What is Global Thermoplastic Polyolefin (TPO) Roofing Market?

The Global Thermoplastic Polyolefin (TPO) Roofing Market is a dynamic sector that focuses on providing roofing solutions with TPO materials. TPO, a type of single-ply roofing membrane, is made from the polymerization of ethylene-propylene rubber and polypropylene. It is widely recognized for its durability, flexibility, and resistance to ultraviolet light and chemical exposure. This market caters to a broad range of applications, offering products that are not only energy-efficient but also environmentally friendly. As of recent years, the demand for TPO roofing has seen a significant uptick due to its cost-effectiveness and performance efficiency compared to traditional roofing materials. The market's expansion is further fueled by the growing awareness among consumers and industries about the benefits of sustainable and green building materials. With advancements in technology and manufacturing processes, the Global Thermoplastic Polyolefin (TPO) Roofing Market is poised for continued growth, aiming to provide innovative roofing solutions that meet the evolving needs of modern construction.

45 mils, 60 mils, 80 mils, 90 mils, Others in the Global Thermoplastic Polyolefin (TPO) Roofing Market:

In the realm of the Global Thermoplastic Polyolefin (TPO) Roofing Market, the products are distinguished by their thickness, which is a critical factor in their performance and application. The thicknesses, measured in mils (a mil is one-thousandth of an inch), include 45 mils, 60 mils, 80 mils, 90 mils, among others, each serving specific requirements and preferences. The 45 mils TPO roofing is often selected for its lightweight and flexibility, making it suitable for a wide range of buildings, particularly where weight and budget are concerns. The 60 mils variant strikes a balance between durability and cost-effectiveness, making it a popular choice for both commercial and residential properties. For areas requiring enhanced durability and longevity, the 80 mils TPO roofing is preferred due to its thicker, more robust nature, offering better resistance to punctures and weathering. The 90 mils option represents one of the thickest, most durable TPO roofing materials available, designed for buildings in extreme weather conditions or where the roof is subject to heavy foot traffic. Other thicknesses cater to niche market needs, providing solutions for unique or specialized applications. This segmentation by thickness allows for tailored roofing solutions that meet diverse requirements, ensuring that there is a TPO roofing option available for virtually any scenario.

Commercial and Industrial, Residential in the Global Thermoplastic Polyolefin (TPO) Roofing Market:

The Global Thermoplastic Polyolefin (TPO) Roofing Market finds its applications predominantly in commercial and industrial, as well as residential sectors. In commercial and industrial settings, TPO roofing is highly valued for its ability to provide a durable, cost-effective solution for large-scale buildings. These environments often require roofing materials that can withstand heavy usage, extreme weather conditions, and environmental pollutants, all while maintaining energy efficiency and cost-effectiveness. TPO roofing meets these demands with its exceptional durability, ease of installation, and low maintenance requirements, making it an ideal choice for warehouses, factories, shopping centers, and other commercial or industrial buildings. On the other hand, the residential sector benefits from TPO roofing's versatility and aesthetic appeal. Homeowners appreciate the wide range of colors and textures available, allowing them to match their roofing with the overall design of their homes. Additionally, TPO's energy-efficient properties contribute to reduced heating and cooling costs, making it an attractive option for individuals looking to enhance their home's sustainability and comfort. The usage of TPO roofing across these sectors underscores its adaptability and effectiveness in meeting the diverse needs of the construction industry.

Global Thermoplastic Polyolefin (TPO) Roofing Market Outlook:

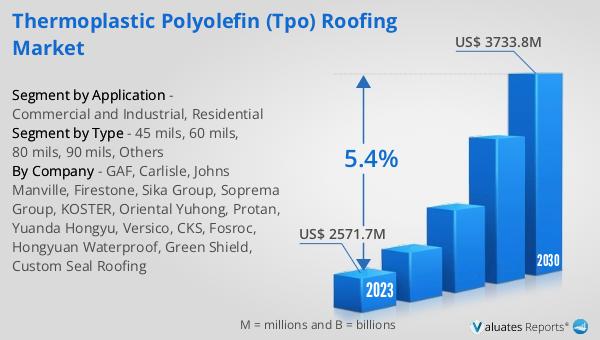

The market outlook for Global Thermoplastic Polyolefin (TPO) Roofing presents a promising future. In 2023, the market was valued at approximately $2571.7 million, showcasing its significance in the construction and roofing industries. The forecast suggests a robust growth trajectory, with expectations to reach around $3733.8 million by the year 2030. This anticipated growth, with a compound annual growth rate (CAGR) of 5.4% during the period from 2024 to 2030, highlights the increasing demand and adoption of TPO roofing solutions across various sectors. Such growth can be attributed to the numerous advantages TPO roofing offers, including its durability, energy efficiency, and cost-effectiveness, alongside a growing awareness and preference for sustainable building materials. This outlook not only reflects the market's current state but also underscores the potential for innovation and expansion in the coming years, as the industry continues to evolve in response to technological advancements and changing consumer preferences.

| Report Metric | Details |

| Report Name | Thermoplastic Polyolefin (TPO) Roofing Market |

| Accounted market size in 2023 | US$ 2571.7 million |

| Forecasted market size in 2030 | US$ 3733.8 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | GAF, Carlisle, Johns Manville, Firestone, Sika Group, Soprema Group, KOSTER, Oriental Yuhong, Protan, Yuanda Hongyu, Versico, CKS, Fosroc, Hongyuan Waterproof, Green Shield, Custom Seal Roofing |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |