What is Global Medical Laser Equipment Market?

The Global Medical Laser Equipment Market refers to the worldwide industry focused on the development, production, and distribution of laser-based devices used in various medical applications. These devices utilize laser technology to perform precise and minimally invasive procedures, offering significant advantages over traditional surgical methods. Medical lasers are employed in a wide range of fields, including ophthalmology, dermatology, oncology, and cardiology, among others. The market encompasses various types of laser systems, each designed for specific medical purposes, such as solid-state lasers, gas lasers, dye lasers, and semiconductor lasers. The increasing prevalence of chronic diseases, advancements in laser technology, and the growing demand for minimally invasive surgeries are key factors driving the growth of this market. Additionally, the rising awareness about the benefits of laser treatments and the expanding applications of medical lasers in both therapeutic and diagnostic procedures contribute to the market's expansion. The Global Medical Laser Equipment Market is characterized by continuous innovation and the introduction of new products, aiming to enhance patient outcomes and improve the efficiency of medical procedures.

Solid State Laser System, Gas Laser System, Dye Laser System, Semiconductor Laser System in the Global Medical Laser Equipment Market:

Solid State Laser Systems, Gas Laser Systems, Dye Laser Systems, and Semiconductor Laser Systems are integral components of the Global Medical Laser Equipment Market, each offering unique advantages and applications. Solid State Laser Systems utilize solid materials, such as crystals or glasses doped with rare earth or transition metal ions, as the gain medium. These lasers are known for their high power output and precision, making them ideal for applications like ophthalmic surgeries, where accuracy is paramount. Gas Laser Systems, on the other hand, use gases like carbon dioxide, argon, or helium-neon as the lasing medium. Carbon dioxide lasers are particularly effective in cutting and vaporizing soft tissues, making them valuable in dermatology and general surgery. Argon lasers are commonly used in ophthalmology for retinal phototherapy. Dye Laser Systems employ organic dyes in liquid solution as the lasing medium, offering tunable wavelengths that can be adjusted for specific applications. These lasers are often used in dermatology for treating vascular lesions and in oncology for photodynamic therapy. Semiconductor Laser Systems, also known as diode lasers, use semiconductor materials as the gain medium. They are compact, efficient, and versatile, making them suitable for a wide range of medical applications, including dental procedures, hair removal, and photocoagulation in ophthalmology. Each type of laser system brings distinct benefits to the medical field, contributing to the overall growth and diversification of the Global Medical Laser Equipment Market. The continuous advancements in laser technology, coupled with the increasing demand for minimally invasive procedures, are driving the adoption of these laser systems across various medical specialties.

General Surgery, Cosmetic Surgery, Dental Surgery in the Global Medical Laser Equipment Market:

The usage of Global Medical Laser Equipment Market spans several critical areas, including General Surgery, Cosmetic Surgery, and Dental Surgery, each benefiting from the precision and efficiency of laser technology. In General Surgery, medical lasers are used for a variety of procedures such as tissue cutting, coagulation, and ablation. The precision of laser technology allows surgeons to perform minimally invasive surgeries with reduced bleeding, lower risk of infection, and faster recovery times for patients. Procedures like laparoscopic surgeries, removal of tumors, and treatment of varicose veins are commonly performed using laser equipment. In Cosmetic Surgery, lasers play a pivotal role in procedures aimed at enhancing aesthetic appearance. Laser-based treatments such as laser skin resurfacing, hair removal, and tattoo removal are highly popular due to their effectiveness and minimal downtime. Lasers are also used for treating skin conditions like acne scars, wrinkles, and pigmentation issues, providing patients with improved skin texture and tone. In Dental Surgery, lasers are revolutionizing the way dental procedures are performed. Laser dentistry offers a less invasive alternative to traditional methods, reducing pain and discomfort for patients. Lasers are used for procedures such as cavity preparation, gum reshaping, and teeth whitening. They also help in the treatment of periodontal disease by removing infected tissue and promoting the regeneration of healthy tissue. The versatility and precision of laser technology make it an invaluable tool in these medical fields, enhancing the quality of care and patient outcomes. The growing adoption of laser equipment in General Surgery, Cosmetic Surgery, and Dental Surgery underscores the significant impact of the Global Medical Laser Equipment Market on modern medical practices.

Global Medical Laser Equipment Market Outlook:

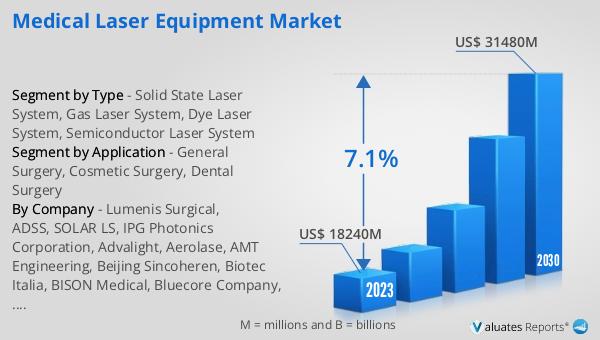

The global Medical Laser Equipment market was valued at US$ 18,240 million in 2023 and is anticipated to reach US$ 31,480 million by 2030, witnessing a CAGR of 7.1% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth trajectory highlights the increasing demand for advanced medical technologies, including laser equipment, driven by factors such as the rising prevalence of chronic diseases, technological advancements, and the growing preference for minimally invasive procedures. The expanding applications of medical lasers in various therapeutic and diagnostic fields further contribute to the market's robust growth. As healthcare providers continue to seek innovative solutions to improve patient outcomes and operational efficiency, the Global Medical Laser Equipment Market is poised for significant expansion in the coming years.

| Report Metric | Details |

| Report Name | Medical Laser Equipment Market |

| Accounted market size in 2023 | US$ 18240 million |

| Forecasted market size in 2030 | US$ 31480 million |

| CAGR | 7.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Lumenis Surgical, ADSS, SOLAR LS, IPG Photonics Corporation, Advalight, Aerolase, AMT Engineering, Beijing Sincoheren, Biotec Italia, BISON Medical, Bluecore Company, BTL International, Candela Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |