What is Global Liquid Dissolved Oxygen Analyzers Market?

The Global Liquid Dissolved Oxygen Analyzers Market is a specialized sector within the broader market for analytical instruments, focusing on devices designed to measure the amount of dissolved oxygen in liquid media. These analyzers are crucial for various applications where monitoring the oxygen levels in liquids is essential for ensuring the quality and safety of processes and products. For instance, in water treatment facilities, maintaining the right level of dissolved oxygen is vital for supporting aquatic life and preventing the proliferation of anaerobic organisms that could lead to water quality issues. Similarly, in the pharmaceutical and food and beverage industries, controlling oxygen levels is key to preventing oxidation that can degrade product quality. The market for these analyzers is driven by technological advancements that offer more accurate, reliable, and user-friendly devices, as well as by the growing awareness of the importance of water quality and environmental monitoring. As industries and regulatory bodies continue to emphasize the need for precise and continuous monitoring, the demand for liquid dissolved oxygen analyzers is expected to rise, reflecting the market's response to these global trends and regulatory requirements.

Fixed, Portable in the Global Liquid Dissolved Oxygen Analyzers Market:

The Global Liquid Dissolved Oxygen Analyzers Market, categorized into fixed and portable analyzers, caters to a wide array of applications, each with its unique requirements and challenges. Fixed analyzers are typically installed at a specific location where continuous monitoring of dissolved oxygen is necessary. These are often found in water treatment plants, aquaculture systems, and industrial processes where a constant watch on oxygen levels is crucial for operational efficiency and product quality. On the other hand, portable dissolved oxygen analyzers offer flexibility and convenience, allowing users to conduct spot checks and assessments in various locations. This is particularly useful in environmental monitoring, where researchers and field workers need to measure oxygen levels in multiple sites, such as rivers, lakes, and oceans, to assess water quality and ecological health. Both types of analyzers play pivotal roles in their respective domains, with advancements in sensor technology, data analytics, and wireless communication enhancing their functionality and application scope. As industries and environmental agencies increasingly focus on precision, reliability, and ease of use, the market for both fixed and portable liquid dissolved oxygen analyzers is expanding, driven by the need for comprehensive monitoring solutions that can adapt to diverse and changing requirements.

General Manufacturing, Semiconductors, Water Treatment, Others in the Global Liquid Dissolved Oxygen Analyzers Market:

The usage of the Global Liquid Dissolved Oxygen Analyzers Market spans across several critical areas, including General Manufacturing, Semiconductors, Water Treatment, and Others, showcasing the versatility and essential nature of these devices in various industries. In General Manufacturing, monitoring dissolved oxygen is key to preventing corrosion in processes and ensuring the quality of products, especially in food and beverage and pharmaceutical sectors where oxidation can significantly affect product shelf life and safety. In the Semiconductor industry, where water purity is paramount, dissolved oxygen analyzers are used to ensure the water used in manufacturing processes does not compromise the quality of the semiconductors by introducing unwanted oxidation. Water Treatment facilities rely heavily on these analyzers to monitor and control the levels of dissolved oxygen, which is critical for the aerobic treatment processes and for maintaining the ecological balance in the treated water bodies. Other applications include environmental monitoring, where understanding oxygen levels in natural water bodies can indicate the health of ecosystems and help in the management of aquatic resources. The broad applicability of liquid dissolved oxygen analyzers underlines their importance in not only safeguarding industrial processes and products but also in protecting and preserving the environment.

Global Liquid Dissolved Oxygen Analyzers Market Outlook:

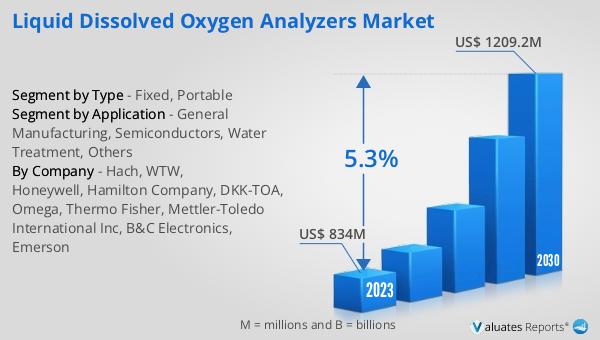

Regarding the market outlook for the Global Liquid Dissolved Oxygen Analyzers Market, it's noteworthy that the sector, valued at approximately US$ 834 million in 2023, is on a trajectory for significant growth. Projections suggest an increase to about US$ 1209.2 million by the year 2030. This anticipated growth, marked by a compound annual growth rate (CAGR) of 5.3% throughout the forecast period from 2024 to 2030, underscores the expanding relevance and demand for liquid dissolved oxygen analyzers across various industries. This upward trend is reflective of the increasing emphasis on water quality management, environmental monitoring, and the need for precise manufacturing processes across the globe. As industries continue to evolve and regulatory standards become more stringent, the reliance on advanced analytical technologies, including liquid dissolved oxygen analyzers, is expected to rise. This growth trajectory highlights the market's response to the growing awareness of the critical role that accurate and reliable dissolved oxygen measurement plays in ensuring the safety, efficiency, and sustainability of numerous operations and processes.

| Report Metric | Details |

| Report Name | Liquid Dissolved Oxygen Analyzers Market |

| Accounted market size in 2023 | US$ 834 million |

| Forecasted market size in 2030 | US$ 1209.2 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Hach, WTW, Honeywell, Hamilton Company, DKK-TOA, Omega, Thermo Fisher, Mettler-Toledo International Inc, B&C Electronics, Emerson |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |