What is Mining Machinery and Equipment - Global Market?

Mining machinery and equipment play a crucial role in the global market by providing the necessary tools and technology for extracting valuable resources from the earth. These machines are designed to perform a variety of tasks, including drilling, crushing, grinding, and transporting materials. The global market for mining machinery and equipment is vast and diverse, encompassing a wide range of products and services tailored to meet the needs of different mining operations. From large-scale surface mining operations to more specialized underground mining activities, the demand for efficient and reliable machinery is ever-present. The market is driven by the need for increased productivity, safety, and environmental sustainability in mining operations. As the demand for minerals and metals continues to grow, so does the need for advanced machinery that can operate in challenging environments and deliver high performance. Companies in this market are constantly innovating to develop new technologies and improve existing equipment, ensuring that they can meet the evolving needs of the mining industry. The global market for mining machinery and equipment is a dynamic and competitive landscape, with numerous players vying for market share and striving to deliver the best solutions to their customers.

Underground Mining Machinery, Surface Mining Machinery, Drills and Breakers, Screening Equipment, Mineral Processing Machinery, Feed Conveyors, Stackers, Reclaimers in the Mining Machinery and Equipment - Global Market:

Underground mining machinery is specifically designed to operate in the challenging conditions found beneath the earth's surface. These machines are built to navigate narrow tunnels and extract resources from deep within the ground. They include equipment such as continuous miners, longwall miners, and shuttle cars, which are used to cut and transport coal and other minerals. Surface mining machinery, on the other hand, is used in open-pit mining operations where resources are extracted from the earth's surface. This category includes equipment like draglines, shovels, and haul trucks, which are used to remove overburden and transport materials. Drills and breakers are essential tools in both underground and surface mining operations. Drills are used to create holes for blasting or for inserting explosives, while breakers are used to break up large rocks and boulders. Screening equipment is used to separate different sizes of materials, ensuring that only the desired size is processed further. Mineral processing machinery is used to separate valuable minerals from the ore, using techniques such as flotation, magnetic separation, and leaching. Feed conveyors are used to transport materials from one part of the mining operation to another, ensuring a continuous flow of materials. Stackers and reclaimers are used to manage stockpiles of materials, ensuring that they are stored efficiently and can be easily accessed when needed. These machines are essential for maintaining the flow of materials in a mining operation, ensuring that resources are extracted and processed efficiently. The global market for mining machinery and equipment is constantly evolving, with new technologies and innovations being developed to meet the changing needs of the industry. Companies in this market are focused on improving the efficiency, safety, and environmental sustainability of their equipment, ensuring that they can meet the demands of modern mining operations.

Transportation, Processing, Excavation in Coal, Minerals, Metals Mining in the Mining Machinery and Equipment - Global Market:

Mining machinery and equipment are used in various stages of the mining process, including transportation, processing, and excavation. In the transportation stage, equipment such as haul trucks, conveyors, and rail systems are used to move materials from the mining site to processing facilities or storage areas. These machines are designed to handle large volumes of materials and operate in challenging environments, ensuring that resources are transported efficiently and safely. In the processing stage, machinery such as crushers, mills, and separators are used to break down and refine raw materials, extracting valuable minerals and metals. These machines are designed to operate with high precision and efficiency, ensuring that the maximum amount of valuable material is extracted from the ore. In the excavation stage, equipment such as drills, excavators, and loaders are used to remove overburden and extract resources from the earth. These machines are designed to operate in harsh conditions, withstanding the rigors of mining operations and delivering high performance. In coal mining, machinery is used to extract coal from underground or surface mines, with equipment such as continuous miners and longwall miners playing a crucial role in the extraction process. In mineral mining, machinery is used to extract valuable minerals such as gold, silver, and copper, with equipment such as crushers and separators being used to process the ore. In metal mining, machinery is used to extract metals such as iron, aluminum, and zinc, with equipment such as smelters and refineries being used to process the raw materials. The global market for mining machinery and equipment is driven by the need for efficient and reliable equipment that can operate in challenging environments and deliver high performance. Companies in this market are focused on developing new technologies and improving existing equipment, ensuring that they can meet the evolving needs of the mining industry.

Mining Machinery and Equipment - Global Market Outlook:

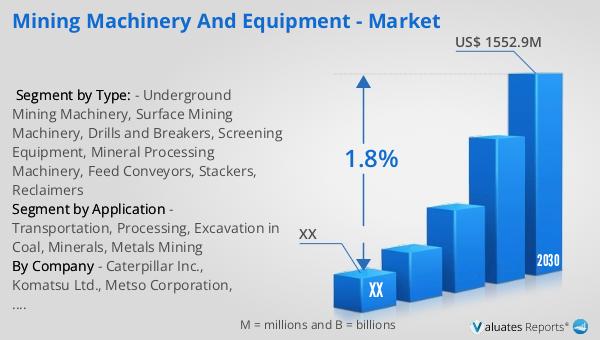

The global market for mining machinery and equipment was valued at approximately $1,373 million in 2023. It is projected to grow to a revised size of $1,552.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 1.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced mining machinery and equipment that can enhance productivity, safety, and environmental sustainability in mining operations. The North American market for mining machinery and equipment was also valued at a significant amount in 2023, with expectations of growth by 2030. The CAGR for this region during the forecast period of 2024 through 2030 highlights the steady demand for mining machinery and equipment in North America. This growth is driven by the need for efficient and reliable equipment that can operate in challenging environments and deliver high performance. Companies in this market are focused on developing new technologies and improving existing equipment, ensuring that they can meet the evolving needs of the mining industry. The global market for mining machinery and equipment is a dynamic and competitive landscape, with numerous players vying for market share and striving to deliver the best solutions to their customers.

| Report Metric | Details |

| Report Name | Mining Machinery and Equipment - Market |

| Forecasted market size in 2030 | US$ 1552.9 million |

| CAGR | 1.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Caterpillar Inc., Komatsu Ltd., Metso Corporation, Sandvik AB, Doosan Corporation, Liebherr, Hitachi, Atlas Copco AB, Epiroc AB, SANY Group, Hyundai Heavy Industries Group, Astec Industries Incorporated, Bell Equipment Limited, Boart Longyear Ltd, FLSmidth & Co. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |