What is Global Non-absorbable Mesh Market?

The Global Non-absorbable Mesh Market refers to the market for surgical meshes that are designed to remain in the body permanently. These meshes are primarily used in various types of surgeries to provide long-term support to weakened or damaged tissue. Unlike absorbable meshes, which dissolve over time, non-absorbable meshes are made from materials that do not break down in the body. This makes them ideal for procedures where long-term reinforcement is necessary. The market includes a variety of products made from different materials such as polypropylene, polyester, and expanded polytetrafluoroethylene (ePTFE). These meshes are commonly used in hernia repair, traumatic or surgical wound treatment, and other types of fascial surgery. The demand for non-absorbable meshes is driven by factors such as the increasing prevalence of hernias, advancements in surgical techniques, and the growing aging population, which is more prone to conditions requiring surgical intervention. The market is also influenced by regulatory approvals, technological innovations, and the availability of skilled healthcare professionals.

Polypropylene Mesh, Polyester Mesh, Expanded PTFE Mesh, Others in the Global Non-absorbable Mesh Market:

Polypropylene mesh is one of the most commonly used types of non-absorbable mesh in the global market. It is known for its strength, flexibility, and biocompatibility, making it suitable for a wide range of surgical applications. Polypropylene mesh is often used in hernia repair surgeries due to its ability to provide robust support to the abdominal wall. Polyester mesh, on the other hand, is another popular option. It is known for its high tensile strength and durability. Polyester mesh is often used in procedures that require a strong and long-lasting material, such as in the repair of large or complex hernias. Expanded PTFE (ePTFE) mesh is a unique type of non-absorbable mesh that is known for its exceptional biocompatibility and minimal tissue reaction. ePTFE mesh is often used in surgeries where minimizing the risk of infection and inflammation is crucial. Other types of non-absorbable meshes include those made from materials like nylon and silicone. These meshes are used in specialized surgical procedures and offer unique properties such as elasticity and resistance to degradation. The choice of mesh material depends on various factors, including the type of surgery, the patient's condition, and the surgeon's preference. Each type of mesh has its own set of advantages and limitations, and the selection process involves careful consideration of these factors to ensure the best possible outcome for the patient.

Hernia Repair, Traumatic or Surgical Wounds, Other Fascial Surgery in the Global Non-absorbable Mesh Market:

The usage of non-absorbable mesh in hernia repair is one of the most common applications in the global market. Hernias occur when an organ or tissue protrudes through a weak spot in the abdominal wall, and non-absorbable mesh is used to reinforce the area and prevent recurrence. The mesh provides a scaffold for tissue growth, ensuring long-term stability and reducing the risk of complications. In the treatment of traumatic or surgical wounds, non-absorbable mesh is used to provide structural support to damaged tissue. This is particularly important in cases where the wound is large or complex, and natural healing processes are insufficient. The mesh helps to hold the tissue together, promoting healing and reducing the risk of infection. In other types of fascial surgery, non-absorbable mesh is used to repair and reinforce the fascia, which is the connective tissue that surrounds muscles and organs. This is often necessary in cases where the fascia has been weakened or damaged due to injury, surgery, or medical conditions. The mesh provides long-term support, helping to restore function and prevent further complications. Overall, the use of non-absorbable mesh in these areas has revolutionized surgical practices, providing a reliable and effective solution for a wide range of medical conditions.

Global Non-absorbable Mesh Market Outlook:

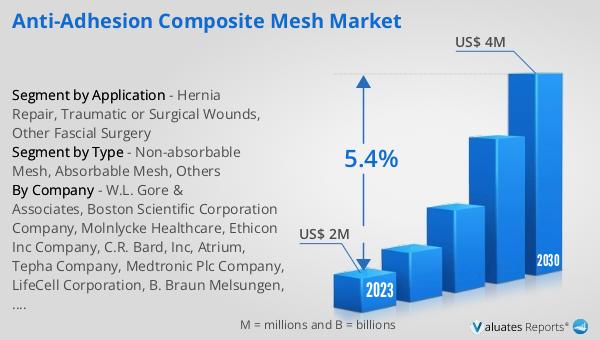

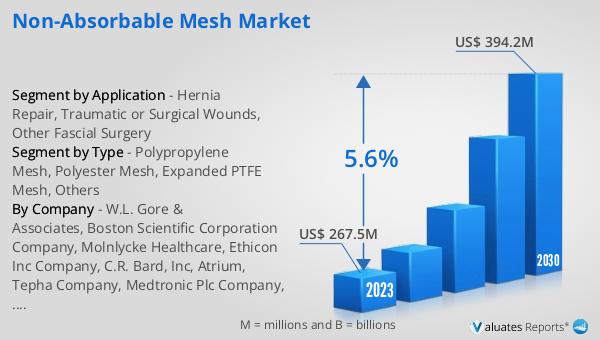

The global non-absorbable mesh market was valued at $267.5 million in 2023 and is projected to grow to $394.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2024 to 2030. This growth is driven by several factors, including the increasing prevalence of conditions that require surgical intervention, advancements in medical technology, and the growing aging population. The demand for non-absorbable mesh is expected to rise as more patients seek effective and long-lasting solutions for conditions such as hernias, traumatic wounds, and other types of fascial surgery. Additionally, the market is influenced by regulatory approvals and the availability of skilled healthcare professionals who can perform these complex surgical procedures. The increasing awareness about the benefits of non-absorbable mesh, such as its durability and biocompatibility, is also contributing to market growth. As healthcare systems around the world continue to evolve, the demand for high-quality surgical materials like non-absorbable mesh is expected to increase, driving further innovation and development in this field.

| Report Metric | Details |

| Report Name | Non-absorbable Mesh Market |

| Accounted market size in 2023 | US$ 267.5 million |

| Forecasted market size in 2030 | US$ 394.2 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | W.L. Gore & Associates, Boston Scientific Corporation Company, Molnlycke Healthcare, Ethicon Inc Company, C.R. Bard, Inc, Atrium, Tepha Company, Medtronic Plc Company, LifeCell Corporation, B. Braun Melsungen, Johnson & Johnson, Transeasy Medical Tech, Sinolinks Medical Innovation, Dikang Zhongke Biomedical Material, Touchstone International Medical Science, Panther Medical Equipment, Jiangsu Canopus Wisdom Medical Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |