses often deal with hazardous materials and processes that can increase the risk of fire. The motors in these settings are designed to operate under extreme conditions, ensuring that smoke and fumes are effectively extracted to prevent the spread of fire and protect both personnel and equipment. Additionally, these motors are essential in maintaining compliance with stringent industrial safety regulations. Other specialized areas where these motors are used include tunnels, underground facilities, and transportation hubs. In tunnels and underground facilities, the risk of fire is particularly high due to the confined spaces and limited ventilation. High-temperature smoke extraction motors are crucial in these environments to ensure that smoke is quickly cleared, providing a safe passage for evacuation and access for emergency responders. In transportation hubs such as airports and train stations, these motors play a vital role in maintaining safety and ensuring that operations can continue smoothly even in the event of a fire. Overall, the usage of high-temperature smoke extraction motors across these various areas highlights their importance in enhancing fire safety and protecting lives and property.

Global High Temperature Smoke Extraction Motor Market Outlook:

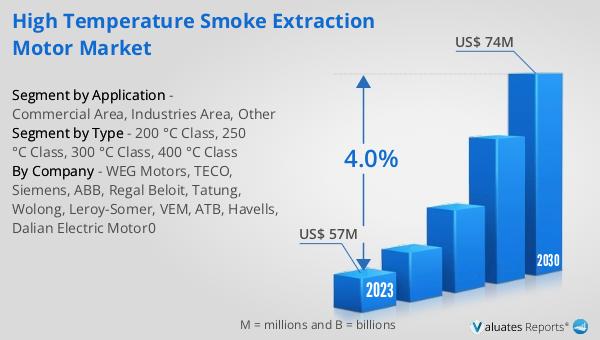

The global High Temperature Smoke Extraction Motor market was valued at US$ 57 million in 2023 and is anticipated to reach US$ 74 million by 2030, witnessing a CAGR of 4.0% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing awareness and implementation of fire safety measures across various sectors. The demand for high-temperature smoke extraction motors is expected to rise as more commercial and industrial facilities recognize the importance of having reliable smoke extraction systems in place. The projected growth also reflects the ongoing advancements in motor technology, which are enhancing the efficiency and reliability of these critical safety components. As urbanization and industrialization continue to expand globally, the need for robust fire safety solutions becomes even more pressing, further fueling the market's growth. The anticipated increase in market value underscores the vital role that high-temperature smoke extraction motors play in safeguarding lives and property, ensuring that buildings and facilities are well-equipped to handle fire emergencies effectively.

| Report Metric | Details |

| Report Name | High Temperature Smoke Extraction Motor Market |

| Accounted market size in 2023 | US$ 57 million |

| Forecasted market size in 2030 | US$ 74 million |

| CAGR | 4.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | WEG Motors, TECO, Siemens, ABB, Regal Beloit, Tatung, Wolong, Leroy-Somer, VEM, ATB, Havells, Dalian Electric Motor0 |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |