What is Global Flame Retardant Material Market?

The Global Flame Retardant Material Market is a sector that focuses on materials designed to slow down or prevent the spread of fire. These materials are crucial in enhancing fire safety across various industries, including construction, electronics, and automotive, among others. The market encompasses a wide range of substances, including chemicals and compounds, that are added to or treated with materials to impart flame retardancy. As safety regulations become stricter and the demand for fire-safe materials grows across the globe, the flame retardant material market is experiencing significant growth. Manufacturers and researchers are continuously working on developing more effective and environmentally friendly flame retardant solutions to meet the evolving needs of the market. This ongoing innovation and the increasing awareness about fire safety are key drivers behind the market's expansion. With a focus on protecting lives and property, the global flame retardant material market plays a pivotal role in today's safety-conscious world.

Flame Retardant Plastic, Fame Retardant Elastomer in the Global Flame Retardant Material Market:

Flame Retardant Plastic and Flame Retardant Elastomer are two critical categories within the Global Flame Retardant Material Market, each serving unique roles in enhancing fire safety across various applications. Flame Retardant Plastics are specially formulated polymers that are designed to resist ignition and slow the spread of flames. These plastics are widely used in the electronics, automotive, construction, and textile industries, where reducing the risk of fire is paramount. The development of these materials involves the incorporation of flame retardant chemicals into plastic compounds, which can then inhibit or delay the combustion process. On the other hand, Flame Retardant Elastomers are a type of synthetic rubber treated with flame retardant chemicals. These materials combine the flexibility and elasticity of rubber with enhanced fire resistance, making them ideal for use in seals, gaskets, and insulation in high-temperature environments. The demand for both flame retardant plastics and elastomers is driven by the need for safer materials that comply with global fire safety standards. As industries continue to prioritize fire safety, the development of advanced flame retardant materials that offer both performance and environmental sustainability is becoming increasingly important. This focus on innovation is leading to the creation of new flame retardant formulations that are less harmful to the environment while still providing effective fire protection.

Chemical Field, Metallurgical Field, Fire Field, Defense Field, Others in the Global Flame Retardant Material Market:

The usage of Global Flame Retardant Material Market spans across several fields, highlighting its versatility and critical importance in enhancing fire safety. In the Chemical Field, flame retardant materials are used in the production of safer chemicals and materials that are resistant to fire, thereby reducing the risk of accidents and enhancing overall safety. The Metallurgical Field benefits from these materials by incorporating them into metals and alloys to improve their fire resistance, which is crucial in applications where materials are exposed to high temperatures. In the Fire Field, flame retardant materials are integral in the development of firefighting gear, including suits and equipment, providing firefighters with protection against flames and heat. The Defense Field utilizes these materials in the manufacturing of vehicles, uniforms, and equipment to ensure the safety of personnel in fire-prone situations. Lastly, the "Others" category encompasses a wide range of applications, including furniture, textiles, and electronics, where flame retardant materials are used to reduce the flammability of products and enhance consumer safety. The diverse applications of flame retardant materials across these fields underscore their importance in modern society, where safety and protection against fire are paramount. The ongoing research and development in this market aim to produce more efficient and environmentally friendly flame retardant solutions, further broadening their usage and effectiveness in protecting lives and property.

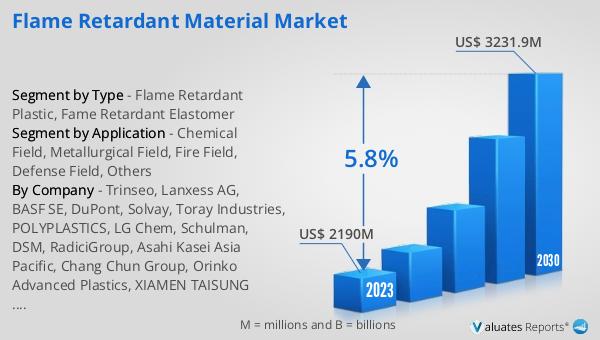

Global Flame Retardant Material Market Outlook:

The market outlook for the Global Flame Retardant Material Market presents a promising future, with the market's value standing at US$ 2190 million in 2023. It is projected to experience a growth trajectory, reaching an estimated value of US$ 3231.9 million by the year 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.8% during the forecast period spanning from 2024 to 2030. This positive outlook is indicative of the increasing demand for flame retardant materials across various industries, driven by heightened safety regulations and a growing awareness of the importance of fire safety. The market's expansion reflects the ongoing efforts to develop more effective and environmentally friendly flame retardant solutions that can meet the stringent safety standards while also addressing environmental concerns. As industries continue to prioritize fire safety, the demand for innovative flame retardant materials is set to rise, further fueling the market's growth in the coming years.

| Report Metric | Details |

| Report Name | Flame Retardant Material Market |

| Accounted market size in 2023 | US$ 2190 million |

| Forecasted market size in 2030 | US$ 3231.9 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Trinseo, Lanxess AG, BASF SE, DuPont, Solvay, Toray Industries, POLYPLASTICS, LG Chem, Schulman, DSM, RadiciGroup, Asahi Kasei Asia Pacific, Chang Chun Group, Orinko Advanced Plastics, XIAMEN TAISUNG POLYMER, CHIMEI Corporation, Kingfa Sci & Tech, Shanghai Pret Composites, Polyrocks Chemical, Super-Dragon Engineering Plastic, China National Bluestar (Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |