What is Global Air Intake Cooling System Market?

The Global Air Intake Cooling System Market refers to the industry focused on technologies and solutions designed to cool the air intake of various machinery and engines. These systems are crucial for enhancing the efficiency and performance of engines, particularly in environments where high temperatures can negatively impact operations. By cooling the air before it enters the engine, these systems help in increasing the air density, which in turn improves combustion efficiency and power output. This market encompasses a wide range of products and technologies, including evaporative coolers, atomizers, chillers, and mechanical refrigeration systems. These solutions are employed across various industries such as power generation, LNG (Liquefied Natural Gas) production, and other sectors where maintaining optimal engine performance is critical. The market is driven by the need for energy efficiency, regulatory requirements, and the growing demand for high-performance engines in industrial applications. As industries continue to seek ways to improve operational efficiency and reduce emissions, the demand for advanced air intake cooling systems is expected to grow.

Evaporative Coolers and Atomizers, Chillers and Mechanical Refrigeration in the Global Air Intake Cooling System Market:

Evaporative coolers and atomizers, chillers, and mechanical refrigeration systems are key components of the Global Air Intake Cooling System Market. Evaporative coolers work by using the natural process of water evaporation to cool the air. When air passes through water-saturated pads, it loses heat through evaporation, resulting in cooler air. This method is energy-efficient and environmentally friendly, making it a popular choice in regions with hot and dry climates. Atomizers, on the other hand, disperse fine droplets of water into the air intake stream. These droplets evaporate quickly, absorbing heat from the air and thereby cooling it. Atomizers are particularly effective in applications where precise control over air temperature is required. Chillers are another critical component, using refrigerants to remove heat from the air. They operate by circulating a coolant through a closed-loop system, which absorbs heat from the air intake and releases it elsewhere. Chillers are highly effective in maintaining consistent air temperatures, making them suitable for applications where precise temperature control is essential. Mechanical refrigeration systems, similar to chillers, use a refrigeration cycle to cool the air. These systems are highly efficient and can operate in a wide range of environmental conditions. They are commonly used in industrial applications where large volumes of air need to be cooled quickly and efficiently. Each of these technologies has its own advantages and is chosen based on the specific requirements of the application. For instance, evaporative coolers and atomizers are often preferred in regions with high ambient temperatures and low humidity, while chillers and mechanical refrigeration systems are used in environments where precise temperature control is critical. The choice of technology also depends on factors such as energy efficiency, environmental impact, and operational costs. As industries continue to seek ways to improve efficiency and reduce emissions, the demand for advanced air intake cooling systems is expected to grow.

Power Industry, LNG Industry in the Global Air Intake Cooling System Market:

The usage of Global Air Intake Cooling Systems in the power industry and LNG industry is crucial for maintaining optimal performance and efficiency. In the power industry, these systems are used to cool the air intake of gas turbines and other power generation equipment. Gas turbines are highly sensitive to the temperature of the intake air, with higher temperatures leading to reduced efficiency and power output. By cooling the intake air, these systems help to increase the density of the air, which in turn improves combustion efficiency and power output. This is particularly important in regions with high ambient temperatures, where the performance of gas turbines can be significantly impacted. In addition to improving efficiency, air intake cooling systems also help to reduce emissions by ensuring more complete combustion of the fuel. This is a critical consideration for power plants, which are subject to stringent environmental regulations. In the LNG industry, air intake cooling systems are used to maintain the performance of compressors and other equipment used in the liquefaction process. The LNG production process involves compressing natural gas to high pressures and then cooling it to extremely low temperatures to convert it into a liquid. The efficiency of this process is highly dependent on the temperature of the intake air, with cooler air leading to more efficient compression and liquefaction. By cooling the intake air, these systems help to improve the overall efficiency of the LNG production process, reducing energy consumption and operational costs. In addition to improving efficiency, air intake cooling systems also help to enhance the reliability and lifespan of the equipment used in the LNG production process. By maintaining optimal operating temperatures, these systems help to reduce wear and tear on the equipment, leading to lower maintenance costs and longer equipment life. As the demand for LNG continues to grow, the importance of air intake cooling systems in the LNG industry is expected to increase.

Global Air Intake Cooling System Market Outlook:

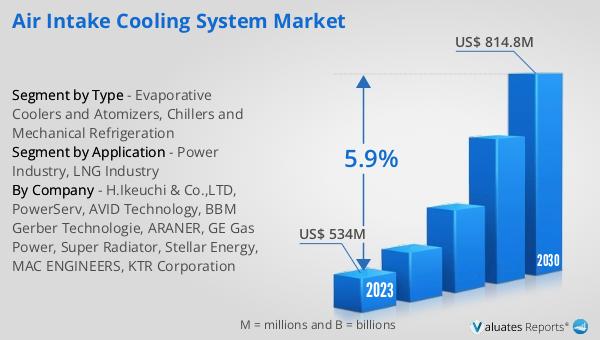

The global Air Intake Cooling System market was valued at US$ 534 million in 2023 and is anticipated to reach US$ 814.8 million by 2030, witnessing a CAGR of 5.9% during the forecast period 2024-2030. This growth is driven by the increasing demand for energy-efficient solutions and the need to comply with stringent environmental regulations. As industries continue to seek ways to improve operational efficiency and reduce emissions, the demand for advanced air intake cooling systems is expected to grow. These systems play a crucial role in enhancing the performance and efficiency of engines and machinery, particularly in environments with high ambient temperatures. By cooling the intake air, these systems help to increase the density of the air, which in turn improves combustion efficiency and power output. This is particularly important in industries such as power generation and LNG production, where maintaining optimal performance and efficiency is critical. The market is also driven by advancements in technology, with new and innovative solutions being developed to meet the evolving needs of various industries. As the demand for high-performance engines and machinery continues to grow, the importance of air intake cooling systems is expected to increase.

| Report Metric | Details |

| Report Name | Air Intake Cooling System Market |

| Accounted market size in 2023 | US$ 534 million |

| Forecasted market size in 2030 | US$ 814.8 million |

| CAGR | 5.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | H.Ikeuchi & Co.,LTD, PowerServ, AVID Technology, BBM Gerber Technologie, ARANER, GE Gas Power, Super Radiator, Stellar Energy, MAC ENGINEERS, KTR Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |