What is Global Natural Astaxanthin Powder Market?

The Global Natural Astaxanthin Powder Market refers to the worldwide industry focused on the production, distribution, and consumption of natural astaxanthin powder. Astaxanthin is a powerful antioxidant found in certain marine organisms like microalgae, yeast, salmon, trout, krill, shrimp, crayfish, and crustaceans. This market is driven by the increasing awareness of the health benefits associated with astaxanthin, such as its anti-inflammatory properties, ability to improve skin health, and potential to enhance athletic performance. The demand for natural astaxanthin powder is growing across various sectors, including nutraceuticals, cosmetics, food and beverages, and animal feed. The market is characterized by a diverse range of suppliers and manufacturers who are constantly innovating to improve the quality and efficacy of their products. As consumers become more health-conscious and seek natural alternatives to synthetic supplements, the global natural astaxanthin powder market is expected to continue its upward trajectory.

Astaxanthin Oleoresin, Astaxanthin Powder, Others in the Global Natural Astaxanthin Powder Market:

Astaxanthin Oleoresin, Astaxanthin Powder, and other forms of astaxanthin are integral components of the Global Natural Astaxanthin Powder Market. Astaxanthin Oleoresin is a highly concentrated form of astaxanthin extracted from microalgae, typically Haematococcus pluvialis. This oleoresin is rich in antioxidants and is used in various applications, including dietary supplements, cosmetics, and pharmaceuticals. It is known for its superior bioavailability, meaning it is more easily absorbed by the body, making it a preferred choice for many health products. On the other hand, Astaxanthin Powder is a dried form of the pigment, which is also derived from microalgae. This powder is versatile and can be easily incorporated into a wide range of products, from capsules and tablets to functional foods and beverages. The powder form is particularly popular in the nutraceutical industry due to its ease of use and stability. Other forms of astaxanthin include beadlets, emulsions, and water-dispersible powders, which are designed to enhance the solubility and bioavailability of astaxanthin in various formulations. These different forms of astaxanthin cater to the diverse needs of consumers and manufacturers, ensuring that the benefits of this potent antioxidant can be harnessed in multiple ways. The global market for natural astaxanthin powder is thus characterized by a wide array of products, each tailored to specific applications and consumer preferences. As research continues to uncover new benefits and applications of astaxanthin, the market is expected to expand further, offering even more innovative and effective products to meet the growing demand for natural health solutions.

Nutraceuticals, Cosmetics, Food & Beverages, Feed, Others in the Global Natural Astaxanthin Powder Market:

The Global Natural Astaxanthin Powder Market finds extensive usage across several key areas, including Nutraceuticals, Cosmetics, Food & Beverages, Feed, and others. In the Nutraceuticals sector, astaxanthin powder is highly valued for its potent antioxidant properties, which help in combating oxidative stress and inflammation. It is commonly used in dietary supplements aimed at improving cardiovascular health, enhancing immune function, and supporting joint health. The Cosmetics industry also leverages the benefits of astaxanthin powder, incorporating it into skincare products due to its ability to protect the skin from UV damage, reduce wrinkles, and improve skin elasticity. In the Food & Beverages sector, astaxanthin powder is used as a natural colorant and a nutritional additive, enriching products with its health-boosting properties. It is often added to functional foods, energy drinks, and health bars to enhance their nutritional profile. The Feed industry utilizes astaxanthin powder primarily in aquaculture, where it is added to the feed of farmed fish and crustaceans to improve their coloration and overall health. This not only makes the seafood more appealing to consumers but also enhances the nutritional value of the end product. Other applications of astaxanthin powder include its use in pharmaceuticals, where it is being explored for its potential in treating various health conditions, and in animal nutrition, where it is used to improve the health and productivity of livestock. The versatility of astaxanthin powder and its wide range of applications make it a valuable ingredient in multiple industries, driving the growth of the global market.

Global Natural Astaxanthin Powder Market Outlook:

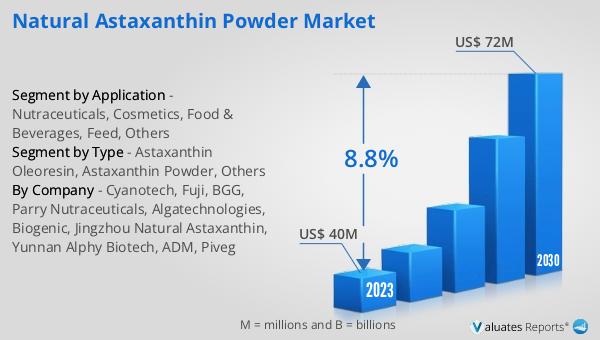

The global market for Natural Astaxanthin Powder was valued at $40 million in 2023 and is projected to reach $72 million by 2030, reflecting a compound annual growth rate (CAGR) of 8.8% during the forecast period from 2024 to 2030. This significant growth can be attributed to the increasing awareness of the health benefits associated with natural astaxanthin, as well as the rising demand for natural and sustainable products across various industries. The market's expansion is also driven by advancements in extraction and production technologies, which have improved the quality and availability of natural astaxanthin powder. As consumers continue to prioritize health and wellness, the demand for natural astaxanthin powder is expected to rise, further propelling the market's growth.

| Report Metric | Details |

| Report Name | Natural Astaxanthin Powder Market |

| Accounted market size in 2023 | US$ 40 million |

| Forecasted market size in 2030 | US$ 72 million |

| CAGR | 8.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Cyanotech, Fuji, BGG, Parry Nutraceuticals, Algatechnologies, Biogenic, Jingzhou Natural Astaxanthin, Yunnan Alphy Biotech, ADM, Piveg |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |