What is Global Master Data Management Solution Market?

The Global Master Data Management (MDM) Solution Market is a rapidly evolving sector that focuses on the management of critical business data. MDM solutions are designed to ensure the uniformity, accuracy, stewardship, semantic consistency, and accountability of an enterprise's official shared master data assets. These solutions are essential for businesses that operate on a global scale, as they help in managing data across different departments, regions, and systems. By centralizing and standardizing data, MDM solutions enable organizations to improve their decision-making processes, enhance operational efficiency, and ensure compliance with regulatory requirements. The market for these solutions is driven by the increasing need for data governance, the growing volume of data generated by businesses, and the rising demand for data quality and consistency. As companies continue to expand their operations globally, the importance of effective master data management becomes even more critical.

Customer Data, Product Data, Others in the Global Master Data Management Solution Market:

Customer data, product data, and other types of data are integral components of the Global Master Data Management Solution Market. Customer data encompasses all the information related to an organization's customers, including personal details, purchase history, preferences, and interactions. Managing customer data effectively is crucial for businesses to deliver personalized experiences, improve customer satisfaction, and drive loyalty. MDM solutions help in consolidating customer data from various sources, ensuring its accuracy and consistency, and making it accessible to different departments within the organization. Product data, on the other hand, includes information about the products or services offered by a company. This data can range from product specifications, pricing, and availability to descriptions, images, and reviews. Accurate and consistent product data is essential for businesses to manage their inventory, streamline their supply chain, and enhance their marketing efforts. MDM solutions enable organizations to maintain a single, unified view of their product data, which helps in reducing errors, improving time-to-market, and increasing sales. Apart from customer and product data, there are other types of data that organizations need to manage, such as supplier data, financial data, and employee data. Supplier data includes information about the vendors and partners that a company works with, such as contact details, contract terms, and performance metrics. Effective management of supplier data is crucial for businesses to ensure smooth operations, negotiate better deals, and mitigate risks. Financial data encompasses all the monetary transactions and records of an organization, including revenue, expenses, assets, and liabilities. Accurate financial data is essential for businesses to make informed decisions, comply with regulatory requirements, and maintain financial health. Employee data includes information about the organization's workforce, such as personal details, job roles, performance metrics, and compensation. Managing employee data effectively is important for businesses to optimize their human resources, improve employee engagement, and ensure compliance with labor laws. MDM solutions provide a centralized platform for managing all these types of data, ensuring their accuracy, consistency, and accessibility. By leveraging MDM solutions, organizations can break down data silos, improve data quality, and gain a holistic view of their operations. This, in turn, helps them to make better decisions, enhance operational efficiency, and drive business growth.

Banking, Finance and Insurance (BFSI), IT and Telecommunications, Government & Health Care, Manufacturing & Logistics, Others in the Global Master Data Management Solution Market:

The usage of Global Master Data Management Solution Market spans across various sectors, including Banking, Finance, and Insurance (BFSI), IT and Telecommunications, Government & Health Care, Manufacturing & Logistics, and others. In the BFSI sector, MDM solutions are used to manage customer data, financial transactions, and regulatory compliance. By ensuring the accuracy and consistency of customer data, banks and financial institutions can deliver personalized services, improve customer satisfaction, and reduce fraud. MDM solutions also help in consolidating financial data from different sources, enabling better risk management, regulatory reporting, and decision-making. In the IT and Telecommunications sector, MDM solutions are used to manage large volumes of customer and product data. Telecom companies can leverage MDM solutions to maintain accurate customer records, streamline billing processes, and enhance customer service. By managing product data effectively, IT companies can improve their product development cycles, reduce time-to-market, and increase sales. In the Government & Health Care sector, MDM solutions are used to manage citizen and patient data. Governments can use MDM solutions to maintain accurate records of citizens, streamline public services, and ensure compliance with regulations. In the healthcare sector, MDM solutions help in managing patient data, improving the quality of care, and ensuring compliance with health regulations. In the Manufacturing & Logistics sector, MDM solutions are used to manage product, supplier, and inventory data. By maintaining accurate product data, manufacturers can improve their production processes, reduce errors, and increase efficiency. MDM solutions also help in managing supplier data, enabling better supplier relationships and reducing supply chain risks. In the logistics sector, MDM solutions help in managing inventory data, improving order fulfillment, and reducing operational costs. Apart from these sectors, MDM solutions are also used in other industries such as retail, education, and energy. In the retail sector, MDM solutions help in managing product and customer data, enabling personalized marketing, improving inventory management, and increasing sales. In the education sector, MDM solutions help in managing student and faculty data, improving administrative processes, and enhancing the quality of education. In the energy sector, MDM solutions help in managing asset and customer data, improving operational efficiency, and ensuring regulatory compliance. Overall, the usage of MDM solutions across various sectors highlights their importance in managing critical business data, improving operational efficiency, and driving business growth.

Global Master Data Management Solution Market Outlook:

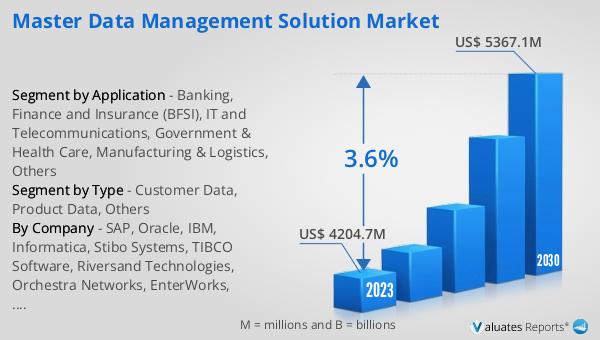

The global Master Data Management Solution market was valued at US$ 4204.7 million in 2023 and is anticipated to reach US$ 5367.1 million by 2030, witnessing a CAGR of 3.6% during the forecast period 2024-2030. This market growth reflects the increasing importance of data management in today's business environment. As organizations continue to generate vast amounts of data, the need for effective data management solutions becomes more critical. MDM solutions help businesses to centralize and standardize their data, ensuring its accuracy, consistency, and accessibility. This, in turn, enables organizations to make better decisions, improve operational efficiency, and drive business growth. The growing adoption of digital technologies, the increasing focus on data governance, and the rising demand for data quality and consistency are some of the key factors driving the growth of the MDM market. As businesses continue to expand their operations globally, the importance of effective master data management will only increase, further fueling the demand for MDM solutions.

| Report Metric | Details |

| Report Name | Master Data Management Solution Market |

| Accounted market size in 2023 | US$ 4204.7 million |

| Forecasted market size in 2030 | US$ 5367.1 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | SAP, Oracle, IBM, Informatica, Stibo Systems, TIBCO Software, Riversand Technologies, Orchestra Networks, EnterWorks, Magnitude, Talend, SAS Institute, Microsoft, KPMG, Teradata, Software AG, Agility Multichannel, VisionWare, SupplyOn AG, Sunway World, Yonyou |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |