What is Global PET Bottles & Containers Market?

The Global PET Bottles & Containers Market refers to the worldwide industry involved in the production, distribution, and sale of polyethylene terephthalate (PET) bottles and containers. PET is a type of plastic that is widely used due to its strength, lightweight nature, and recyclability. These bottles and containers are commonly used for packaging beverages, food, pharmaceuticals, and various fast-moving consumer goods (FMCG). The market is driven by the increasing demand for convenient and sustainable packaging solutions. PET bottles and containers are favored for their ability to preserve the quality and extend the shelf life of products. Additionally, the growing awareness about environmental issues and the push for recycling have further boosted the demand for PET packaging. The market encompasses a wide range of products, from small beverage bottles to large containers used for bulk storage. The versatility and cost-effectiveness of PET make it a preferred choice for manufacturers and consumers alike. The global market is characterized by continuous innovation, with companies investing in new technologies to improve the performance and sustainability of PET packaging.

Colorful Type, Transparent Type in the Global PET Bottles & Containers Market:

In the Global PET Bottles & Containers Market, products can be broadly categorized into two types: colorful and transparent. Colorful PET bottles and containers are often used for branding and aesthetic purposes. They allow companies to differentiate their products on the shelves and attract consumers with vibrant and appealing packaging. These colorful containers can be found in various shades and are commonly used for beverages, personal care products, and household items. The use of color not only enhances the visual appeal but also helps in protecting the contents from light exposure, which can degrade certain products. On the other hand, transparent PET bottles and containers are highly valued for their clarity and ability to showcase the product inside. This transparency is particularly important for food and beverage packaging, where consumers prefer to see the product before purchasing. Transparent PET containers are also used in the pharmaceutical industry, where visibility of the contents is crucial for safety and compliance. Both colorful and transparent PET bottles and containers offer excellent barrier properties, ensuring that the contents remain fresh and uncontaminated. The choice between colorful and transparent packaging often depends on the product type, brand strategy, and consumer preferences. Manufacturers are continually exploring new colorants and additives to enhance the functionality and appeal of PET packaging. Additionally, advancements in recycling technologies are enabling the production of high-quality recycled PET (rPET) in both colorful and transparent forms, contributing to the sustainability goals of the industry. The market for colorful and transparent PET bottles and containers is expected to grow as consumers and brands increasingly prioritize aesthetics, functionality, and environmental impact in their packaging choices.

Beverages and Food, Pharmaceutical, FMCG, Others in the Global PET Bottles & Containers Market:

The usage of Global PET Bottles & Containers Market spans across various sectors, including beverages and food, pharmaceuticals, FMCG, and others. In the beverages and food industry, PET bottles and containers are extensively used for packaging water, soft drinks, juices, dairy products, and edible oils. Their lightweight nature and durability make them ideal for transporting and storing liquids. PET packaging also ensures that the contents remain fresh and free from contamination, which is crucial for maintaining the quality and safety of food and beverages. In the pharmaceutical sector, PET bottles and containers are used for packaging medicines, vitamins, and other health supplements. The transparency of PET allows for easy identification of the contents, while its excellent barrier properties protect the products from moisture, oxygen, and other external factors that could compromise their efficacy. The FMCG sector, which includes personal care products, household items, and cleaning agents, also relies heavily on PET packaging. The versatility of PET allows for the creation of various shapes and sizes of containers, catering to the diverse needs of FMCG products. Additionally, the recyclability of PET aligns with the growing consumer demand for sustainable packaging solutions. Other industries, such as automotive and electronics, also utilize PET bottles and containers for packaging lubricants, chemicals, and small components. The adaptability of PET to different forms and its ability to withstand various environmental conditions make it a preferred choice across multiple sectors. Overall, the widespread usage of PET bottles and containers in these areas highlights their importance in modern packaging solutions, driven by their practicality, safety, and environmental benefits.

Global PET Bottles & Containers Market Outlook:

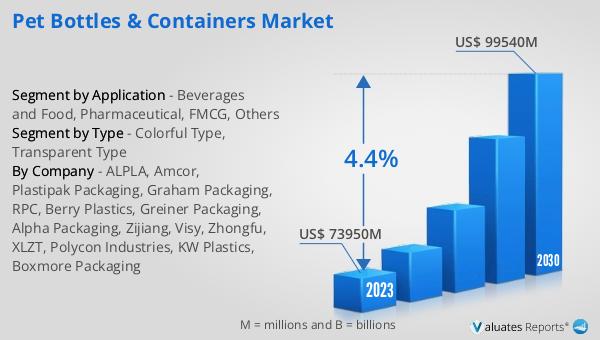

The global PET Bottles & Containers market was valued at US$ 73,950 million in 2023 and is anticipated to reach US$ 99,540 million by 2030, witnessing a compound annual growth rate (CAGR) of 4.4% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for PET packaging solutions across various industries. The market's expansion is driven by factors such as the rising consumption of packaged beverages and food, the growing pharmaceutical industry, and the need for sustainable and recyclable packaging materials. The versatility and cost-effectiveness of PET bottles and containers make them a preferred choice for manufacturers and consumers alike. Additionally, advancements in recycling technologies and the development of high-quality recycled PET (rPET) are contributing to the market's growth. As companies continue to innovate and invest in new technologies, the global PET Bottles & Containers market is expected to witness sustained growth, meeting the evolving needs of consumers and industries worldwide.

| Report Metric | Details |

| Report Name | PET Bottles & Containers Market |

| Accounted market size in 2023 | US$ 73950 million |

| Forecasted market size in 2030 | US$ 99540 million |

| CAGR | 4.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ALPLA, Amcor, Plastipak Packaging, Graham Packaging, RPC, Berry Plastics, Greiner Packaging, Alpha Packaging, Zijiang, Visy, Zhongfu, XLZT, Polycon Industries, KW Plastics, Boxmore Packaging |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |