What is Global Integrated Circuit Packaging and Testing Technology Market?

The Global Integrated Circuit Packaging and Testing Technology Market is a crucial segment of the semiconductor industry, focusing on the final stages of semiconductor device fabrication. This market encompasses a wide array of processes, including the packaging of integrated circuits (ICs) and the testing of these packaged components to ensure they meet the required specifications and standards. Packaging is an essential step that involves encasing the ICs in a protective material to safeguard them from physical damage and environmental factors, thereby enhancing their performance and reliability. Testing, on the other hand, is conducted to verify the functionality and performance of the ICs against the desired outcomes. This ensures that only the components that meet the stringent quality criteria make it to the market. As electronic devices become more sophisticated, the demand for advanced packaging and testing technologies grows, driving innovation and development in this sector. The importance of this market lies not only in its role in maintaining the quality and reliability of electronic products but also in its contribution to the overall growth and evolution of the semiconductor industry.

IDM Mode, Foundry Mode in the Global Integrated Circuit Packaging and Testing Technology Market:

In the Global Integrated Circuit Packaging and Testing Technology Market, two primary business models prevail: IDM Mode and Foundry Mode. IDM (Integrated Device Manufacturer) Mode refers to companies that handle the entire production process of their semiconductor products. This includes designing, manufacturing, packaging, and testing of the ICs. Companies operating in IDM Mode benefit from a high degree of control over their production processes and product quality. They can quickly adapt to new technologies and maintain tighter security on their intellectual property. However, this model requires significant capital investment in fabrication plants, equipment, and research and development. On the other hand, the Foundry Mode involves companies that specialize in manufacturing ICs designed by their clients. These foundries focus solely on the fabrication aspect, leaving the design, packaging, and testing to their clients or third-party service providers. This model allows for a more flexible production scale, enabling companies to adjust their output based on market demand without the need for heavy investment in manufacturing facilities. Foundries can achieve economies of scale by serving multiple clients, which can lead to lower production costs per unit. Both IDM and Foundry Modes play vital roles in the Global Integrated Circuit Packaging and Testing Technology Market, catering to different needs within the semiconductor industry and driving innovation through their specialized approaches.

Consumer Electronics, Transportation, Medical, Aerospace, Others in the Global Integrated Circuit Packaging and Testing Technology Market:

The Global Integrated Circuit Packaging and Testing Technology Market finds its applications across a diverse range of sectors, including Consumer Electronics, Transportation, Medical, Aerospace, among others. In Consumer Electronics, this technology is pivotal for the reliability and performance of devices such as smartphones, tablets, and laptops, ensuring they meet the consumers' increasing demands for faster, more efficient gadgets. In the Transportation sector, advanced IC packaging and testing are essential for the development of safer, more reliable automotive electronics, including navigation, infotainment, and autonomous driving systems. The Medical field benefits from this technology through the enhancement of medical devices' precision and reliability, critical for patient monitoring, diagnostics, and treatment equipment. Aerospace applications rely heavily on these technologies for the durability and performance of spacecraft and aviation electronics, where failure is not an option. Each of these sectors demands high standards for IC packaging and testing, given the critical nature of their applications. The technology not only ensures the performance and reliability of the ICs but also extends their lifespan, contributing significantly to the advancement and innovation within these industries.

Global Integrated Circuit Packaging and Testing Technology Market Outlook:

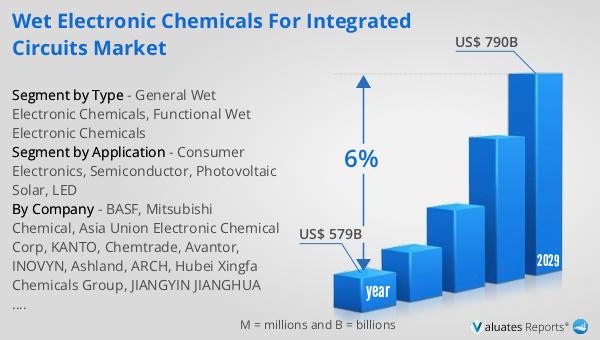

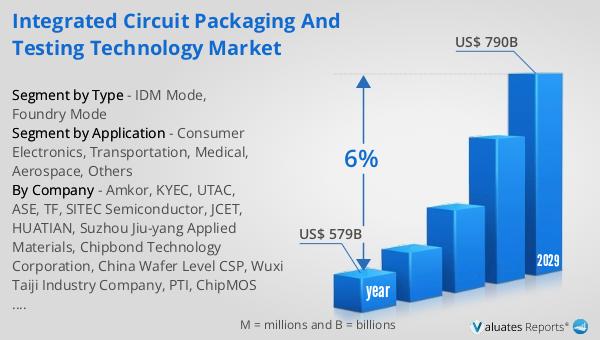

The outlook for the Global Integrated Circuit Packaging and Testing Technology Market is highly optimistic, with projections indicating a significant growth trajectory. In 2022, the market's valuation stood at approximately 579 billion US dollars, a figure that is expected to climb to around 790 billion US dollars by the year 2029. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 6% throughout the forecast period. Such an expansion reflects the increasing demand for semiconductor components across various sectors, driven by advancements in technology and the growing need for more sophisticated electronic devices. The market's growth is also indicative of the continuous innovation within the field of integrated circuit packaging and testing, as industry players strive to meet the evolving requirements of electronic device manufacturers. This positive outlook underscores the critical role of the Global Integrated Circuit Packaging and Testing Technology Market in the broader semiconductor industry, highlighting its contribution to the development of cutting-edge technologies and the enhancement of electronic device performance and reliability.

| Report Metric | Details |

| Report Name | Integrated Circuit Packaging and Testing Technology Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Amkor, KYEC, UTAC, ASE, TF, SITEC Semiconductor, JCET, HUATIAN, Suzhou Jiu-yang Applied Materials, Chipbond Technology Corporation, China Wafer Level CSP, Wuxi Taiji Industry Company, PTI, ChipMOS TECHNOLOGIES |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |