What is Global Financial Management Information System Market?

The Global Financial Management Information System (FMIS) Market is a rapidly evolving sector that plays a crucial role in the financial operations of organizations worldwide. This market encompasses a range of software solutions designed to streamline and automate financial management processes, including budgeting, accounting, financial reporting, and asset management. These systems are essential for organizations to maintain accurate financial records, ensure compliance with regulatory standards, and make informed financial decisions. The FMIS market is driven by the increasing demand for efficient financial management solutions, the need for real-time financial data, and the growing complexity of financial operations in a globalized economy. As businesses expand their operations across borders, the need for integrated financial management systems that can handle multiple currencies, tax regulations, and financial reporting standards becomes more critical. The market is also influenced by technological advancements, such as cloud computing and artificial intelligence, which are enhancing the capabilities of FMIS solutions and making them more accessible to organizations of all sizes. Overall, the Global FMIS Market is poised for significant growth as organizations continue to prioritize financial efficiency and transparency in their operations.

Traditional Financial Management System, Modern Financial Management System in the Global Financial Management Information System Market:

Traditional Financial Management Systems (TFMS) have long been the backbone of organizational financial operations, providing essential tools for managing budgets, accounting, and financial reporting. These systems are typically characterized by their reliance on manual processes and paper-based documentation, which can be time-consuming and prone to errors. In a traditional setup, financial data is often siloed within different departments, making it challenging to obtain a comprehensive view of an organization's financial health. This lack of integration can lead to inefficiencies and delays in financial decision-making. However, TFMS have been instrumental in establishing foundational financial practices and ensuring compliance with regulatory standards. They have provided organizations with the necessary tools to manage their finances effectively, albeit with limitations in terms of scalability and adaptability to changing business environments.

Large Enterprise, Medium Enterprise, Small Enterprise in the Global Financial Management Information System Market:

In contrast, Modern Financial Management Systems (MFMS) leverage advanced technologies to overcome the limitations of traditional systems. These systems are designed to provide a more integrated and automated approach to financial management, enabling organizations to streamline their financial processes and improve accuracy. MFMS solutions often incorporate cloud-based platforms, allowing for real-time access to financial data from anywhere in the world. This accessibility is particularly beneficial for organizations with global operations, as it enables them to manage their finances more efficiently and respond quickly to market changes. Additionally, modern systems often include advanced analytics and reporting capabilities, providing organizations with deeper insights into their financial performance and helping them make more informed decisions. The integration of artificial intelligence and machine learning technologies further enhances the capabilities of MFMS, enabling predictive analytics and automated financial forecasting. These advancements are transforming the way organizations manage their finances, making financial operations more efficient, transparent, and adaptable to the dynamic business landscape.

Global Financial Management Information System Market Outlook:

The Global Financial Management Information System Market is witnessing significant growth as organizations increasingly recognize the benefits of modern financial management solutions. The transition from traditional to modern systems is driven by the need for greater efficiency, accuracy, and transparency in financial operations. Organizations are investing in FMIS solutions to enhance their financial management capabilities and gain a competitive edge in the market. As the demand for integrated and automated financial management solutions continues to rise, the FMIS market is expected to expand further, offering organizations new opportunities to optimize their financial operations and achieve their business objectives.

| Report Metric | Details |

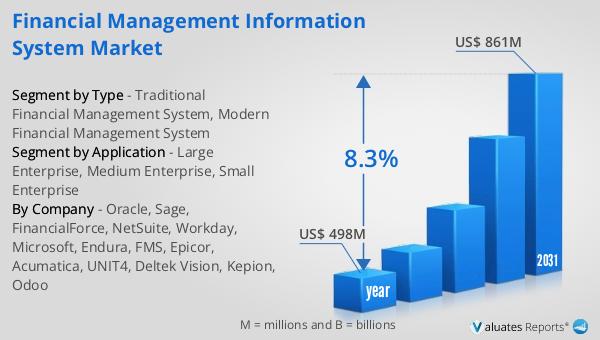

| Report Name | Financial Management Information System Market |

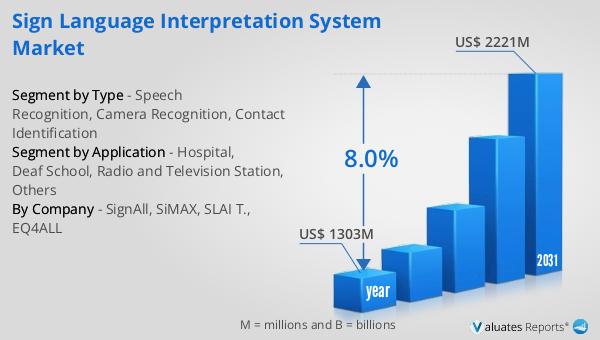

| Accounted market size in year | US$ 498 million |

| Forecasted market size in 2031 | US$ 861 million |

| CAGR | 8.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Oracle, Sage, FinancialForce, NetSuite, Workday, Microsoft, Endura, FMS, Epicor, Acumatica, UNIT4, Deltek Vision, Kepion, Odoo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |